A data-driven breakdown of AAPL valuation, analyst targets, Apple Intelligence impact, and whether to buy, hold, or sell in 2026.

Introduction to Fintechzoom Apple Stock Analysis

Apple Inc. consistently ranks among the most searched and closely watched equities on the planet. For investors navigating the fast-moving tech sector, Fintechzoom Apple Stock data has become a go-to resource for timely market intelligence, price tracking, and forward-looking analysis. This guide delivers a thorough examination of where AAPL stands heading into the second half of 2026 and what could move the needle over the coming quarters.

The purpose of this article is straightforward. Rather than rehashing surface-level bullet points, we dig into the numbers that actually matter: revenue segmentation, margin trajectories, Wall Street consensus targets, and the real-world financial impact of Apple Intelligence. Every section ties back to specific data points, giving you the context needed to make confident portfolio decisions.

Whether you are a long-term shareholder evaluating your position, a growth-oriented investor looking for the right entry point, or a newcomer researching your first tech stock purchase, this Fintechzoom Apple Stock guide is structured to answer your most pressing questions. We cover current trading metrics, fundamental strength, competitive positioning, technical chart signals, and risk factors, all in one place.

Pro Tip: Bookmark this page and revisit it before each quarterly earnings release. Apple typically reports in January, April, July, and October, and we update our analysis within 24 hours of each call.

Apple Stock Price Today: Real-Time Market Snapshot

Current Trading Metrics and Valuation Data

Apple stock trades under the ticker AAPL on the NASDAQ exchange, and it remains one of the most liquid securities available to retail and institutional investors alike. On any given session, tens of millions of AAPL shares change hands, which means you can enter or exit positions with minimal slippage regardless of size.

The core valuation metrics that every investor should track include the price-to-earnings ratio, market capitalization, earnings per share, dividend yield, and beta. The P/E ratio measures how much the market is willing to pay for each dollar of Apple’s earnings. A ratio significantly above the S&P 500 average suggests the market expects above-average growth. Market capitalization, which now exceeds three trillion dollars, reflects the total value investors assign to every outstanding share. Beta, a measure of price volatility relative to the broader market, hovers near 1.0 for AAPL, indicating that it generally moves in step with major indices. This moderate volatility profile makes Apple a suitable core holding for both conservative income portfolios and growth-oriented accounts.

Pro Tip: Set up price alerts through your brokerage app at key support and resistance levels. Automated alerts remove emotion from decision-making and help you act when the price reaches your predefined entry or exit targets.

How Apple’s Market Cap Stacks Up Against Tech Peers

Apple holds the distinction of carrying the largest market capitalization among publicly traded technology companies. Microsoft and Alphabet compete for the second and third positions, and the ranking shifts periodically depending on quarterly results and broader sector sentiment. What separates Apple from most peers is the combination of hardware revenue scale and a rapidly expanding Services segment, which together create a diversified earnings stream that many pure-play software companies lack.

This market cap leadership matters for your portfolio for a practical reason. Companies at this scale attract enormous institutional ownership, which provides a floor of buying support during broad market selloffs. Pension funds, sovereign wealth vehicles, and index-tracking ETFs are structurally required to hold AAPL, which smooths volatility over time.

