FintechZoom IBM stock is trading near $248 per share as of March 2026. For many investors, that price tag raises an immediate question: is this blue-chip technology company worth owning right now? Search traffic for fintechzoom IBM stock grows every month, which tells you that retail investors are actively looking for a clear, consolidated answer, not scattered data across a dozen sites.

This guide gives you exactly that. We cover IBM’s 2026 price targets, dividend health, key growth drivers, competitive position, and the risks that could derail returns. Whether you are a first-time investor curious about IBM or a seasoned portfolio manager looking to re-evaluate an existing position, the analysis here is built to support a real decision.

FintechZoom IBM Stock sits at an interesting crossroads in 2026. The company is executing a genuine shift toward artificial intelligence and hybrid cloud services, while its legacy infrastructure business continues to generate reliable cash flow. That combination creates a different kind of investment story than most technology stocks, one that rewards patience more than momentum.

Five questions frame this entire analysis: What price do analysts expect IBM to reach in 2026? Is the dividend safe? Which business segments are actually driving value? What are the biggest risks? And how does IBM compare to Microsoft and Oracle? Work through those five questions and you will have everything you need to make a well-informed decision.

💡 Pro Tip: Set a price alert at $230 for a potential entry point and at $270 as a signal to reassess your position — it saves you from watching the screen all day.

FintechZoom IBM Stock: The Real Challenges Facing IBM Investors in 2026

IBM is not a straightforward buy. Before looking at the upside, it is worth being honest about why many investors stay on the sidelines.

Mixed Analyst Signals Create Confusion

Wall Street is genuinely divided on IBM right now. Some analysts rate it a strong buy while others recommend holding and trimming. For a retail investor trying to make sense of it all, that disagreement is frustrating rather than helpful.

The stock price reflects that uncertainty. IBM shares moved between $218 and $285 over the past twelve months, a $67 range on a stock that many people associate with stability. That kind of volatility makes timing an entry point difficult, especially for investors who are newer to equity analysis.

There is also a perception problem. IBM still carries a ‘legacy tech’ label in many corners of the market, even though its business today looks quite different from what it was a decade ago. That outdated narrative suppresses the multiple investors are willing to pay, which keeps valuation lower than fundamentals might otherwise support.

Revenue Growth Lags Behind Tech Peers

IBM is projecting around five percent revenue growth for 2026. In isolation that sounds reasonable, but the technology sector is averaging closer to twelve percent. When growth-hungry capital allocates across the sector, it tends to flow toward names delivering two or three times that rate.

Cloud competition amplifies the problem. Microsoft Azure, Amazon Web Services, and Google Cloud all invest at a scale IBM cannot match. That means IBM must win enterprise clients on specialisation and service quality rather than breadth and price, which is a harder sell in competitive procurement cycles.

Artificial intelligence is the variable that could change this calculus, but the monetisation timeline remains unclear. IBM’s Watsonx platform is gaining traction, but converting early enterprise interest into meaningful revenue takes time. The market is watching that translation closely.

💡 Pro Tip: Compare IBM’s five percent growth against the twelve percent sector average before finalising your allocation — the gap matters for valuation multiples.

Information Gaps Frustrate Individual Investors

One of the most common complaints about IBM investment research is fragmentation. Quality analysis exists, but it is spread across analyst reports, earnings transcripts, and dozens of financial websites. Assembling a complete picture takes hours that most investors simply do not have.

Dividend safety is a prime example. The question ‘Can IBM sustain its dividend?’ comes up constantly, yet clear answers, payout ratio, free cash flow coverage, historical growth rate, are surprisingly hard to find in one place.

Business segment performance creates similar confusion. IBM reports results across software, consulting, and infrastructure separately. Understanding which segments drive shareholder value and which are in decline requires manual calculation that goes beyond what most financial summary pages provide.

What Smart Investors Actually Need — and What the Data Shows

Here is what a well-grounded IBM investment thesis looks like when you work through the key questions systematically.

Price Targets: Where Analysts See IBM Heading

Based on thirty-four analyst estimates, the Wall Street consensus price target for IBM sits at $318 per share — implying roughly twenty-eight percent upside from the current $248 level. That is a material gap between price and consensus value.

The range is wide, which reflects genuine disagreement. Bull case scenarios push toward $390, built on assumptions of accelerating AI adoption, strong Red Hat performance, and expanding software margins. Bear case scenarios cluster around $218, reflecting concern about growth execution and competitive pressure from larger cloud rivals.

Neither extreme is the base case. Most analysts land somewhere in the $280 to $340 corridor, contingent on IBM continuing to show measurable progress on its strategic initiatives each quarter.

💡 Pro Tip: Track the consensus price target monthly on fintechzoom IBM stock pages — analyst revisions after earnings often move the stock before mainstream media coverage catches up.

