Balmoral Funds investment strategy stands out in the middle market private equity space because it targets situations most firms walk away from. Carve-outs, turnarounds, distressed assets, these are not edge cases for Balmoral. They are the core of what this Los Angeles-based firm does, and has done since 2005.

This article breaks down exactly how the strategy works, what makes it different from standard buyout approaches, what results it has produced, and how sellers and management teams can decide whether Balmoral fits their situation in 2026.

Balmoral Funds Investment Strategy: What It Actually Targets

The Balmoral Funds investment strategy is built around one specific thesis: complex situations create better entry prices and larger value-creation opportunities than clean, competitive auction processes.

Most private equity firms prefer businesses with clean financials, stable earnings, and straightforward ownership. That preference drives up prices and compresses returns. Balmoral takes the opposite path. It focuses on:

- Corporate carve-outs: divisions being separated from large parent companies, often with operational complexity and transitional service agreements to manage

- Distressed asset investing: companies facing liquidity stress, capital structure problems, or operational setbacks that require fast, decisive action

- Management-led buyouts: transactions where the existing team wants a growth partner that brings more than just capital

This focus on complexity is not accidental. It is the foundation of the firm’s ability to generate returns in a market where clean deals have become expensive and crowded.

The firm targets businesses with revenue between $30 million and $800 million. Equity checks range from $10 million to $100 million. That range puts Balmoral squarely in the middle market, a segment large enough to support institutional investment but competitive enough that operational know-how matters as much as financial engineering.

Why Special Situations Private Equity Produces Different Results

Special situations private equity is a category, not just a description. It refers to investments where the value opportunity comes from resolving a structural, operational, or financial complexity rather than from simple multiple expansion or market growth.

Balmoral Funds investment strategy draws on this approach across every deal. The logic works like this:

When a large corporation decides to sell a non-core business unit, the transaction often comes with complications. Systems need to be separated. Contracts need to be assigned. Back-office functions need to be rebuilt. Traditional buyers see risk. Balmoral sees a business that will be simpler and stronger once those transitional challenges are resolved.

When a company faces a distressed situation, sellers often need speed and certainty more than maximum price. Buyers who can move quickly and close without financing contingencies gain an advantage. Balmoral’s Fund IV, which continues deployment through 2026, is structured to act in exactly those situations.

The result is a deal flow that looks different from what most buyout firms see. Fewer auction processes. More direct sourcing. More situations where operational expertise is the actual competitive advantage.

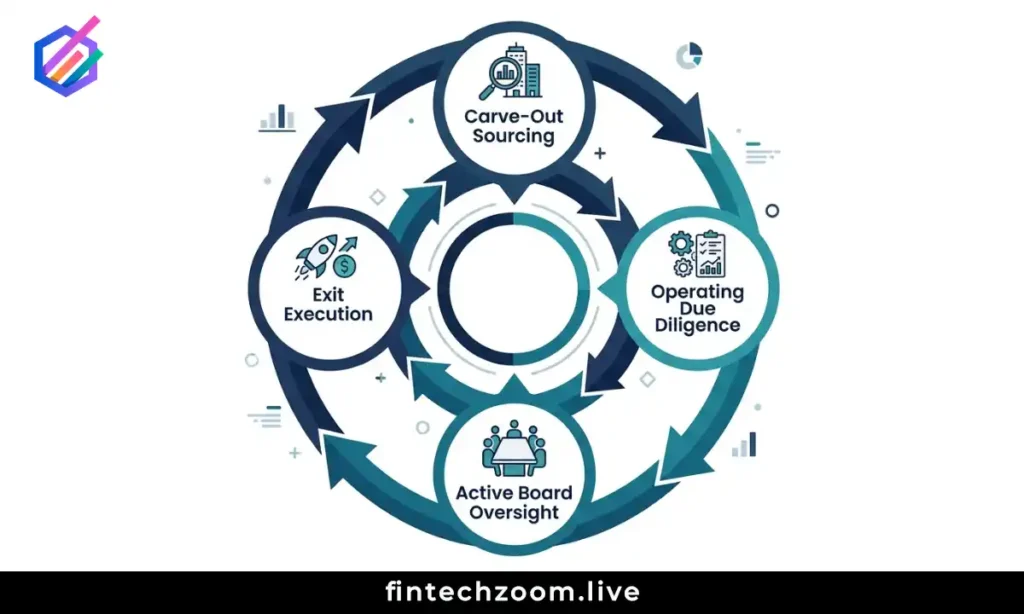

The Operating Advisor Model: Balmoral Funds Investment Strategy in Practice

One of the defining characteristics of the Balmoral Funds investment strategy is the use of experienced operating advisors on every deal. These are not board observers or consultants brought in after problems appear. They are active participants in the investment from day one.