Fintechzoom Apple Stock Forecast: What Wall Street Expects for 2026

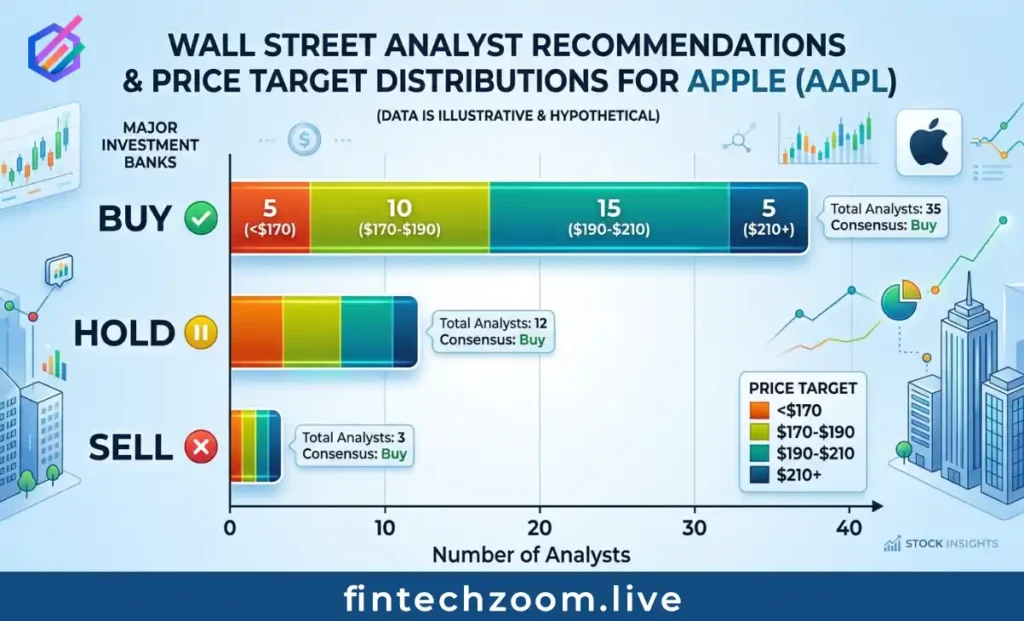

Analyst Price Target Range and Consensus Ratings

Major sell-side firms publish updated price targets and investment ratings for Apple on a rolling basis throughout each quarter. As of early 2026, the consensus among top-tier analysts points to moderate upside from current trading levels, with the average twelve-month price target reflecting expectations of continued, steady earnings growth rather than an explosive re-rating.

Firms such as Goldman Sachs, Morgan Stanley, and JP Morgan each approach the Apple thesis from a slightly different angle. Goldman tends to emphasize the long-term margin expansion potential of Services revenue. Morgan Stanley focuses heavily on the iPhone replacement cycle and the adoption curve of Apple Intelligence features. JP Morgan frequently highlights capital return programs, including the company’s historically aggressive share buyback strategy, as a key driver of EPS accretion. Across these perspectives, the buy-rated consensus suggests that Apple’s current valuation is justifiable if management executes on its stated product roadmap and Services growth targets.

On the bearish side, conservative price targets generally assume a weaker macroeconomic backdrop, slower consumer spending in developed markets, and the possibility that Apple Intelligence adoption may fall short of optimistic projections. These lower targets still tend to imply limited downside from current prices, which speaks to the defensive quality embedded in the stock.

Pro Tip: Track rating changes and price target revisions on financial terminals or aggregation sites. A cluster of upgrades from multiple firms within a short window often signals a meaningful shift in institutional sentiment.

Revenue and Earnings Growth Projections

Apple’s revenue outlook for fiscal 2026 centers on two growth engines. The Services segment, which encompasses the App Store, Apple Music, iCloud, AppleCare, and the expanding advertising business, continues to deliver recurring, high-margin revenue that compounds predictably quarter over quarter. iPhone revenue, which still represents the largest single contributor to the top line, depends on upgrade cycle timing, average selling prices, and the competitive landscape in key geographic markets.

Earnings per share projections reflect the combined effect of organic revenue growth, operating leverage from Services scale, and the mechanical benefit of ongoing share repurchases. Fewer outstanding shares mean that the same pool of net income translates to a higher per-share figure, a dynamic that has quietly boosted AAPL’s EPS trajectory for over a decade. Gross margins remain anchored near historical averages, with supply chain discipline and component pricing trends roughly offsetting each other over multi-year periods.

Geographic diversification adds another dimension to the revenue picture. The Americas and Europe provide stable, mature market foundations, while Greater China represents both a meaningful revenue contributor and a source of geopolitical uncertainty. Emerging markets across Southeast Asia, India, and Latin America offer incremental growth opportunities that are still in their early innings.

Apple Intelligence and Its Impact on Stock Valuation

AI Monetization Pathways

Apple Intelligence represents the company’s most significant software-driven value proposition since the launch of the App Store. By embedding machine learning and generative AI capabilities directly into the operating system layer, Apple has created a platform advantage that third-party developers and enterprise customers can build on top of. The investment thesis around Apple Intelligence rests on a simple premise: advanced AI features that require newer hardware processors create a natural upgrade incentive for the installed base, while premium AI-powered services open new subscription revenue streams.

