The Income That Looks Better Than It Is

In the last 90 days alone, investors put nearly $2 billion into one NEOS ETF. That number should tell you something. NEOS funds have become one of the most talked-about names in income investing for 2026. Promises of 12 to 37 percent monthly yields have pulled in retirees, income seekers and ordinary investors at a pace few ETF issuers have ever matched.

But here is the question you should ask before you put a single dollar in: is that income real?

This review of NEOS funds gives you a plain and honest answer. We cover every major fund in the NEOS lineup, explain how the options strategy actually works, show you what return of capital means in real dollar terms and tell you exactly who these funds suit and who should stay away. No jargon and no hype.

❓ Are the 12 to 37 percent yields from NEOS funds real income or just your own money coming back to you?

💡 Pro Tip: Before reading any ETF’s distribution rate, always check the 30-Day SEC Yield first. For SPYI, that figure is just 0.52 percent while the distribution rate is 12 percent. That gap tells you most of the story.

What Are NEOS Funds?

The Plain-English Answer (150 words)

NEOS Investments is an asset management firm founded in 2022 and headquartered in Westport, Connecticut. The company was built by a team that has spent decades working on options-based investment strategies. Its full name, NEOS, stands for Next Evolution Option Strategies.

NEOS funds are actively managed ETFs that do one main thing: they hold stocks or other assets and sell call options on top of those holdings to collect monthly option premiums. Those premiums get passed to investors as monthly distributions. That is the core of the business.

As of early 2026, NEOS manages 19 ETFs spanning equities, bonds, Bitcoin, Ethereum, gold, energy and international markets. The firm won two major industry awards in 2025: ETF.com Best New Active ETF for QQQI and Best Options Strategies ETF Issuer from ETF Express U.S.

The NEOS flagship fund SPYI now holds $6.3 billion in assets. That kind of growth from a firm launched just four years ago is remarkable and tells you how much demand exists for this type of income product.

❓ How does selling call options on an index actually generate monthly income for ordinary investors?

How the NEOS Options Strategy Works

Covered Calls in One Minute (200 words)

A call option gives someone the right to buy an asset at a set price before a set date. When NEOS sells a call option, it collects a cash payment called a premium upfront. In exchange, the fund agrees to cap its gains above a certain price level for the life of that option.

For example, imagine NEOS holds S&P 500 stocks worth $100 and sells a call option at a $105 strike. If the market rises to $108, the fund gains only up to $105 and not beyond. But it keeps the premium it collected. That premium becomes your monthly distribution.

Why NEOS Uses Index Options Instead of Stock Options (150 words)

Most covered call ETFs sell options on individual stocks. NEOS sells options on broad indexes like the SPX (S&P 500 Index) and NDX (Nasdaq-100 Index). This one difference matters enormously for your taxes.

Index options fall under Section 1256 of the US tax code. That means any gains are taxed at a 60 percent long-term rate and 40 percent short-term rate regardless of how long you held them. Standard stock options are taxed at full short-term rates. For investors in higher brackets this distinction can save thousands per year.

💡 Pro Tip: If you hold NEOS funds in a taxable brokerage account, the Section 1256 treatment on SPX and NDX options gives you a meaningful tax advantage versus most competing covered call ETFs. However, if you are not a US taxpayer, you do not get this benefit at all.

The Call Spread Approach: How NEOS Keeps Upside Potential (150 words)

NEOS goes one step further than simple covered calls. Instead of just selling a call and capping all upside, it uses some of the premium collected to buy a higher-strike call option. This creates a call spread. The result is that the fund retains some ability to benefit from market rallies while still collecting income.

This is why SPYI managed a 19.00 percent total return over the past 12 months including distributions. A plain covered call fund would have capped more of that upside. The active management team adjusts the spread structure based on market conditions, volatility levels and income targets.

❓ If NEOS captures more upside than a standard covered call ETF, why do some analysts still prefer simpler index funds for long-term growth?

