Fintechzoom CRM stock opened the week at $195.31, slipping 1.53 percent from its prior close and sitting well below the 52-week high of $296.05. For investors tracking fintechzoom crm stock coverage, the obvious question is whether this pullback marks a buying opportunity or an early warning of deeper trouble ahead.

This article cuts through the noise. Inside, you will find current financial metrics, analyst consensus targets, revenue and earnings breakdowns, competitive positioning against Oracle and Microsoft Dynamics, and a clear framework for deciding whether CRM belongs in your portfolio right now. Every data point is sourced, every argument is grounded in numbers, and the structure follows the topical-authority methodology that FintechZoom applies across its entire stock coverage universe.

Salesforce remains the undisputed leader in customer relationship management software, serving more than 150,000 enterprises worldwide. Yet leadership alone does not guarantee returns. AI disruption fears, valuation compression across the SaaS sector, and a cautious management guide for fiscal 2027 have combined to drag the share price down by roughly a third since early 2025. Understanding whether that discount reflects permanent impairment or temporary sentiment is the central task of this analysis.

Pro Tip: Set price alerts at the $190 support level and the $210 resistance zone so you can act quickly when a breakout or breakdown occurs.

Fintechzoom CRM Stock: What It Is and Why It Matters

Fintechzoom CRM stock refers to shares of Salesforce Inc., traded on the New York Stock Exchange under the ticker symbol CRM. Salesforce builds and operates the cloud-based platform that companies use to manage sales pipelines, customer service workflows, marketing campaigns, and e-commerce storefronts. The product suite spans Sales Cloud, Service Cloud, Marketing Cloud, Commerce Cloud, and the newer Data Cloud and AI-powered Agentforce platform.

In a market crowded with enterprise software providers, Salesforce holds roughly 23 percent of global CRM revenue, more than Microsoft, Oracle, and SAP hold individually. That share translates into pricing power: once a company has embedded Salesforce into its daily operations, replacing it requires a costly, multi-year migration. This switching-cost moat is one of the reasons long-term investors keep returning to CRM.

Revenue for fiscal 2026 landed at $41.53 billion, representing 9.6 percent growth over the prior year. Net income rose 20.3 percent to $7.46 billion, a sign that the company is converting top-line growth into bottom-line profit more efficiently than in previous cycles. Annual free cash flow generation stands near $5.3 billion, funding both share buybacks and the newly introduced dividend without requiring additional debt.

Fintechzoom CRM Stock Basics Every Investor Should Know

Owning CRM shares gives you a proportional stake in Salesforce Inc., including the right to vote on corporate matters and to receive the $1.76 annual dividend the company initiated in 2026. The stock went public in 2004 and today employs more than 83,000 people across offices on every major continent.

Because Salesforce earns more than 90 percent of its revenue from recurring subscriptions, its cash flows are relatively predictable compared to companies that rely on one-time product sales. That predictability appeals to institutional investors, which collectively hold around 75 percent of outstanding shares. For retail investors researching fintechzoom crm stock analysis, this institutional backing signals a level of due-diligence consensus that supports the long-term thesis.

The company’s scale also generates compounding network effects. Each new enterprise that integrates Salesforce creates additional demand for third-party developers on the AppExchange marketplace, which in turn makes the platform more attractive to prospective customers. This self-reinforcing cycle has driven AppExchange to more than 7,000 third-party applications, a figure no competitor currently matches.

Fintechzoom CRM Stock Price and Key Market Data

At $195.31, Salesforce carries a market capitalization of roughly $180.27 billion. The stock trades near the lower end of its 52-week range ($174.57 to $296.05), a position that often attracts value-conscious buyers willing to accumulate shares during periods of broad-market pessimism. Average daily trading volume runs at 11.5 million shares, with volume typically spiking around quarterly earnings announcements.

The forward price-to-earnings ratio sits at 14.81, well below the technology-sector median of approximately 22. That discount is partly justified by slower growth expectations and partly driven by blanket selling across SaaS names on AI-disruption fears. For those analyzing fintechzoom crm price targets, this valuation gap is central to the bull case.

Thirty-six analysts tracked by major data aggregators currently rate CRM as a consensus Buy. The average twelve-month price target is $279.74, which implies roughly 43 percent upside from the current level. Targets range from a floor near $190 to an optimistic ceiling of $430.