Potential monetization routes include premium tiers within existing subscription bundles such as Apple One, standalone AI productivity tools for business users, and licensing arrangements with enterprise customers who value on-device processing for privacy and security reasons. Analysts estimate that even modest per-user revenue uplift from AI services could translate into billions of incremental annual revenue when applied across Apple’s installed base of over two billion active devices.

iPhone Upgrade Cycle Acceleration

One of the most consequential effects of Apple Intelligence is its potential to compress the iPhone replacement cycle. During the pandemic years, the average time between upgrades lengthened as incremental hardware improvements failed to motivate consumers to trade in functional devices. Apple Intelligence changes this equation by making advanced AI features exclusive to devices with the latest neural engine chipsets, meaning that older iPhones physically cannot run the full suite of new capabilities.

This hardware exclusivity creates a pull-through effect similar to what Apple experienced during major form factor transitions. Carrier promotions and trade-in programs further reduce the financial barrier to upgrading. If the upgrade rate rises even a few percentage points above its recent baseline, the impact on quarterly iPhone revenue could be substantial and sustained across multiple product generations.

Fundamental Analysis: Revenue Composition and Profitability

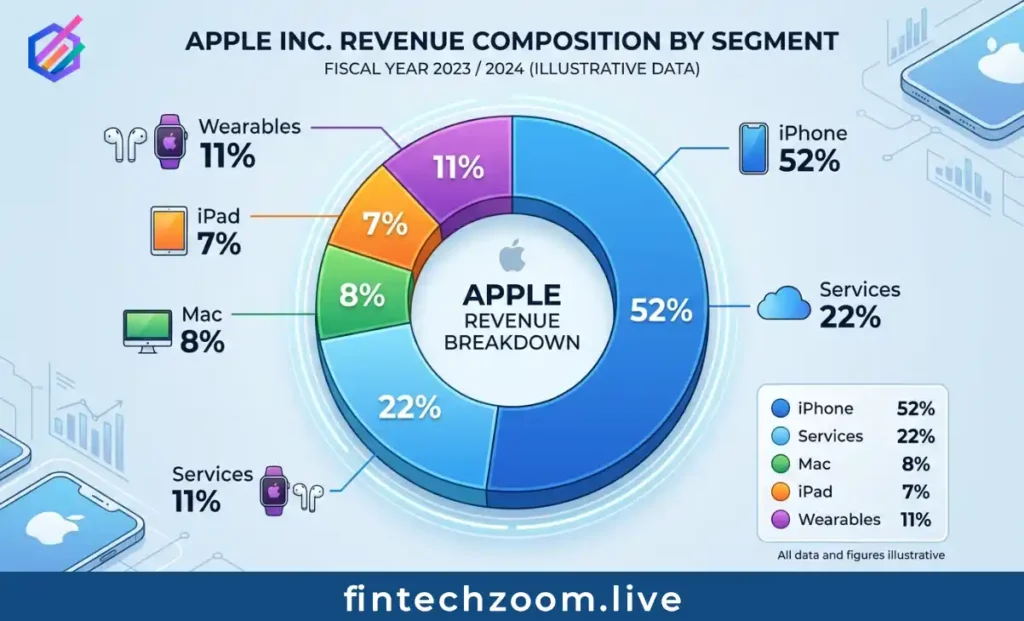

Revenue Breakdown by Business Segment

Understanding how Apple earns its money is essential to evaluating the stock’s risk profile. iPhone revenue constitutes the majority of total sales, which concentrates a large portion of the business in a single product category subject to consumer electronics replacement cycles. However, this concentration has been steadily declining as the Services segment scales. Services revenue now represents a meaningfully larger share of the total than it did five years ago, and its margins are significantly higher than hardware margins.

Mac and iPad contribute smaller but consistent revenue streams, and their growth tends to correlate with product refresh cycles and educational market demand. The Wearables, Home, and Accessories category, which includes Apple Watch, AirPods, and HomePod, has matured into a stable business line that complements the core hardware ecosystem. Advertising revenue, primarily from App Store search ads, is a newer growth area that remains underappreciated in most analyst models.

Profitability and Cash Flow Generation

Apple’s profitability metrics rank among the strongest in the technology sector. Gross margins consistently exceed 35 percent on a blended basis, supported by premium pricing, disciplined cost management, and the high-margin contribution of Services. Operating margins benefit from economies of scale and a relatively lean cost structure for a company of Apple’s revenue size.

