An in-depth look at Hussman’s hedged equity approach, fund-by-fund performance data, fee comparisons, and a practical guide for investors considering downside protection in today’s market.

Introduction to Hussman Funds

Hussman Funds represents one of the most distinctive investment approaches available to retail and institutional investors today. Founded by John Hussman, Ph.D., the firm operates on a philosophy rooted in valuation-driven analysis and active hedging strategies designed to protect capital during market downturns. For investors navigating the elevated valuations and economic uncertainty of 2026, understanding how these funds work has never been more relevant.

The firm currently manages three mutual funds, each serving a different purpose within a diversified portfolio. The Strategic Market Cycle Fund (formerly Strategic Growth Fund, ticker: HSGFX) focuses on hedged equity positions. The Strategic Total Return Fund (HSTRX) manages a flexible bond portfolio. The Strategic Allocation Fund (HSAFX) blends stocks and bonds dynamically based on market conditions.

This review covers the full scope of what prospective investors need to evaluate: the underlying investment philosophy, historical performance across bull and bear markets, the fee structure relative to alternatives, and a step-by-step guide to purchasing these funds through major brokerage platforms. Every section is written to help you determine whether Hussman Funds deserves a place in your portfolio.

💡 Pro Tip: Read the latest weekly market commentary on hussmanfunds.com before making any investment decision. Hussman publishes his positioning and market outlook every Monday.

Why Traditional Approaches Fall Short

Market Volatility and Portfolio Risk

Stock market investors face a fundamental challenge: traditional buy-and-hold strategies provide no mechanism for limiting losses during sharp downturns. When the S&P 500 dropped 37 percent in 2008, retirement accounts across the country lost years of accumulated growth in a matter of months. Recovery took more than five years for many portfolios, and investors who sold near the bottom locked in permanent damage.

The mathematics of drawdowns compounds the problem. A 50 percent portfolio loss requires a 100 percent gain just to return to the starting point. This asymmetry means that avoiding severe declines can matter as much as capturing gains during rising markets. For investors within a decade of retirement, a major crash at the wrong time can fundamentally alter financial plans.

Consider this: If your portfolio dropped 40 percent tomorrow, how would that affect your retirement timeline, your income needs, and your willingness to stay invested? These are the questions that make downside protection strategies worth examining.

Valuation Risks Heading Into 2026

Market valuations in 2026 remain stretched by most historical standards. The cyclically adjusted price-to-earnings ratio (CAPE), popularized by Yale professor Robert Shiller, sits well above its long-term average. Market capitalization relative to GDP, a measure Warren Buffett has called his preferred valuation gauge, continues to signal elevated risk. Meanwhile, bond yields, while higher than the near-zero levels of 2020 through 2021, still offer modest real returns for conservative investors.

Hussman’s own research consistently highlights that above-average starting valuations correlate with below-average future returns over ten-year horizons. Passive index investors entering the market at today’s prices may face disappointment compared to historical norms. This is the environment where active, valuation-aware strategies offer their strongest conceptual advantage.

📊 Pro Tip: Compare current market valuations to historical averages using the Shiller CAPE ratio data, available free on Professor Robert Shiller’s website at Yale.