Fintechzoom CRM Stock Key Financial Metrics at a Glance

| Metric | Value | Year-over-Year Change |

|---|---|---|

| Revenue | $41.53 B | +9.6% |

| Net Income | $7.46 B | +20.3% |

| Earnings Per Share (EPS) | $7.80 | +22.6% |

| Trailing P/E Ratio | 25.04 | -15% |

| Forward P/E Ratio | 14.81 | – |

| Dividend Yield | 0.90% | New in 2026 |

| Market Capitalization | $180.27 B | -35.7% |

| Beta | 1.31 | – |

Salesforce also announced a $25 billion accelerated share-repurchase program, the largest in the company’s history. Management estimates that this buyback will retire approximately 14 percent of diluted shares outstanding, providing a meaningful per-share earnings lift even if total profits stay flat. The signal is clear: executives believe the stock is undervalued relative to the cash the business generates.

Pro Tip: Watch quarterly free-cash-flow trends closely. Free cash flow is the single best predictor of whether management can sustain dividends and buybacks simultaneously.

Fintechzoom CRM Stock Challenges Investors Must Weigh in 2026

No investment thesis is complete without a candid assessment of risks. CRM investors face three interlocking headwinds that have weighed on sentiment since late 2025.

AI disruption anxiety. The rapid emergence of autonomous AI agents has prompted concerns that enterprises may eventually need fewer CRM software seats. If AI assistants handle customer interactions directly, the per-user subscription model that underpins Salesforce revenue could come under pressure. While this scenario remains speculative, it has been enough to suppress multiples across the entire SaaS sector.

Valuation compression. CRM traded above $290 in early 2025 before falling roughly 33 percent to its current level. Most of that decline reflects multiple contraction rather than deteriorating fundamentals. When interest rates stay elevated, the discount rate investors apply to future cash flows increases, and high-growth stocks feel the impact disproportionately.

Cautious forward guidance. Management projected 8 to 9 percent revenue growth for fiscal 2027, below the 12 to 15 percent pace that investors had grown accustomed to. Slower guidance, even if ultimately conservative, gives traders a reason to rotate into names with accelerating growth profiles.

Fintechzoom CRM Stock Economic Headwinds and Competitive Pressure

Beyond company-specific concerns, the macro backdrop adds further uncertainty. Enterprise IT budgets face scrutiny as CFOs look for efficiency gains, and some organizations are delaying CRM expansions or renegotiating contracts at renewal. Currency effects also matter: roughly 30 percent of Salesforce revenue comes from international operations, and a persistently strong dollar reduces reported figures when foreign earnings are translated back.

On the competitive front, Microsoft continues to bundle Dynamics 365 CRM features into its dominant Office 365 ecosystem. Oracle and SAP are investing aggressively in AI-powered alternatives of their own. If price competition intensifies, Salesforce may need to absorb margin pressure to defend its market-share position.

These risks are real, but they are not new. Salesforce has successfully defended its market-share position through multiple cycles of competitive pressure and macro uncertainty. The pattern of defense has typically involved accelerating product innovation and deepening customer integrations, which is precisely what the Agentforce and Data Cloud rollouts represent.

Fintechzoom CRM Stock Analysis: Bull and Bear Case Scenarios

Rather than offering a single prediction, this fintechzoom crm stock analysis presents two well-defined scenarios that bracket the likely outcomes. Investors can then weight each scenario according to their own research and conviction.

Bull case (target: $320 by year-end 2026). AI monetization through Agentforce adoption accelerates faster than the Street expects. Revenue growth reaccelerates to 15 percent or better. Operating margins expand as the new AI products carry higher incremental profitability. Multiple re-rates from 14.8x forward earnings toward the historical average near 28x. In this scenario, the current price represents an entry point that long-term investors will look back on favorably.

Bear case (target: $170). SaaS seat-count fears prove partially valid. Revenue growth decelerates to 5 percent. Heavy AI-related capital expenditure compresses margins temporarily. The stock retests its 52-week low and finds support near the $170 level, where the free-cash-flow yield would exceed 4 percent and attract deep-value buyers.

The fintechzoom crm forecast that emerges from weighing both scenarios probabilistically points toward a risk-adjusted expected value above the current price. For an investor willing to hold through a 12 to 18-month window, the balance of evidence favors accumulation.