The Full NEOS ETF Lineup 2026

All 19 Funds at a Glance (200 words)

The table below covers all current NEOS ETFs as of March 2026. Distribution rates are approximate and based on recent declared distributions. They are not guaranteed.

| Ticker | Fund Name | Focus | Mgmt Fee | Dist. Rate | Frequency |

| SPYI | S&P 500 High Income ETF | S&P 500 Equities | 0.68% | ~12.0% | Monthly |

| QQQI | Nasdaq-100 High Income ETF | Nasdaq-100 Equities | 0.68% | ~14.0% | Monthly |

| IWMI | Russell 2000 High Income ETF | Small-Cap Equities | 0.68% | Varies | Monthly |

| BTCI | Bitcoin High Income ETF | Bitcoin ETPs | 0.98% | ~28%+ | Monthly |

| NEHI | Ethereum High Income ETF | Ethereum ETPs | 0.98% | ~34.83% | Monthly |

| IAUI | Gold High Income ETF | Gold ETPs | 0.78% | ~12.2% | Monthly |

| MLPI | MLP & Energy Infrastructure ETF | MLPs / Energy Infra | 0.68% | ~14.9% | Monthly |

| NIHI | MSCI EAFE High Income ETF | Intl Equities | 0.68% | Varies | Monthly |

| HYBI | High Yield Bond Income ETF | High Yield Bonds | 0.68% | Varies | Monthly |

| BNDI | Bond High Income ETF | Broad Bonds | 0.58% | Varies | Monthly |

| CSHI | Cash Alternative ETF | T-Bills / Cash | 0.38% | Varies | Monthly |

| TLTI | Long-Term Treasury Income ETF | Long-Duration Treas. | 0.58% | Varies | Monthly |

| SPYH | S&P 500 Hedged Equity Income ETF | S&P 500 + Hedge | 0.68% | Varies | Monthly |

| QQQH | Nasdaq-100 Hedged Equity Income ETF | Nasdaq + Hedge | 0.68% | Varies | Monthly |

| IYRI | Real Estate High Income ETF | REITs | 0.68% | ~10.92% | Monthly |

| NLSI | Leveraged Short Income ETF | Short / Leveraged | 0.98% | Varies | Monthly |

| XSPI | Boosted S&P 500 High Income ETF | S&P 500 (150% Exp.) | 0.98% | 15-18% | Weekly/Monthly |

| XQQI | Boosted Nasdaq-100 High Income ETF | Nasdaq-100 (150% Exp.) | 0.98% | 19-23% | Weekly/Monthly |

| XBCI | Boosted Bitcoin High Income ETF | Bitcoin (150% Exp.) | 0.98% | Higher | Weekly/Monthly |

Source: NEOSFunds.com, BusinessWire distribution announcements, March 2026. All distribution rates are approximate and subject to change.