How Hussman Funds Addresses These Challenges

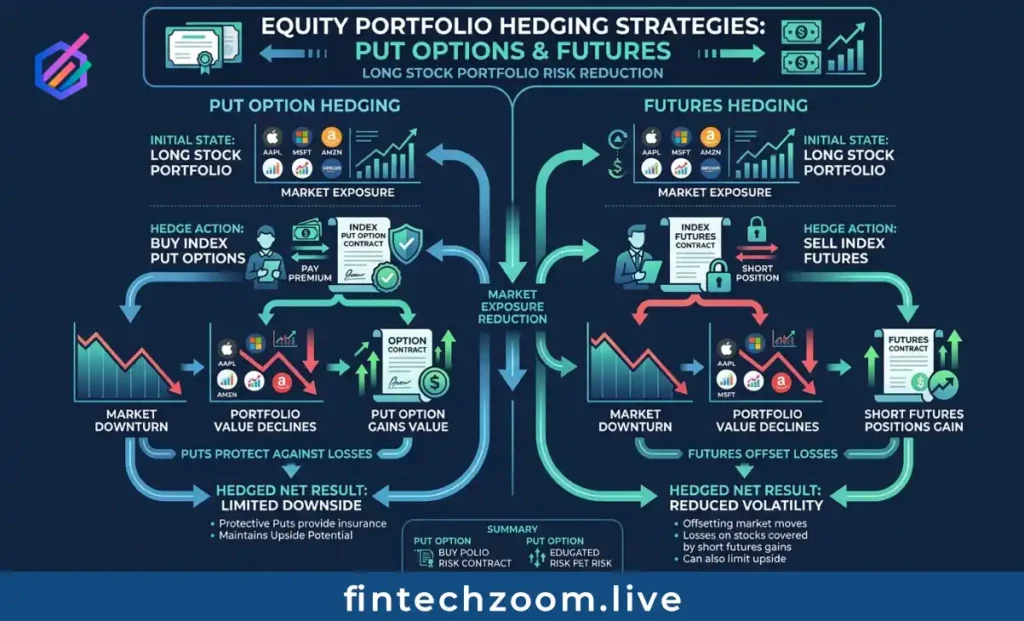

The Hedged Equity Strategy

The Strategic Market Cycle Fund employs a distinctive approach: it holds a diversified portfolio of individual stocks while simultaneously using index put options and futures contracts to hedge against broad market declines. When Hussman’s valuation models and market internals indicators signal elevated risk, the fund can reduce its net market exposure to near zero. When conditions appear more favorable, the hedge is reduced to increase equity participation.

Market internals play a central role in the timing framework. Technical breadth, measured by the uniformity of advances across different sectors and stock types, serves as a confirmation signal alongside valuation analysis. This dual framework reduces the chance of acting on false signals from either measure alone. Hussman developed this refined approach after studying patterns from the late 1990s technology bubble.

A defining feature of the firm is its transparency. Every week, Hussman publishes a detailed market commentary explaining his current positioning, the data behind his decisions, and his outlook. Investors are never left guessing about what the fund is doing or why.

Bond and Allocation Fund Alternatives

The Strategic Total Return Fund (HSTRX) takes an active approach to fixed-income investing. Rather than holding a static bond allocation, the fund adjusts its duration exposure based on interest rate conditions. Treasury securities form the core of the portfolio, with tactical additions of utility stocks and REITs when yield opportunities arise. This active duration management aims to protect against rising rates while capturing income during favorable conditions.

The Strategic Allocation Fund (HSAFX) offers a one-fund solution that dynamically shifts between stocks and bonds based on valuation signals. For investors who prefer simplicity over managing multiple positions, this fund handles the asset allocation decision internally. Assets under management remain smaller than the equity and bond funds, reflecting more limited investor adoption so far.

Key Benefits of Hussman Funds

Capital Preservation During Bear Markets

The primary advantage of the Hussman approach is downside protection when markets decline sharply. During the 2008 financial crisis, the Strategic Growth Fund (now the Strategic Market Cycle Fund) declined just 9.02 percent while the S&P 500 lost 37 percent. That 28 percentage point difference preserved significant capital that would have taken years to recover through a passive strategy.

This protection comes with a clear trade-off. During extended bull markets, hedging costs reduce returns relative to unhedged index funds. From 2010 through 2019, the fund underperformed the S&P 500 by a wide margin as markets climbed steadily with only shallow corrections. This is not a flaw in the strategy but rather the expected cost of the insurance it provides.

For investors who prioritize portfolio stability and sleep-at-night confidence over maximum gains, this trade-off may be acceptable. The key question is whether you can tolerate years of relative underperformance in exchange for protection during the next significant decline.

Full Market Cycle Performance

Hussman designs his funds to outperform over complete market cycles, not arbitrary calendar periods. A complete cycle includes both a bull phase and a bear phase. Evaluating the fund solely during a decade-long bull run misses the point of the strategy entirely.