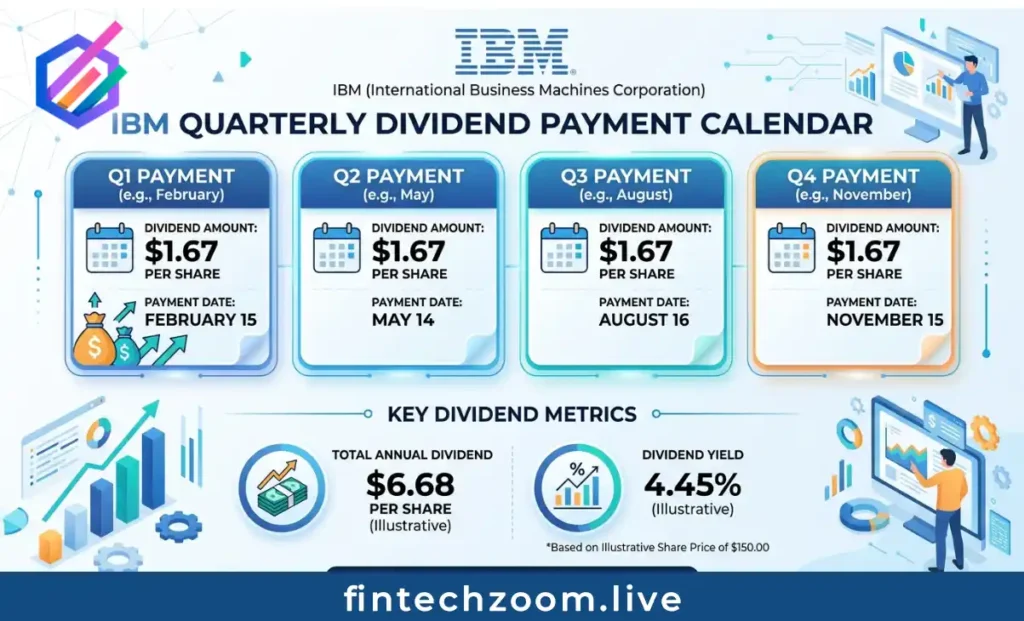

Dividend Analysis: Income You Can Count On

IBM currently yields approximately four percent annually, more than double the S&P 500 average. For income-focused investors, that yield is one of IBM’s clearest competitive advantages as an investment.

The payout ratio sits at around sixty-five percent of earnings. That is not a dangerously stretched number. It leaves enough room for IBM to continue growing the dividend while still funding its strategic investments in AI and hybrid cloud. Free cash flow coverage confirms this, FintechZoom IBM Stock targets $15.7 billion in free cash flow for 2026, well above what is needed to sustain dividend payments.

Perhaps the most compelling data point for income investors is longevity. IBM has raised its dividend for over twenty-five consecutive years, which qualifies it as a dividend aristocrat. That track record reflects management’s commitment to shareholders across bull markets, recessions, and business model transitions alike.

💡 Pro Tip: Reinvesting dividends automatically compounds your returns meaningfully over a multi-year holding period without requiring additional capital.

Business Segments: What Is Actually Driving Value

IBM’s software division is the engine of growth in 2026, largely driven by Red Hat’s hybrid cloud platform. This segment grows faster than the rest of the business and carries higher margins than consulting or infrastructure.

The consulting segment provides steady, recurring revenue and strong client relationships. It does not excite growth investors, but it generates reliable cash flow and helps IBM maintain deep enterprise relationships that support cross-selling of software and AI products.

Infrastructure revenue continues to decline on a unit basis, but the pace of decline has slowed. IBM has been fairly transparent about this transition, and the market has largely priced it in. What matters more now is whether software growth can more than offset infrastructure contraction, and so far, it can.

FintechZoom IBM Stock in 2025: A Year-in-Review

Understanding what happened last year helps contextualise where IBM stands today.

Price Performance and Key Catalysts

IBM shares traded between $218 and $285 during 2025. The full-year range tells a story of a market working through uncertainty about IBM’s transition pace while ultimately awarding modest gains to shareholders who held through the volatility.

The biggest single catalyst was the Q2 2025 earnings report, which pushed shares near the $285 high on the back of better-than-expected software revenue and an upward revision to free cash flow guidance. Q3 produced the opposite effect — a guidance disappointment sent shares back toward $220, where technical support held on elevated volume.

For investors paying attention to technical levels, the $215 zone acted as reliable support throughout the year. The $280 area capped each rally attempt until a stronger fundamental catalyst arrives to break through it.

Earnings Beat Pattern and Management Credibility

IBM exceeded earnings estimates in three of four quarters in 2025. That consistency — while not perfect — marks a meaningful improvement from prior years when guidance misses were more frequent.

The pattern that stands out is management’s improving guidance accuracy. Rather than setting aggressive targets and falling short, IBM leadership provided realistic ranges that the business then exceeded. In a market that punishes guidance misses harshly, that shift in communication style has started to rebuild investor confidence.

💡 Pro Tip: Look at eight consecutive quarters of earnings surprises before drawing conclusions about execution quality — one or two quarters either way can be noise.

Total Returns Including Dividends

IBM delivered a total return of approximately twelve percent in 2025 when dividend payments are included. That outcome outpaced the S&P 500 by about three percentage points during the same period.