NEOS Flagship ETFs: Deep Dives

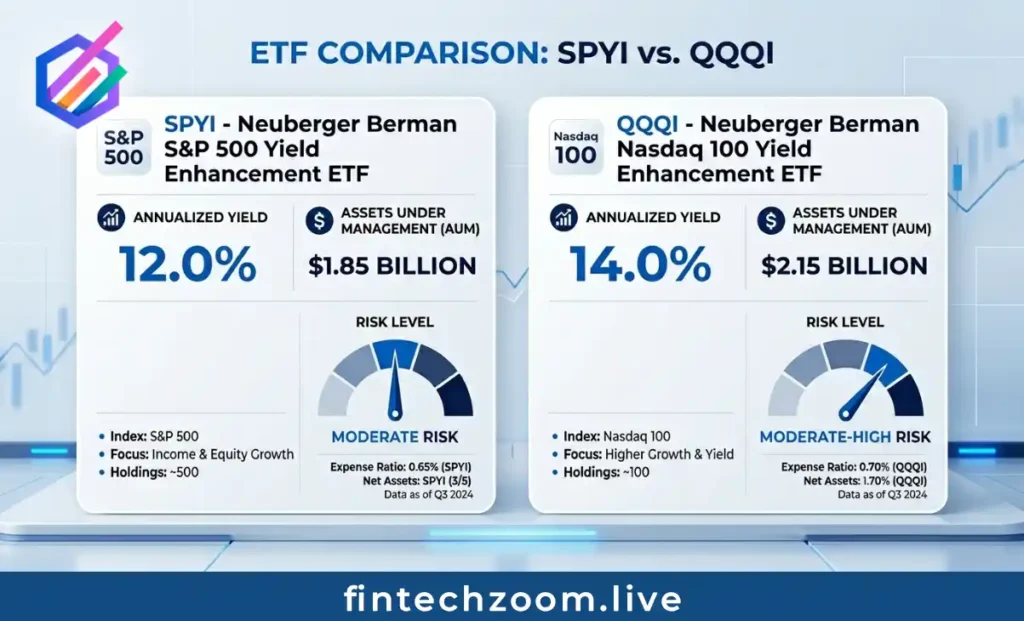

SPYI: The $6.3 Billion Flagship Fund (250 words)

SPYI is the largest NEOS ETF by a wide margin. It launched in August 2022 and has grown to $6.3 billion in assets as of March 2026. Over the past three months alone investors added $1.87 billion in new capital. That pace of inflows is extraordinary for any fund in any category.

SPYI holds a portfolio of stocks that track the S&P 500 and layers an SPX call spread strategy on top. The fund targets a distribution rate of 10 to 12 percent per year. In 2025 SPYI achieved a 17.31 percent total return with 94 percent of distributions classified as return of capital.

The fund’s beta is 0.69 against the broader market. That means it is 31 percent less volatile than the S&P 500 while still capturing a meaningful share of upside. Its 12-month total return of 19.00 percent and average annual return since inception of 13.50 percent place it well above most traditional income alternatives.

Key Metric SPYI’s 30-Day SEC Yield as of late 2025 was just 0.52 percent. The distribution rate was approximately 12 percent. That 11.5 percentage point gap is nearly all return of capital, not income.

QQQI: Higher Yield, More Tech Exposure (200 words)

QQQI launched in January 2024 and focuses on the Nasdaq-100 Index. It holds roughly 80 percent of its NAV in Nasdaq-100 stocks and sells NDX index call options to generate income. The fund has a distribution rate of approximately 14 percent and a 30-Day SEC Yield of just 0.02 percent.

That gap between 14 percent and 0.02 percent is the single most important number in this entire review. Nearly all of QQQI’s distributions are return of capital driven by capital appreciation and tax-loss harvesting rather than genuine investment income.

QQQI delivered a 23.14 percent total return over the past 12 months including distributions. Since inception its average annual return has been 17.47 percent. Those are strong numbers. But they came during one of the best two-year runs in Nasdaq history. Investors should consider what these figures might look like during a prolonged tech downturn.

QQQI’s maximum drawdown has reached negative 20 percent at one point compared to SPYI’s negative 16.47 percent. The tech concentration means more upside in bull markets and more pain when growth stocks fall.

SPYI vs JEPI: The Real Comparison

Side-by-Side Data Table (150 words)

NEOS funds are often compared to JPMorgan’s JEPI and JEPQ. The table below shows how they stack up on the key metrics that actually matter for income investors.

| Fund | Ticker | Strategy | Approx Yield | Expense Ratio | Options Type | Tax Sec 1256? |

| NEOS S&P 500 High Income | SPYI | Active SPX call spread | ~12% | 0.68% | Index options | Yes |

| NEOS Nasdaq-100 High Income | QQQI | Active NDX call spread | ~14% | 0.68% | Index options | Yes |

| JPMorgan Equity Premium Income | JEPI | ELN-based covered call | ~7-8% | 0.35% | Equity-linked notes | No |

| JPMorgan Nasdaq Equity Premium | JEPQ | ELN-based covered call | ~9-10% | 0.35% | Equity-linked notes | No |

| Goldman S&P 500 Premium Income | GPIX | Active covered call | ~6-8% | 0.29% | Stock options | No |

| Goldman Nasdaq-100 Premium | GPIQ | Active covered call | ~8-10% | 0.29% | Stock options | No |

Source: Public fund disclosures, ETFdb.com and StockAnalysis.com data as of early 2026. For informational comparison only. Not investment advice.