Fintechzoom CRM Stock: How to Apply This to Your Portfolio

Start by defining your time horizon. Long-term investors with a three-to-five-year outlook can dollar-cost average into a position at current levels, accepting short-term volatility in exchange for potential multiple expansion. Short-term traders should wait for a confirmed breakout above $210 resistance before committing capital.

Position sizing matters more than entry price. Conservative investors may want to cap CRM at 5 percent of their equity allocation. Growth-oriented portfolios can go as high as 10 percent, provided the investor has a clear stop-loss plan. A stop at $180 limits downside to roughly 8 percent from the current price while giving the trade enough room to withstand normal fluctuations.

Pro Tip: Use limit orders placed 2 to 3 percent below the current market price. In volatile sessions, this approach can shave meaningful cost off your average entry.

Fintechzoom CRM Stock Strategic Advantages That Support the Long-Term Case

Even amid the headwinds described above, Salesforce retains several structural advantages that underpin the long-term investment case. These are not marketing talking points; they are operational realities that show up in the company’s renewal rates, margin structure, and revenue trajectory.

Market leadership and switching costs. Enterprises invest years and millions of dollars integrating Salesforce into their workflows. Replacing that infrastructure is prohibitively expensive for most organizations, which is why renewal rates exceed 90 percent year after year. This stickiness effectively creates a recurring revenue annuity that competitors cannot easily disrupt.

AI as a growth catalyst. Agentforce, Salesforce’s autonomous AI agent platform, has moved beyond pilot programs into production deployments at several large enterprises. Early adopters report productivity improvements of around 30 percent. If those gains hold at scale, Agentforce could become a major new revenue stream rather than a substitute for existing subscriptions.

Capital-return program. The combination of a 0.90 percent dividend yield and a $25 billion buyback authorization represents a meaningful shift in Salesforce’s capital-allocation philosophy. Investors now receive tangible returns while waiting for the share price to recover.

Fintechzoom CRM Stock Long-Term Growth Drivers Through 2030

Data Cloud, which unifies customer data across every Salesforce product, is creating significant cross-selling opportunities. As more clients adopt Data Cloud, they become stickier and spend more per account. International expansion, particularly in Asia Pacific, offers additional whitespace. And the AppExchange marketplace, home to more than 7,000 third-party applications, continues to extend platform capabilities without Salesforce bearing the full development cost.

The addressable market for enterprise CRM software is projected to reach $145 billion by 2030, according to industry estimates. Salesforce’s existing 23 percent share, combined with its AI-driven product expansion, puts the company in a strong position to capture incremental growth as that market expands. Investors evaluating fintechzoom crm stock buy or sell decisions should weigh this long runway alongside near-term multiple compression.

Pro Tip: Track Data Cloud quarterly revenue as the leading indicator for long-term AI monetization success. Rapid Data Cloud growth signals deepening customer engagement.