The operating advisor model works on several levels:

Due diligence: Operators with industry experience identify problems and opportunities that financial analysts miss. A former plant manager reviewing a manufacturing carve-out sees things in an operational walk-through that a spreadsheet cannot capture.

Value creation planning: Before a deal closes, the operating team develops a specific plan for improving the business. That plan drives the investment thesis and the underwriting assumptions.

Post-close execution: After closing, operating advisors take active roles. Balmoral takes board seats on every portfolio company. Advisors work directly with management on the specific initiatives identified during due diligence.

This hands-on model requires management co-investment as well. Every Balmoral deal includes a requirement that the management team invest alongside the fund. This alignment mechanism matters. A management team that has personal capital at risk behaves differently than one that is simply employed. Decisions become more focused. Accountability becomes more direct.

The combination, active operating advisors plus management co-investment, creates a governance structure that reduces the gap between investment thesis and actual execution.

Balmoral Funds Investment Strategy: Target Company Profile

Not every business is a fit for the Balmoral Funds investment strategy. The firm has developed a clear picture of the companies it wants to own and the situations where its model creates the most value.

Revenue range: $30 million to $800 million. Below that floor, businesses often lack the management depth to absorb the demands of a PE-backed transformation. Above that ceiling, deal complexity and capital requirements move into a different market tier.

Industry focus: Balmoral considers all industries but has built particular depth in industrials and chemicals. These sectors frequently produce carve-out opportunities as large conglomerates rationalize their portfolios. They also tend to have operating complexity that rewards hands-on advisors.

Situation type: Corporate carve-outs, distressed transactions, and management-led buyouts. Each of these produces a different kind of complexity, but all three benefit from the same operating-first approach.

Management alignment: The team must be willing to co-invest and to operate under active board oversight. Companies where management sees private equity as passive capital are not a fit.

Transaction certainty: Sellers in complex situations often value certainty of close over maximum price. Balmoral’s track record of executing difficult transactions is part of its competitive positioning with these sellers.

Balmoral Funds Investment Strategy: Real Results From Fund History

The Balmoral Funds investment strategy is not theoretical. It has produced documented results across multiple fund cycles.

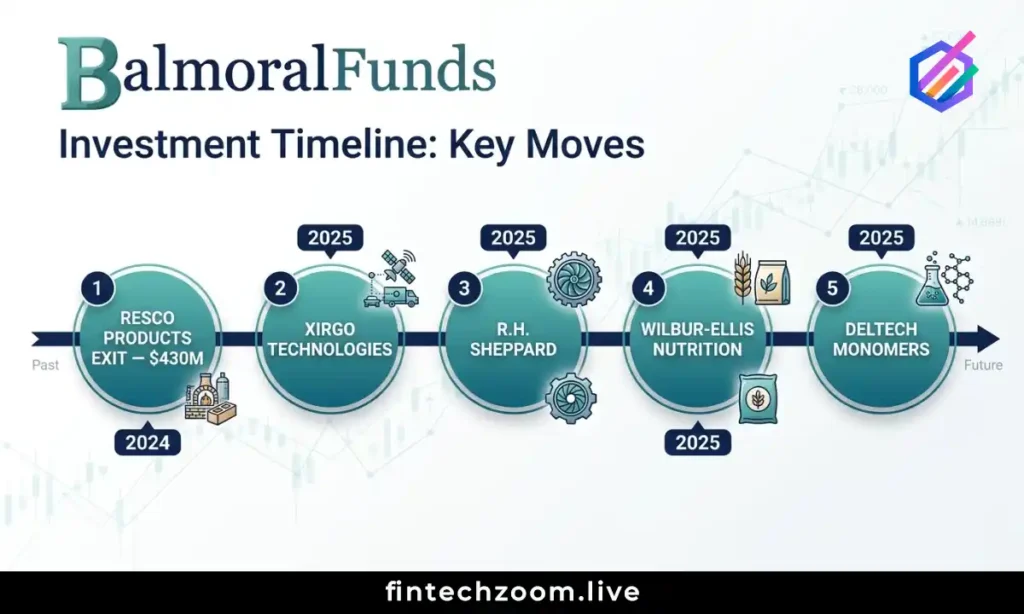

The clearest recent example is the exit from Resco Products. The sale reached approximately $430 million, a significant outcome for a middle market industrial business. Before the exit, the operating team had worked directly on improving manufacturing efficiency, expanding the customer base, and strengthening the management structure. The sale validated the carve-out investment thesis.