SPYI and QQQI offer higher headline yields and a genuine tax advantage through Section 1256 contracts. JEPI and JEPQ offer lower expense ratios and potentially more stable distributions because they use equity-linked notes rather than direct index options. SPYI captured 98 percent of S&P 500 upside in 2025 whereas JEPI typically captures less in strong bull markets.

The right choice depends on your tax bracket and income goal. If you are in the 32 percent federal bracket or above and hold funds in a taxable account, SPYI’s Section 1256 treatment likely makes up for the higher expense ratio versus JEPI.

💡 Pro Tip: Run a simple tax comparison before choosing between SPYI and JEPI. Take the yield difference, apply your marginal tax rate to both income types, and add back the expense ratio savings from JEPI. Many investors in higher brackets will find SPYI comes out ahead on an after-tax basis.

Return of Capital: The Most Important Thing You Need to Understand

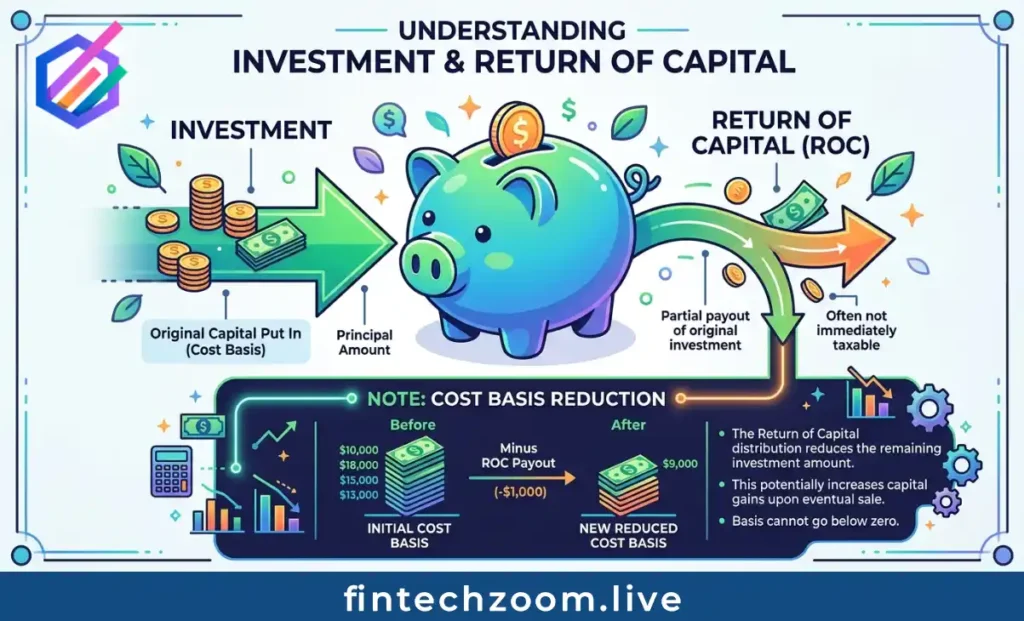

What ROC Actually Means for Your Money (200 words)

Return of capital is not income. When a fund classifies a distribution as return of capital, it is giving you back a portion of your own invested money rather than paying you from earnings, dividends or option premiums. This has two direct consequences that every investor must grasp.

First, your cost basis in the fund goes down. If you invested $10,000 in SPYI and received $500 in ROC distributions, your cost basis falls to $9,500. When you eventually sell your shares, capital gains taxes are calculated from that lower number.

Second, ROC distributions are not taxed in the year you receive them. That tax is deferred until you sell, which can be genuinely useful for investors who want to delay their tax liability.