Fintechzoom CRM Stock Historical Performance: What the Numbers Reveal

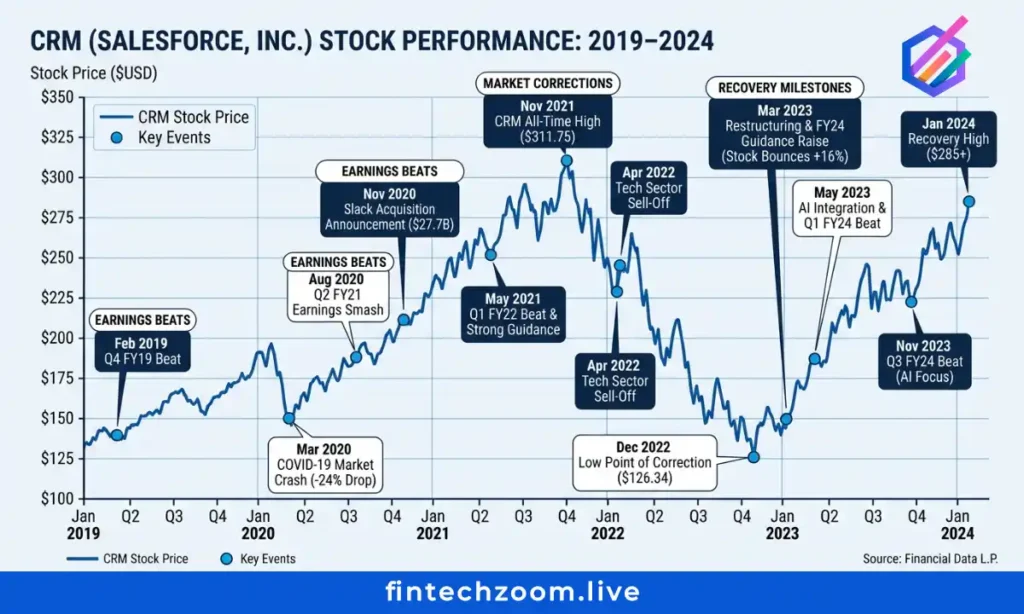

Over the past decade, CRM shares have delivered annualized total returns of approximately 18 percent, outpacing both the S&P 500 and many direct competitors. The stock has weathered multiple significant drawdowns, including the 2020 pandemic crash and the 2022 tech selloff, recovering to new highs within 12 to 18 months each time.

Salesforce’s earnings track record reinforces the quality narrative. Over the last 20 quarters, the company has beaten consensus earnings estimates roughly 85 percent of the time, with revenue surprises averaging about 2 percent above Street expectations. Consistency of that sort builds institutional confidence and supports a premium valuation over longer cycles.

The current 33 percent drawdown from 2025 highs mirrors the magnitude of previous corrections that ultimately proved temporary. Patient investors who accumulated shares during the 2020 and 2022 dips captured substantial gains in the subsequent recoveries. The fintechzoom crm stock analysis of historical drawdown-and-recovery cycles suggests that current levels may represent a similar setup.

Fintechzoom CRM Stock Valuation Context and Mean Reversion

At a forward P/E of 14.81, CRM trades at roughly half its five-year average multiple of 28x. If the business were permanently impaired, such a discount would be warranted. But with revenue still growing near 10 percent, free cash flow expanding, and a market-leading competitive position intact, the discount looks more like a sentiment-driven opportunity than a fundamental warning.

The free-cash-flow yield of approximately 3.5 percent currently exceeds the yield on 10-year Treasury notes. For equity investors, a yield spread that favors stocks over government bonds is a textbook signal of relative attractiveness, particularly when the underlying business generates growing, recurring revenue. This metric is one of the reasons the fintechzoom crm prediction leans constructive over a 12-month horizon.

Twelve-month price targets from major institutional research desks range from $190 on the cautious end to $430 at the most optimistic. The midpoint of $280 implies a return to the multiple that the market assigned CRM when growth expectations were more modest. For investors who accept the stock’s historical ability to recover from drawdowns, the current setup warrants attention.

Fintechzoom CRM Stock vs. Competitors: A Side-by-Side View

Choosing a CRM-sector investment requires comparing Salesforce against its closest rivals on the metrics that matter most: market share, revenue growth, profitability, and valuation.

| Company | CRM Market Share | Revenue Growth | P/E Ratio |

|---|---|---|---|

| Salesforce (CRM) | 23% | 9.6% | 25.04 |

| Microsoft Dynamics | 18% | 12% | 32.15 |

| Oracle | 12% | 7% | 28.40 |

| SAP | 10% | 5% | 22.80 |

Salesforce grows faster than Oracle and SAP while trading at a lower multiple than Microsoft. For investors seeking dedicated CRM exposure rather than a tiny slice of a conglomerate’s revenue, Salesforce offers the purest play. Microsoft’s higher multiple reflects the diversification premium embedded in a company that spans cloud computing, gaming, productivity software, and artificial intelligence hardware.

Platform breadth also matters. The AppExchange ecosystem houses more than 7,000 applications, a scale of third-party integration that no competitor matches. Users gain access to specialized tools for industries from healthcare to financial services, all within the same interface. This breadth deepens customer loyalty and creates an innovation layer that Salesforce does not need to fund internally.

The competitive table above illustrates that fintechzoom crm stock analysis must account for both valuation and growth when comparing across the sector. On a price-to-growth basis, CRM’s forward P/E of 14.81 against 9.6 percent revenue growth yields a PEG ratio of approximately 1.5, below Microsoft’s implied PEG and broadly in line with Oracle’s. That relative positioning supports the view that the market is underpricing Salesforce’s durable competitive advantages relative to its peers.