Trailing ten-year returns remain negative through 2025, reflecting the longest bull market in history that followed the 2009 lows. However, the fund’s performance during crisis periods like 2008 and 2022 demonstrates the strategy executing as intended. Patient investors who understand the cyclical nature of this approach and who entered before a significant decline have seen the benefits firsthand.

🎯 Pro Tip: Evaluate Hussman Funds over complete market cycles rather than isolated three-year or five-year windows. The strategy is designed for full-cycle investing, not year-to-year comparisons.

Performance During Market Crises: 2008 and 2022

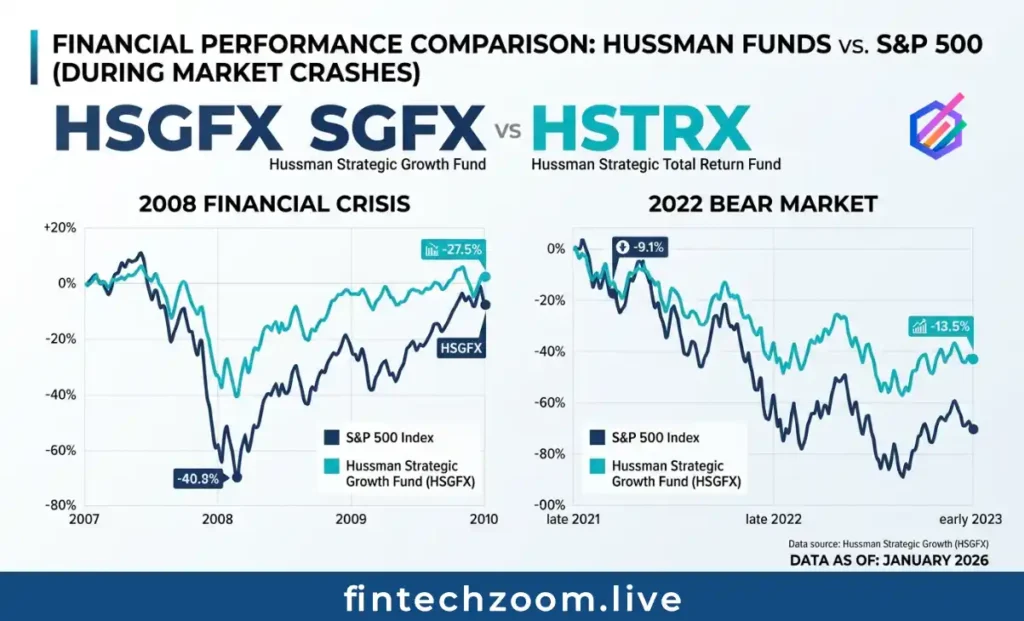

The 2008 Financial Crisis

The 2008 financial crisis remains the defining test for any defensive investment strategy. As global markets collapsed under the weight of subprime mortgage failures and banking sector insolvency, the S&P 500 fell 37 percent for the calendar year. Category averages for equity mutual funds exceeded 29 percent in losses.

Hussman’s Strategic Growth Fund declined just 9.02 percent that year. The hedging positions, built up as valuation and market internals deteriorated throughout 2007, absorbed much of the market’s decline. Investors who held the fund preserved capital that passive strategies simply could not.

The 2022 Inflation-Driven Decline

The year 2022 brought a different kind of stress test. Rising inflation, aggressive Federal Reserve rate hikes, and a correction in speculative growth stocks pushed the S&P 500 down 18.11 percent. The Strategic Market Cycle Fund gained 17.32 percent that year, generating profits as equity values fell. The hedging positions performed exactly as designed.

Crisis Period Performance Comparison

| Year | HSGFX Return | S&P 500 Return | Difference |

| 2008 | -9.02% | -37.00% | +27.98% |

| 2022 | +17.32% | -18.11% | +35.43% |

| 2010–2019 Avg | -1.50% | +13.50% | -15.00% |

What Investors Can Learn

Investors who held through both crisis periods and the intervening bull market experienced the full character of this strategy: significant protection during declines paired with relative underperformance during advances. The lesson is straightforward. Behavior determines outcomes as much as the fund’s strategy. Investors who abandoned the fund during the 2010 through 2019 underperformance period missed the 2022 recovery. Those who stayed committed saw the strategy deliver precisely what it promised.