But here is the risk: if the fund’s market value does not grow enough to offset the distributions it pays out, NAV will erode over time. In a flat or declining market you may find yourself holding a fund worth less than you started with while having received distributions that are largely just your own capital returned to you.

| NEOS ETF | Estimated ROC % (Most Recent Distribution) |

| SPYI | ~98% |

| QQQI | ~99-100% |

| IWMI | ~100% |

| BTCI | ~96% |

| NEHI | ~97% |

| IAUI | ~93% |

| MLPI | ~86% |

| HYBI | ~62% |

| BNDI | ~70% |

| CSHI | ~67% |

| TLTI | ~67% |

Source: NEOS Investments / BusinessWire February 2026 distribution announcement. ROC percentages vary month to month.

Reality Check A 12 percent distribution rate does not mean the fund earns 12 percent annually. If 98 percent is return of capital, only 2 percent represents genuine investment income. SPYI’s 30-Day SEC Yield of 0.52 percent is a far more honest measure of actual income generation.

Section 1256 Tax Treatment: Real Savings With a Catch

The 60/40 Rule Explained With Real Numbers (200 words)

Section 1256 of the US tax code applies to certain financial contracts including SPX and NDX index options. Under this rule, any gains from these contracts are taxed as 60 percent long-term capital gains and 40 percent short-term capital gains regardless of how long you held them.

Here is why that matters in dollars. Say you are in the 32 percent federal bracket and earn $10,000 from option income. Under standard short-term rates you owe $3,200 in tax. Under Section 1256 the blended rate works out to roughly 23.8 percent on the combined 60/40 split, leaving you owing around $2,380 instead. That is over $800 saved on $10,000 in income.

NEOS Funds also actively harvests tax losses throughout the year by selling positions at a loss and using those losses to offset gains elsewhere in the fund. This is one reason such a high proportion of distributions end up classified as return of capital rather than taxable income.

Two important warnings: Section 1256 treatment applies only to US investors. And return of capital defers your tax bill but does not eliminate it. When you sell your shares you will owe capital gains taxes on a lower cost basis.

❓ Should you hold NEOS funds inside a Roth IRA where distributions grow tax-free or in a taxable account where the Section 1256 advantage applies?

The NEOS Boosted ETF Suite: XSPI, XQQI and XBCI

What 150 Percent Notional Exposure Actually Means (200 words)

In February 2026 NEOS launched three Boosted ETFs: XSPI for the S&P 500, XQQI for the Nasdaq-100 and XBCI for Bitcoin. These funds build on the same options framework as SPYI, QQQI and BTCI but target 150 percent notional exposure to their underlying markets.

That means if the S&P 500 rises 10 percent, XSPI aims to participate as if it held 1.5 times the index. XSPI targets 15 to 18 percent annualized distributions and XQQI targets 19 to 23 percent. Those numbers are higher than the core funds because the greater notional exposure generates larger option premiums.

The leverage here works differently from daily-reset leveraged ETFs like ProShares 2x funds. NEOS Funds achieves the 150 percent exposure by buying index call options and selling index put options at similar strike prices rather than borrowing money or using daily swaps. This means you do not get the volatility decay that kills daily-reset products over time.

But make no mistake: these are not conservative products. Losses are amplified when markets fall. NEOS states clearly that relatively small market movements can result in large changes in the value of leveraged positions and that losses may potentially exceed the initial amount invested in adverse scenarios.

Warning XSPI, XQQI and XBCI are not suitable for conservative investors. They carry amplified downside risk and should only be considered by investors with a high risk tolerance and a clear understanding of leveraged options structures.

BTCI: Bitcoin Income Without Directly Holding Bitcoin

How a 28 Percent Yield Is Possible and What It Costs You (150 words)

BTCI does not hold Bitcoin directly. Instead it invests in Bitcoin exchange-traded products and sells call options on top to collect premium income from Bitcoin’s famously high volatility. High volatility means large premiums and large premiums mean high distribution rates. That is how a 28 percent yield is possible.