The 2025 deal activity showed the same pattern. Four new investments followed the core strategy:

Xirgo Technologies came through a carve-out process. The business, which provides fleet management technology solutions, was separated from a larger parent and required the kind of transitional support that Balmoral’s operating model is built for.

R.H. Sheppard added steering system expertise to the portfolio. The business serves commercial vehicle manufacturers and fit the industrial sector focus that has driven much of Balmoral’s historical deal flow.

Wilbur-Ellis Nutrition strengthened the portfolio’s exposure to agriculture-adjacent businesses. The deal reflected the firm’s willingness to move across sectors when the situation type matches the investment model.

Deltech Monomers closed in December 2025, adding a specialty chemicals business. Chemicals has been a consistent area of activity for Balmoral given the frequency of corporate carve-outs in that sector.

Each of these transactions reflects the Balmoral Funds investment strategy operating as designed: sourcing complex situations, applying operational expertise, and building businesses that are stronger and more independent than they were under corporate ownership.

How Balmoral Funds Investment Strategy Compares to Standard Buyout Approaches

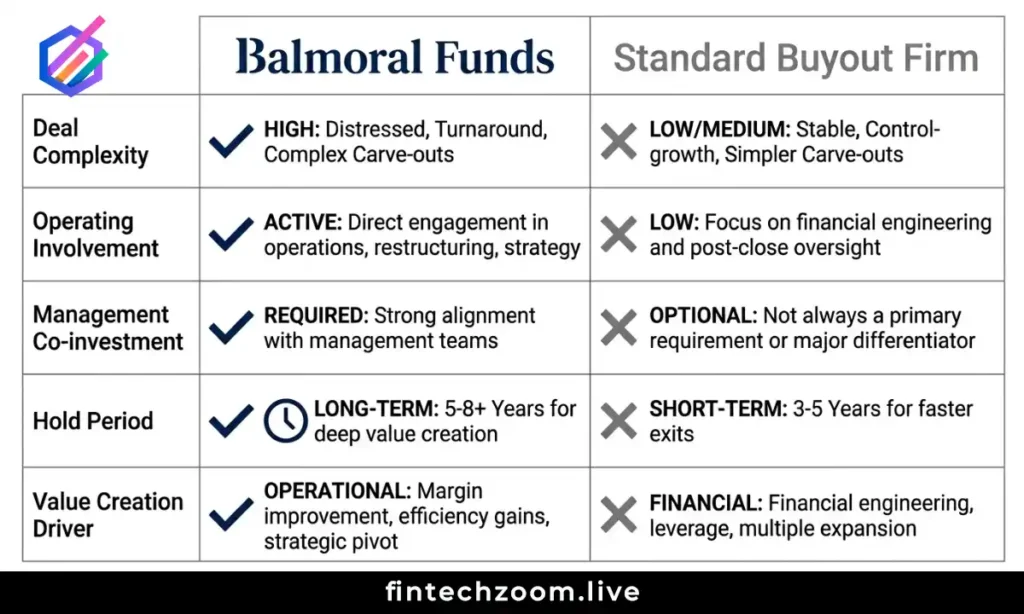

Understanding the Balmoral Funds investment strategy requires understanding what it is not. Standard middle market buyout firms follow a fairly consistent model: find a well-run business in a growing sector, pay a competitive price at auction, apply financial leverage, and sell after improving EBITDA margins or revenue. That model works, but it depends on starting with a clean, well-positioned business.

Balmoral’s approach differs in several ways:

| Feature | Balmoral Funds | Standard Middle Market PE |

|---|---|---|

| Target complexity | High (carve-outs, distressed) | Low to medium |

| Deal sourcing | Direct, proprietary | Auction-heavy |

| Operating involvement | Active advisors on every deal | Limited or reactive |

| Management co-investment | Always required | Sometimes optional |

| Industry depth | Industrials and chemicals | Sector-agnostic |

| Hold period | Patient capital | Defined timeline |

| Value creation driver | Operational improvement | Multiple expansion |

The table shows that Balmoral occupies a specific position in the PE market. It is not trying to compete with firms that win auction processes on price. It is trying to source situations where its operating model creates advantages that purely financial buyers cannot replicate.

Balmoral Funds Investment Strategy and the 2026 Market Environment

The Balmoral Funds investment strategy is particularly well-suited to the 2026 market environment for several reasons.