The composition matters: roughly eight percentage points came from price appreciation and four from dividend income. For conservative and income-oriented investors, that four-point dividend contribution provided meaningful downside cushion during volatile stretches. For growth-focused investors comparing IBM to NVIDIA or other AI plays, the twelve percent total return looked modest, which is exactly why IBM suits different portfolios than high-multiple growth stocks.

Competitive Context: IBM vs. Microsoft and Oracle

No stock analysis is complete without understanding where a company sits relative to its direct competitors.

IBM vs. Microsoft

Microsoft is the most common comparison because both companies sell enterprise software and cloud infrastructure. Microsoft wins on scale — Azure is significantly larger than IBM’s cloud business, and Microsoft’s AI integration through Copilot reaches further across its product suite.

IBM competes differently. Its Red Hat platform targets hybrid cloud environments where enterprises run workloads both on-premises and in public cloud. That specific use case is actually growing faster than pure public cloud adoption in some regulated industries, which gives IBM a defensible niche.

On valuation, IBM trades at a meaningful discount to Microsoft. Microsoft’s growth premium justifies a higher multiple, but for investors seeking technology exposure without paying a top-of-market price, IBM’s valuation makes the comparison interesting.

IBM vs. Oracle

Oracle is the closer peer in terms of enterprise database and cloud infrastructure positioning. Both companies are navigating a transition from legacy on-premises revenues toward cloud-based recurring subscription models.

Oracle has executed that transition more aggressively and has been rewarded with a higher valuation multiple. IBM’s dividend yield advantage is significant in this comparison — Oracle yields less than one percent, while IBM sits near four percent.

The investor type that chooses IBM over Oracle generally prioritises income and stability. The investor who chooses Oracle is betting on faster cloud transition execution and greater capital appreciation. Both are defensible positions depending on your investment objectives and time horizon.

Key Risks Every IBM Investor Should Understand

A balanced investment thesis acknowledges what could go wrong.

- Competitive pressure from Microsoft, Amazon, and Google — all of which invest more heavily in cloud infrastructure — could limit IBM’s ability to grow market share, particularly outside its hybrid cloud niche.

- Technology transition execution risk remains real. IBM is in the middle of shifting from a hardware-and-services company to a software-and-AI company. Missteps during that transition — whether in product development, enterprise sales execution, or capital allocation — could dampen financial results.

- Economic sensitivity affects enterprise technology spending broadly. In a recessionary environment, corporate customers delay or reduce cloud and AI investments, which would weigh on IBM’s revenue growth and potentially put pressure on the dividend payout ratio.

- AI monetisation timeline uncertainty is the most speculative risk. IBM has made substantial bets on Watsonx and quantum computing. If those platforms take longer than expected to generate meaningful revenue, growth projections will require downward revision.

💡 Pro Tip: Position IBM at three to five percent of a diversified portfolio — enough to benefit from upside while limiting exposure to execution risk.

Frequently Asked Questions

What is the FintechZoom IBM Stock price target for 2026?

The consensus Wall Street price target is $318 per share, based on estimates from thirty-four analysts. That implies approximately twenty-eight percent upside from the current $248 trading level. High estimates reach $390 and low estimates sit at $218, reflecting a genuine range of views on IBM’s growth execution.

Does IBM pay a dividend?

Yes. IBM pays quarterly dividends with a current yield near four percent annually. Payments are distributed in March, June, September, and December. IBM has raised its dividend for over twenty-five consecutive years and carries dividend aristocrat status. The payout ratio of approximately sixty-five percent supports continued payment without straining free cash flow.

Is FintechZoom IBM Stock undervalued right now?

At a forward P/E of approximately twenty-one times earnings, IBM trades below the technology sector average of twenty-six times. Discounted cash flow models suggest fair value in the $280 to $340 range, pointing to modest undervaluation at current prices for investors with a twelve-to-eighteen month time horizon.

What are the main risks of investing in IBM?

The primary risks are competitive pressure from larger cloud providers, uncertainty around AI monetisation timelines, execution risk during the ongoing business model transition, and cyclical sensitivity to enterprise technology spending in a potential economic slowdown.

Next Steps: How to Put This Analysis to Work

Immediate Actions Worth Taking

Set price alerts at the $230 support level and the $270 resistance level. These two levels have been consistent reference points for entry and exit timing over the past year. Alerts let you respond when prices move without requiring constant monitoring.

Add IBM’s next earnings date to your calendar and review the free cash flow and software segment results specifically. Those two data points are the most reliable indicators of whether IBM’s strategic transition is on track.

Review your overall technology allocation before adding IBM. If you already hold significant Microsoft or Oracle positions, adding IBM increases sector concentration. Consider IBM as a complement to, rather than a replacement for, other technology holdings.

Further Resources on FintechZoom

The fintechzoom IBM stock hub provides real-time price data, analyst rating summaries, earnings calendars, and segment performance breakdowns in one place. Related analysis covers Microsoft, Oracle, and other enterprise technology peers for comparative research.

The broader Markets section of FintechZoom provides context on interest rate trends and economic indicators that directly influence how the market values technology stocks. Macro awareness consistently improves individual stock timing decisions.