Free cash flow generation is the metric that underpins Apple’s capital return strategy. The company produces tens of billions of dollars in free cash flow annually, which funds dividend payments, share repurchases, and strategic investments without requiring external financing. Return on equity has exceeded 100 percent in recent periods, a reflection of efficient capital deployment and the company’s willingness to use balance sheet leverage in the form of long-term debt to optimize its cost of capital.

Fintechzoom Apple Stock: Buy, Hold, or Sell in 2026?

The Bull Case for Buying Apple Stock

The most compelling argument for owning AAPL in 2026 centers on the strength and durability of the Apple ecosystem. Users who own an iPhone, Mac, Apple Watch, and AirPods face extraordinarily high switching costs. This lock-in effect translates directly into pricing power, repeat purchases, and a predictable flow of Services revenue. No other consumer technology company has replicated this level of hardware-software integration at Apple’s scale.

Brand loyalty reinforces the economic moat. Apple customers consistently demonstrate willingness to pay premium prices, which protects margins even during periods of competitive pressure. On the capital allocation front, management has demonstrated a clear commitment to returning value to shareholders through the largest corporate buyback program in history and a growing dividend. These programs provide a visible return floor that limits downside during periods of market weakness.

The Fintechzoom Apple Stock outlook for long-term investors remains constructive. The combination of ecosystem stickiness, expanding Services revenue, disciplined capital allocation, and the emerging Apple Intelligence growth driver creates a risk-reward profile that continues to attract institutional capital.

The Bear Case and Key Risk Factors

No investment thesis is without vulnerabilities, and Apple carries several identifiable risks. China exposure tops the list. Apple generates a meaningful portion of its revenue from Greater China, and both demand-side headwinds from local competitors and supply-side risks from geopolitical tensions could disrupt this business. Regulatory scrutiny of the App Store business model represents another structural risk. Antitrust actions in the European Union, the United States, and other jurisdictions could force changes to commission rates or distribution practices, directly impacting Services margins.

From a valuation standpoint, AAPL trades at a premium to its own historical averages and above most large-cap peers. If earnings growth disappoints or macroeconomic conditions tighten, the stock is vulnerable to multiple compression. Interest rate sensitivity compounds this risk, as higher discount rates reduce the present value of future cash flows and disproportionately affect growth-oriented names in the technology sector. Finally, if Apple Intelligence features fail to generate meaningful consumer excitement or measurable revenue uplift, the upgrade cycle thesis could prove overly optimistic.

Apple Stock vs. Microsoft and Google: Performance Comparison

Apple vs. Microsoft Stock Analysis

Microsoft and Apple represent two fundamentally different technology business models. Microsoft’s growth engine is Azure cloud computing and enterprise software, which generate recurring revenue with high customer retention. Apple’s strength lies in consumer hardware integration and the fast-growing Services layer built on top of that installed base. Both companies deliver strong free cash flow, maintain investment-grade balance sheets, and return substantial capital to shareholders through dividends and buybacks.

Revenue growth rates tend to favor Microsoft during periods of aggressive cloud adoption, while Apple’s margin profile benefits from its premium hardware pricing and Services mix shift. Dividend yields are comparable between the two, and both companies have delivered annualized total returns that outpace the broader market over the past five and ten years.

Apple vs. Google Stock Comparison

Alphabet’s Google presents a different competitive comparison. Google’s core business is digital advertising, which makes its revenue more cyclical and dependent on macroeconomic conditions than Apple’s diversified model. However, Google maintains substantial competitive advantages in search, YouTube, and Android, and its AI research capabilities through DeepMind are among the most advanced in the industry.

On valuation, Google often trades at a lower P/E multiple than Apple, reflecting the market’s perception of higher regulatory risk and advertising cyclicality. Apple’s premium valuation reflects the defensive characteristics of its ecosystem and the predictability of its cash flow generation. Both stocks face regulatory headwinds, but the nature of those risks differs: antitrust concerns around search dominance for Google versus App Store commission practices for Apple.