Large corporations continue to rationalize their business portfolios. After years of expansion, many industrial and chemical companies are divesting non-core units to focus capital and management attention. That wave of corporate portfolio activity creates a consistent supply of carve-out opportunities, exactly the deal type where Balmoral has the deepest experience.

Interest rate conditions have also changed how distressed investing works. Higher borrowing costs have put pressure on businesses that carried significant debt loads at lower rates. Companies that need capital structure solutions are increasingly willing to accept terms that include active board involvement and operational support.

Fund IV continues deployment through 2026. The fund size supports meaningful equity checks across the $10 million to $100 million range, which means Balmoral can move quickly when the right situation appears. Speed and certainty remain competitive advantages in situations where sellers are managing uncertainty.

Jonathan Victor, who founded the firm and leads Fund IV, brings a restructuring background that informs how the team evaluates distressed situations. That experience is directly relevant to the types of transactions that define the Balmoral Funds investment strategy.

Balmoral Funds Investment Strategy: What Sellers and Management Teams Should Know

If you run a middle market business that fits the Balmoral profile, whether as a corporate parent considering a divestiture, a management team seeking a growth partner, or an intermediary representing a complex situation — there are several things worth knowing about how the firm operates.

Speed matters. Balmoral is structured to move quickly in situations that require certainty of close. The firm does not need to go back to an investment committee multiple times or wait for debt financing to commit to a deal.

Operations come before financial engineering. The investment thesis on every deal is rooted in a specific operational improvement plan. If you are a management team, expect to engage deeply with that plan during diligence and to co-invest based on it.

Industry experience is real. The operating advisors on each deal have direct sector experience. Conversations during due diligence are substantive, not just process-driven.

Patient capital changes the dynamic. Balmoral does not operate on a rigid hold period. If a business needs more time to realize its full value, the fund structure supports that. That patience is genuinely different from how most PE firms operate.

Management alignment is non-negotiable. Co-investment is a requirement, not a preference. Management teams that want a passive financial partner should look elsewhere. Teams that want an active partner with operational resources will find the model works well.

Balmoral Funds AUM and Fund Structure

Balmoral Funds manages approximately $1.3 billion in assets under management across its fund history. That scale positions the firm to write meaningful equity checks while staying focused on the middle market where its operational model creates the most differentiated value.

Fund IV is the current vehicle and continues to deploy capital through 2026. The fund’s focus mirrors the firm’s historical approach: special situations across industrials, chemicals, and adjacent sectors, with active board involvement and operating advisors on every portfolio company.

The AUM figure also reflects the firm’s track record of successfully exiting investments. Returns have been generated across fund cycles that included the post-2008 recovery period, the mid-2010s industrial expansion, and the more recent period of corporate portfolio rationalization.

Balmoral Funds Investment Strategy: Frequently Asked Questions

What is the Balmoral Funds investment strategy? The Balmoral Funds investment strategy focuses on special situations private equity, specifically corporate carve-outs, distressed assets, and management-led buyouts in the middle market. The firm targets businesses with revenue between $30 million and $800 million and applies an operating-first model to create value post-close.

Where is Balmoral Funds based? Balmoral Funds is based in Los Angeles, California. The firm has operated from that base since its founding in 2005.

Who leads Balmoral Funds? Jonathan Victor founded the firm and leads Fund IV. His background in restructuring directly informs how the team approaches distressed and complex situations.

How does Balmoral Funds compare to other private equity firms? The Balmoral Funds investment strategy differs from standard buyout approaches in its focus on complex situations, its active operating advisor model, and its requirement for management co-investment on every deal. The firm does not compete primarily on price in auction processes.

What industries does Balmoral focus on? Balmoral considers all industries but has the deepest experience in industrials and chemicals, sectors that frequently produce the carve-out and distressed opportunities that fit the investment model.

How large are Balmoral’s equity checks? Equity checks range from $10 million to $100 million, targeting companies with revenue between $30 million and $800 million.

Is Fund IV still investing? Yes. Fund IV continues to deploy capital through 2026.

What was the Resco Products exit? Resco Products was a portfolio company that Balmoral exited for approximately $430 million. The exit validated the carve-out thesis and reflected the operating improvements made during the hold period.

External Resources

- Balmoral Funds Official Website

- Private Equity Industry Data — PitchBook

- Middle Market PE Research — Association for Corporate Growth

Risk Disclaimer

Private equity investments involve significant risk, including the potential loss of principal. The information in this article is intended for informational purposes only and does not constitute investment advice. Past performance of any fund or portfolio company does not guarantee future results. Prospective investors should conduct independent due diligence and consult qualified advisors before making investment decisions.