BTCI launched in October 2024 and surpassed $700 million in AUM within its first year. That is remarkable growth. But the underlying asset can fall 50 to 80 percent within a single market cycle. Option premiums provide some income buffer but they do not meaningfully protect against a deep Bitcoin correction.

The NEOS Ethereum High Income ETF NEHI works the same way with Ethereum and carries an even higher distribution rate of approximately 34.83 percent as of February 2026. It is worth noting that 97 percent of NEHI distributions are return of capital.

Consider BTCI and NEHI only if you have a strong existing view on Bitcoin and Ethereum and you understand that high income here comes directly from high risk rather than from a stable earnings stream.

The Real Risks of NEOS Funds

Seven Risks Every Investor Must Understand (250 words)

NEOS funds can play a useful role in the right portfolio. But they carry risks that many investors underestimate, especially when they focus only on the headline yield.

- Capital erosion risk. In flat or declining markets, high distributions that are largely return of capital can reduce NAV over time. You may be receiving your own money back while the fund shrinks.

- Capped upside in bull markets. Selling call options limits how much the fund gains when markets rise sharply. In 2025 SPYI captured most but not all of the S&P 500’s upside. In a stronger bull run the gap would be larger.

- Options strategy complexity. Active management adds costs and decisions that purely passive index funds avoid. Strategy adjustments depend on management judgment which introduces uncertainty.

- Bitcoin and crypto volatility for BTCI, NEHI and XBCI. Bitcoin has historically fallen 30 to 80 percent within single market cycles. Premium income does not fully offset losses of that size.

- Leveraged ETF risk for XSPI, XQQI and XBCI. Amplified losses when markets fall. Losses may exceed the original investment in severe scenarios.

- Return of capital misunderstanding. Investors who spend distributions freely without understanding the cost basis reduction are quietly depleting their own investment base.

- Distribution fluctuation. NEOS Funds does not guarantee a fixed monthly payment. Distributions change based on option premium income, market conditions and management decisions.

❓ If option premiums fall during a low-volatility period, how much can NEOS distribution rates drop and has that happened before?

Who Should Invest in NEOS Funds and Who Should Not

Investor Profiles and Suitability Guide (200 words)

NEOS funds are not one-size-fits-all products. The table below gives honest guidance based on investor profile.

| Investor Profile | Fit with NEOS Funds | Key Consideration |

| Income-focused retirees (with caution) | Moderate fit | Understand ROC mechanics. Do not rely on NEOS as sole income source. |

| Tax-conscious investors in higher brackets (32%+) | Good fit | Section 1256 and ROC treatment may reduce tax bill significantly in taxable accounts. |

| Investors seeking equity income alternatives | Good fit | SPYI and QQQI complement equity allocations with monthly income overlay. |

| Portfolio diversifiers (non-correlated income) | Moderate fit | IAUI gold and MLPI energy funds add income from less S&P 500-correlated sources. |

| Aggressive income seekers comfortable with high risk | Conditional fit | BTCI, NEHI and Boosted suite offer highest yields but carry substantial downside risk. |

| Conservative investors seeking capital preservation | Poor fit | Limited downside protection and NAV erosion risk make these unsuitable. |

| Buy-and-hold long-term total return investors | Poor fit | Capped upside will underperform SPY or QQQ significantly in a multi-year bull market. |

How to Buy NEOS ETFs: A Step-by-Step Guide

Getting Started in Five Steps (150 words)

NEOS Funds ETFs trade on US stock exchanges and are available through most major brokerage platforms including Fidelity, Charles Schwab, TD Ameritrade, E*TRADE and Interactive Brokers. You do not need a minimum account size beyond the cost of one share.

Step one: Open a brokerage account if you do not already have one. Step two: Fund the account with the amount you want to invest. Step three: Search for the ticker symbol of the NEOS ETF you want, for example SPYI or QQQI. Step four: Place a limit order at or near the current market price rather than a market order to control your execution price. Step five: After purchase, set up a plan for how you will handle distributions and whether you want to reinvest them.