Key Financial Metrics Comparison

| Metric | Apple (AAPL) | Microsoft (MSFT) | Google (GOOGL) |

| P/E Ratio | ~28.5x | ~32.1x | ~24.3x |

| Dividend Yield | ~0.52% | ~0.78% | ~0.45% |

| Revenue Growth | ~6.2% | ~12.4% | ~8.7% |

| Operating Margin | ~29.8% | ~42.1% | ~27.5% |

| Market Cap | ~$3.2T | ~$2.9T | ~$2.1T |

Note: Figures are approximate and subject to daily market fluctuations. Verify current data on your brokerage platform.

Dividend History and Shareholder Return Programs

Dividend Yield and Growth Trajectory

Apple reinstated its dividend in 2012 after a long hiatus, and has increased the payout every year since. The current yield is modest relative to traditional income stocks, but the annual growth rate consistently exceeds ten percent, which means the income stream compounds meaningfully for long-term holders. The payout ratio remains conservative, typically below twenty percent of net income, leaving ample room for continued increases without straining cash flow.

For income-focused investors, the dividend alone may not justify a position. The real appeal lies in the combination of dividend growth and share price appreciation, which together have delivered a total return that outpaces most pure dividend strategies in the technology sector.

Share Buyback Program and Capital Allocation

Apple’s buyback program is the largest in corporate history by a wide margin. The company has retired billions of dollars’ worth of shares over the past decade, reducing the total share count by a meaningful percentage. This systematic reduction in outstanding shares mechanically boosts earnings per share, even in periods where net income growth is moderate.

Management adjusts the pace of repurchases based on prevailing share prices and available cash flow, which means buyback activity tends to accelerate during periods of price weakness. This countercyclical approach signals management confidence in intrinsic value and provides a structural floor under the stock price during market dislocations.

Technical Analysis: Support, Resistance, and Momentum Signals

Moving Averages and Chart Structure

From a technical perspective, Apple stock currently trades above its 50-day and 200-day simple moving averages, a configuration that chart-oriented investors interpret as a bullish signal. When the shorter-term average crosses above the longer-term average, a pattern known as a golden cross, it historically correlates with sustained upward momentum in large-cap equities.

Key support levels have formed at previous consolidation zones where buying interest absorbed selling pressure during past pullbacks. These price levels serve as logical areas to place stop-loss orders for active traders, or to consider adding to positions for investors employing a scaling strategy. Resistance levels, marked by prior swing highs, represent price points where selling pressure has historically intensified. A decisive breakout above the nearest resistance level on elevated volume would be a technically significant development.

Oscillators and Momentum Readings

The Relative Strength Index (RSI) for AAPL currently reads in neutral territory, which indicates that the stock is neither overbought nor oversold. This reading suggests that further upside movement is technically possible without triggering the short-term exhaustion signals that often precede pullbacks. The MACD histogram remains in positive territory with a bullish signal line configuration, reinforcing the constructive momentum picture.

Volume analysis provides additional confirmation. Elevated volume on up-days relative to down-days is consistent with institutional accumulation, a pattern that typically supports continued price strength. Low-volume pullbacks within the prevailing uptrend suggest healthy profit-taking rather than aggressive distribution by large holders.

Upcoming Earnings Calendar: What to Monitor

Priority Metrics for the Next Quarterly Report

When Apple reports its next quarterly results, the metrics that will move the stock are iPhone revenue and average selling price, Services revenue and growth rate, gross margin percentage, and updated guidance for the following quarter. Any positive surprise in Services growth would reinforce the long-term thesis that Apple is transitioning from a hardware-dependent business to a platform-and-services company with recurring revenue characteristics.

Earnings per share relative to the consensus estimate will drive the immediate post-report price reaction, but investors should focus equally on the quality of the beat or miss. Revenue-driven earnings growth is more sustainable than growth achieved purely through cost cutting or financial engineering.

Management Commentary and Forward Guidance

Apple’s management team typically provides revenue guidance for the immediately following quarter, expressed as a range. The width of that range and the tone of the accompanying commentary signal management’s confidence level. Conservative guidance that the company subsequently beats has been Apple’s pattern for years, and any departure from this approach would draw attention.

During the question-and-answer session, listen for commentary on Apple Intelligence adoption rates, iPhone upgrade trends, China demand conditions, and any updates on regulatory developments affecting the App Store. These qualitative inputs often matter more than the headline numbers for shaping the medium-term investment thesis.