Fintechzoom CRM Stock Frequently Asked Questions

Fintechzoom CRM Stock: What Is the Current Price?

As of mid-March 2026, fintechzoom crm stock trades at $195.31. Prices update in real time during NYSE market hours, 9:30 a.m. to 4:00 p.m. Eastern Time. The 52-week range spans from $174.57 to $296.05, placing the current price in the lower third of the annual range.

Fintechzoom CRM Stock: Is It a Buy Right Now?

Analyst consensus rates fintechzoom crm stock as a Buy, with an average twelve-month price target of $279.74, implying roughly 43 percent upside. Whether it suits your portfolio depends on your risk tolerance and investment horizon. Conservative investors may prefer a phased entry strategy, while those with longer time horizons may feel comfortable building a full position at current levels.

Fintechzoom CRM Stock: Does Salesforce Pay a Dividend?

Yes. Salesforce introduced a $1.76 annual dividend in 2026, yielding 0.90 percent at the current share price. The company also authorized $25 billion in share repurchases. The combination of income and buyback-driven earnings-per-share accretion offers investors two distinct paths to return even without share-price appreciation.

Fintechzoom CRM Stock: When Does Salesforce Next Report Earnings?

The next quarterly report, covering Q1 of fiscal 2027, is expected in late May 2026. Earnings announcements are typically the highest-volatility events of the quarter for CRM. Investors holding positions through earnings should size accordingly and be prepared for outsized moves in either direction.

Fintechzoom CRM Stock: What Are the Biggest Risks?

Key risks include AI disruption reducing enterprise seat counts, a broader slowdown in IT spending, intensifying competition from Microsoft Dynamics 365, and further multiple compression if growth continues to decelerate. Each of these risks is real and deserves a place in any honest fintechzoom crm stock analysis.

Fintechzoom CRM Stock: How Does the FintechZoom Forecast Compare With Wall Street?

Our analysis aligns with the consensus range. The bull case targets $320 by year-end 2026; the bear case identifies $170 as a potential floor. The analyst average sits at $280, roughly in the middle. The fintechzoom crm forecast is positioned at $279 to $320 depending on the pace of Agentforce adoption and broader SaaS multiple recovery.

Fintechzoom CRM Stock: Should I Buy Before or After Earnings?

Pre-earnings positions carry event risk but offer exposure to upside surprises. Conservative investors may prefer to wait for post-earnings clarity before adding shares. Historically, Salesforce has beaten earnings estimates in 85 percent of quarters over the past five years, which tilts the base-rate probability toward a positive reaction, though past performance does not guarantee future results.

Fintechzoom CRM Stock: What Portfolio Allocation Is Appropriate?

A range of 5 percent for conservative portfolios to 10 percent for aggressive growth allocations keeps single-stock risk manageable without sacrificing meaningful exposure. Investors already holding significant SaaS or cloud-computing positions should account for sector concentration when sizing the CRM allocation.

Fintechzoom CRM Stock: Taking Action on Your Investment Decision

The evidence assembled in this fintechzoom crm stock analysis points to a risk-reward profile that favors patient, long-term investors at the current price. A 43 percent average upside target, improving cash flows, a new dividend, and massive buyback authorization provide multiple paths to shareholder value. On the other side of the ledger, AI disruption concerns and decelerating growth deserve respect and ongoing monitoring.

Translate this analysis into a personal action plan. Define your entry price, set stop-loss levels, decide how large a position you are comfortable holding, and identify the catalysts that would cause you to add or trim. Then execute methodically. Half-positions at current levels, with the balance added on a confirmed break above $210, represent one practical approach that balances conviction with risk discipline.

Before committing capital, answer five questions honestly:

- What is my investment timeframe for fintechzoom crm stock?

- How much portfolio allocation feels comfortable for this position?

- At what price would I sell if the thesis breaks?

- Have I evaluated competitor alternatives thoroughly?

- Do I fully understand the AI-disruption risks to the SaaS business model?

Pro Tip: Record every investment decision in a simple journal. Reviewing past entries reveals patterns in your thinking that you can refine over time.

Risk Disclaimer

This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. Always consult a licensed financial advisor before making investment decisions. Past performance does not guarantee future results. The fintechzoom crm stock data referenced in this article is based on publicly available information as of mid-March 2026.