Understanding your own behavioral tendencies matters here. If you would sell after three years of lagging the S&P 500, this fund is probably not suited to your temperament, regardless of its protective value.

Hussman Funds Versus the Alternatives

How It Compares to Index Funds and ETFs

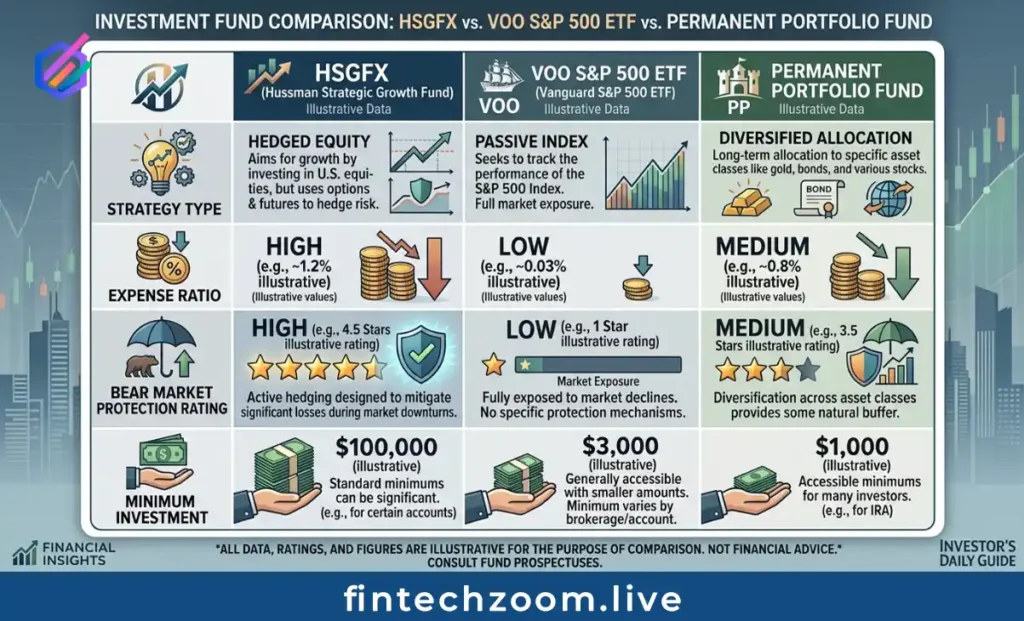

Index funds offer market exposure at rock-bottom costs. The Vanguard S&P 500 ETF (VOO) charges just 0.03 percent annually, compared to approximately 1.15 percent for the Strategic Market Cycle Fund. On cost alone, passive funds win decisively.

The case for Hussman rests entirely on risk management. Index funds provide zero downside protection. During bear markets, you absorb the full decline. Hedged equity ETFs do exist as alternatives, but most employ static hedging approaches that do not adjust based on market conditions the way Hussman’s valuation-driven model does.

Fund Comparison Overview

| Feature | HSGFX | VOO (S&P 500 ETF) | Permanent Portfolio |

| Strategy | Hedged Equity | Passive Index | Multi-Asset |

| Expense Ratio | 1.15% | 0.03% | 0.82% |

| Bear Market Defense | Strong | None | Moderate |

| Minimum Investment | $1,000 | Share Price | $1,000 |

| Turnover | High (400%+) | Low (3–4%) | Moderate |

| Best For | Defensive Investors | Long-Term Growth | Conservative Blend |

Fee Structure and Value Assessment

All three Hussman funds operate as no-load mutual funds, meaning there are no sales commissions or front-end charges. The minimum initial investment is $1,000 across all funds, with subsequent contributions accepted at $100. These are reasonable thresholds compared to many actively managed alternatives.

When evaluating fees, context matters. The long-short equity fund category carries higher average expenses than passive index funds due to the research and trading costs inherent in active hedging. Whether those fees represent good value depends entirely on how the next market cycle unfolds. In a sustained bull market, the fees drag on returns. In a bear market, the protection they fund can more than justify the cost.