A note on account type: holding NEOS funds inside a Roth IRA removes all tax considerations since distributions grow and can be withdrawn tax-free. This is worth considering if you qualify, though you give up the Section 1256 advantage that only applies in taxable accounts.

💡 Pro Tip: Use a limit order rather than a market order when buying NEOS ETFs. Some of the smaller funds in the lineup have wide bid-ask spreads during low-volume periods. A limit order set at the NAV price protects you from overpaying.

The 2026 Distribution Schedule Change

Weekly Income: How the New Staggered System Works (120 words)

In February 2026 NEOS Funds restructured its distribution payment schedule across the full lineup. Different fund families now pay in different weeks of the month. The Boosted ETFs XSPI, XQQI and XBCI pay in week one. Other fund families are staggered across weeks two through four.

For investors who hold a diversified basket of NEOS ETFs across multiple families, this staggered approach means it is possible to receive a distribution payment every week of the month rather than once monthly. That can help with cash flow planning for investors who rely on portfolio income to cover regular expenses.

Frequently Asked Questions

Are NEOS Funds Safe Investments?

No NEOS fund is risk-free. All funds carry the risk of loss of principal. Equity funds can lose value in market downturns and the options strategy does not fully protect against losses. Boosted ETFs carry amplified downside risk. These funds are appropriate for investors willing to accept meaningful volatility who clearly understand the options-based income strategy.

What Is the Difference Between Distribution Rate and 30-Day SEC Yield?

The distribution rate is the annualized rate based on the most recent monthly payment divided by NAV. The 30-Day SEC Yield is the fund’s actual net investment income calculated using an SEC-mandated formula over a 30-day period. For SPYI the distribution rate is approximately 12 percent but the SEC yield is just 0.52 percent. The gap is almost entirely return of capital.

Are NEOS Distributions Guaranteed?

No. NEOS explicitly states there is no guarantee the ETFs will make monthly distributions and that amounts may fluctuate from month to month. Distributions depend on option premium income generated, which varies with market volatility and management decisions. A sustained period of low VIX could reduce distributions noticeably.

Is NEOS SPYI a Good Investment for Retirees?

SPYI can be a useful component of a retirement income portfolio for investors who understand what return of capital means and who are not relying solely on SPYI for living expenses. The beta of 0.69 and the 11 to 12 percent distribution rate make it attractive. However, using it as a sole income source creates NAV erosion risk over a long retirement.

How Do NEOS Funds Compare to JEPI?

SPYI offers a higher yield and Section 1256 tax efficiency. JEPI offers a lower expense ratio and uses equity-linked notes rather than direct options, which may result in more stable distributions in low-volatility markets. SPYI has outperformed JEPI in total return over the 2022 to 2025 period. The best choice depends on your tax situation and income needs.

❓ If you held $100,000 in SPYI for five years with all distributions reinvested, would you end up with more or less than $100,000 in a flat market?

The Honest Verdict on NEOS Funds in 2026

NEOS funds represent a genuinely well-designed approach to income investing. The options strategy is sophisticated, the tax structure is thoughtful and the performance record since 2022 is strong. SPYI’s 19 percent total return over the past 12 months and QQQI’s 23.14 percent are real numbers that income-focused investors should pay attention to.

But the headline yields deserve scrutiny. A 12 percent distribution rate sounds nothing like a 0.52 percent SEC yield and both figures describe the same fund. Most of what NEOS pays you monthly is your own capital returning, not income from the market. That is not a fraud and in the right tax situation it is genuinely useful. But it means these funds work best as one piece of a diversified income strategy rather than a standalone solution.

For investors who understand return of capital, appreciate the Section 1256 tax advantage and have a specific income role in mind for these ETFs, NEOS funds are worth serious consideration. For investors focused purely on long-term total return, a simple index fund will likely outperform in a sustained bull market where capped upside becomes a real cost.

Always read the fund prospectus, understand the distribution policy section and speak with a qualified tax professional before investing. NEOS ETFs are not FDIC insured and carry risk of loss of principal.