Risk Factors Every Investor Should Evaluate

Macroeconomic and Market-Level Risks

Recession risk represents the most significant macro headwind for AAPL. Consumer electronics purchases are discretionary by nature, and iPhone sales historically decelerate during economic downturns as households prioritize essential spending. Rising interest rates compound this risk by elevating the discount rate applied to future cash flows, which pressures valuation multiples across the technology sector. Currency fluctuations also affect reported results, as a strengthening dollar reduces the value of revenue earned in euros, yuan, yen, and other foreign currencies.

Company-Specific Challenges

Apple’s manufacturing concentration in a small number of Asian countries creates operational vulnerability to geopolitical disruption, natural disasters, and pandemic-related supply chain interruptions. While the company has begun diversifying production toward India and Vietnam, the transition is gradual and will take years to reduce concentration risk meaningfully. Regulatory actions targeting App Store commission rates in the EU, US, and other jurisdictions represent a structural threat to Services margins. Executive succession planning, though not an immediate concern, warrants monitoring given the outsized influence of the current leadership team on strategic direction and operational execution.

How to Buy Apple Stock: A Practical Step-by-Step Walkthrough

Selecting a Brokerage Platform

Choosing the right brokerage platform is the first practical step toward purchasing AAPL shares. Commission-free trading is now standard across major retail brokerages, so the differentiating factors are research tools, platform reliability, mobile app quality, and customer service responsiveness. Taxable brokerage accounts offer the most flexibility, while Individual Retirement Accounts provide tax-deferred or tax-free growth depending on the account type.

Order Types and Position Management

Market orders execute immediately at the best available price, which is appropriate for a highly liquid stock like AAPL in most situations. Limit orders allow you to specify the maximum price you are willing to pay, which is useful when entering a position around a specific support level. For position sizing, a widely accepted guideline is to limit individual stock positions to no more than five percent of total portfolio value, though this threshold should be adjusted based on your personal risk tolerance, investment horizon, and overall diversification.

Dollar-cost averaging is a particularly effective strategy for building an Apple position over time. By investing a fixed dollar amount at regular intervals, you automatically purchase more shares when the price dips and fewer when it rises, which smooths your average cost basis across market cycles.

Frequently Asked Questions About Fintechzoom Apple Stock

What ticker symbol does Apple trade under?

Apple trades under the symbol AAPL on the NASDAQ exchange. This ticker is used across all brokerage platforms, financial news websites, and market data terminals.

Does Apple pay a dividend?

Yes. Apple pays a quarterly cash dividend and has increased the payout each year since reinstating dividends in 2012. The current yield is modest relative to income-oriented sectors, but the growth rate has been strong.

When does Apple report earnings?

Apple typically reports quarterly results in late January, late April, late July, and late October. Exact dates vary slightly each year and are confirmed on Apple’s Investor Relations website.

Is Apple stock overvalued at current prices?

Valuation is relative and depends on your assumptions about future growth. Apple’s P/E ratio is above historical averages, but proponents argue that the expanding Services segment and Apple Intelligence growth justify a premium multiple.

How much money do I need to buy Apple stock?

Most major brokerages now support fractional share purchases, which means you can invest any dollar amount regardless of the current share price. Fractional shares receive proportional dividend payments just like whole shares.

Should I buy Apple stock in 2026?

This depends entirely on your individual financial situation, investment goals, and risk tolerance. The analysis in this guide provides the data framework for making an informed decision. Consider consulting a licensed financial advisor for personalized recommendations.

Final Assessment and Actionable Next Steps

Apple remains one of the highest-quality businesses available on public markets. The ecosystem moat, Services growth trajectory, capital return discipline, and Apple Intelligence optionality combine to create a stock that can serve as a foundational portfolio holding for investors across risk profiles. The Fintechzoom Apple Stock analysis presented here supports a constructive outlook for 2026, with the caveat that position sizing and entry timing should always reflect individual circumstances.

For investors ready to act, the practical next steps are clear. Open a brokerage account if you do not already have one. Start with a modest position and consider adding to it through dollar-cost averaging over the next several quarters. Set price alerts at the support and resistance levels discussed in the technical analysis section. Monitor quarterly earnings reports for validation of the growth thesis, and be prepared to reassess if the fundamental picture changes materially.

Above all, make decisions based on data rather than headlines. The financial markets reward disciplined investors who do their homework, and this guide is designed to be one of your primary homework tools for AAPL.