Tax efficiency is one area where Hussman funds fall short for taxable accounts. Portfolio turnover rates exceeding 400 percent generate substantial capital gains distributions annually. For this reason, holding these funds in tax-advantaged accounts like IRAs or 401(k) plans is strongly recommended.

How to Buy Hussman Funds: A Step-by-Step Guide

Account Setup and Minimum Requirements

Purchasing Hussman Funds requires an active brokerage account. If you already hold investments through Fidelity, Schwab, Vanguard, or similar platforms, you likely have immediate access. New investors will need to open an account first, which typically involves providing identification, linking a bank account, and completing a brief suitability questionnaire.

The minimum initial investment across all three funds is $1,000. After your first purchase, subsequent investments can be as low as $100. Automatic investment plans are available for those who prefer to contribute on a regular schedule.

For tax optimization, consider placing these funds in an IRA account. Traditional IRAs defer taxes on gains until withdrawal during retirement. Roth IRAs allow tax-free growth and qualified distributions. Given the high turnover and resulting capital gains distributions, tax-sheltered accounts provide a meaningful advantage.

Brokerage Platform Availability

Major discount brokerages including Fidelity, Charles Schwab, Vanguard, and TD Ameritrade all carry Hussman Funds. Some platforms may charge transaction fees for mutual fund purchases, so check your specific broker’s fee schedule before buying.

Direct purchases are also available through the Hussman Funds website at hussmanfunds.com. The site provides current prospectus documents, monthly performance updates, and the weekly market commentary that serves as the fund’s primary investor communication channel.

Frequently Asked Questions

General Investor Questions

What happens if John Hussman retires?

Succession planning is a legitimate concern. The firm has not announced detailed transition plans, and John Hussman’s personal involvement drives the investment methodology. This key-person risk is inherent in any manager-dependent fund. Monitor the firm’s communications for updates on leadership continuity.

Is this strategy appropriate for buy-and-hold investors?

Only if your time horizon extends at least ten years and you can tolerate extended periods of underperformance during bull markets. The fund targets complete market cycle returns, not short-term outperformance. Align your expectations with the fund’s design before committing capital.

How does the hedging mechanism work in practice?

The fund purchases index put options that increase in value when the market declines. Futures contracts further offset long equity exposure when the model calls for reduced risk. At full hedging, net market exposure approaches zero, limiting both losses and gains from broad market movements.

Tax and Retirement Account Questions

Can I hold Hussman Funds in retirement accounts?

Yes. IRA and most 401(k) plans accept Hussman Funds. Check your specific employer-sponsored plan for fund availability. IRA custodians at major brokerages generally offer all three funds.

What are the tax implications for taxable accounts?

Annual capital gains distributions create tax liabilities regardless of whether you sell shares. Turnover rates above 400 percent in the equity fund generate significant short-term and long-term gains. Tax-loss harvesting across other positions can offset some of this impact, but retirement accounts remain the preferred vehicle.

How can I track fund performance?

Brokerage statements display current holdings and values. Morningstar and Yahoo Finance provide free, updated performance data. The Hussman Funds website publishes monthly fact sheets and the weekly commentary provides ongoing context about positioning and market outlook.

Next Steps for Investors

Before making any changes to your portfolio, take an honest look at your current allocation, risk tolerance, and investment timeline. Hussman Funds is not a replacement for a core equity allocation. It serves as a defensive satellite position within a diversified portfolio, designed to reduce overall volatility and protect against severe declines.

A reasonable starting allocation ranges from five to fifteen percent of your total portfolio. Begin with a small position to test your comfort level with the fund’s behavior during both rising and falling markets. Keep your core holdings in low-cost index funds and use Hussman as a complement, not a substitute.

Recommended actions: Read at least four recent weekly commentaries to understand Hussman’s current market view. Download the prospectus for each fund you’re considering. Consult a financial advisor if you need personalized guidance on how defensive positioning fits your unique circumstances.

Visit hussmanfunds.com for the most current fund information, performance data, and market analysis. Your financial future benefits from informed, deliberate decision-making.