Energy as geopolitical weapon 2026 has evolved from a tactical disruption into a structural force that is reshaping inflation trajectories, equity valuations, and central bank policy across every major economy. In 2022, Russia’s invasion of Ukraine triggered an energy price shock that sent Brent crude above $106 per barrel and pushed the NASDAQ down 4% in a single month. Lloyds Banking Group, however, gained 2% during that same window, an early signal that domestically focused banks could absorb external commodity volatility. Four years later, the Middle East conflict has disrupted roughly 20% of global oil and LNG flows through the Strait of Hormuz, sending oil futures toward $100 per barrel and forcing the IMF to revise global inflation forecasts upward.

The difference between 2022 and 2026 lies in permanence. The 2022 shock was severe but bounded; European gas storage refilled, alternative suppliers emerged, and inflation peaked within eighteen months. The 2026 shock is embedded in a multipolar landscape where supply chains for fertilizers, chemicals, and critical minerals face simultaneous pressure. This article offers forward-looking analysis, 2026-2030 projections, and actionable strategies for investors who need to position portfolios around energy-driven volatility. We examine why select financial institutions, particularly Lloyds Bank, demonstrate durable resilience through higher net interest margins and domestic lending strength, even as headline inflation reaccelerates.

5 Key Takeaways

- Energy as geopolitical weapon 2026 has produced the largest oil supply shock on record through Strait of Hormuz disruptions, with energy prices projected to surge 24% this year.

- Global headline inflation is expected to rise to 4.4% in 2026 under the IMF reference forecast, with adverse scenarios pushing inflation above 6% and global growth below 2%.

- Lloyds Banking Group has upgraded its 2026 return on tangible equity target to greater than 16%, supported by net interest income guidance of approximately £14.9 billion and structural hedge tailwinds.

- UK domestic banks benefit from higher-for-longer interest rates that widen net interest margins, even as energy as geopolitical weapon 2026 pressures household budgets and mortgage demand.

- Investors should balance energy equities and commodity exposure with selective bank positions, while monitoring AI-driven electricity demand as an emerging structural wildcard through 2030.

From 2022 Russia Gas Cutoffs to 2026 Strait of Hormuz Crisis – The Evolution of Energy Weaponization

Energy as geopolitical weapon 2026 represents a fundamental escalation from the isolated supply cutoffs seen in 2022. The 2026 Middle East conflict inflicts damage that exceeds the Russia-Ukraine shock in both scale and persistence, confirming that commodity markets have become permanent battlefields.

Historical Parallel – 2022 Energy Shock Recap

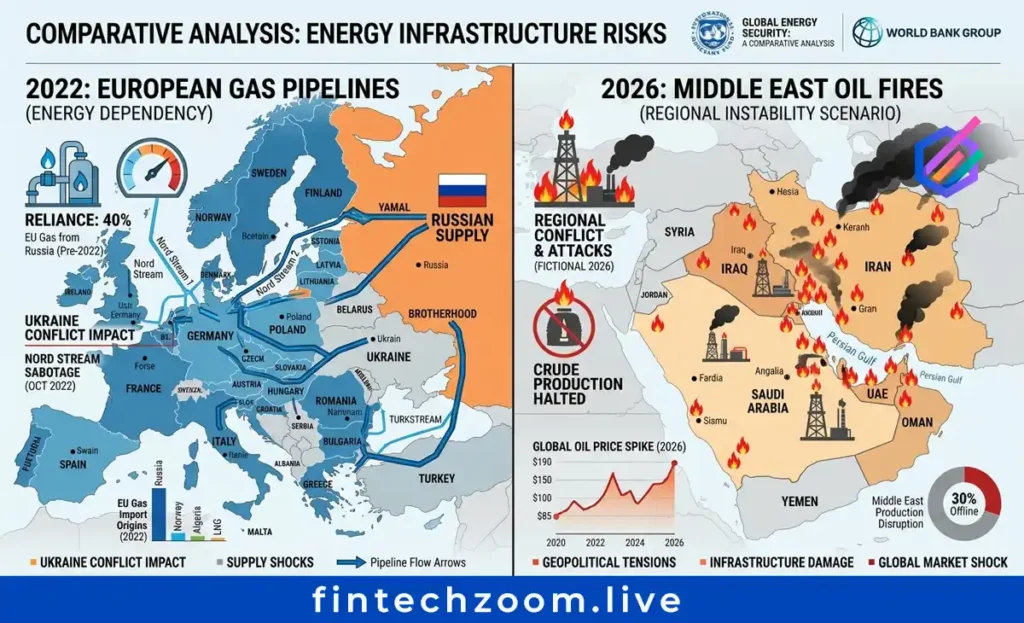

In April 2022, Russia halted natural gas deliveries to Poland and Bulgaria after those countries refused Moscow’s demand for ruble-denominated payments. Brent crude surged above $106 per barrel within weeks, and European electricity prices hit record levels. Wall Street responded with broad liquidation as recession fears mounted, yet early signals suggested that UK-focused banks like Lloyds could weather the storm. Buoyant housing markets and rising take-home pay, driven by pandemic-era savings and tight labor markets, supported mortgage origination and consumer credit quality through much of 2022.

The 2022 shock was primarily a gas crisis concentrated in Europe, offering an early preview of energy as geopolitical weapon 2026 dynamics. LNG cargoes rerouted from Asia to Europe, coal plants received temporary lifelines, and North Sea production provided partial relief. Inflation peaked but proved cyclical; by late 2023, energy prices had normalized and central banks began signaling rate cuts, though none anticipated energy as geopolitical weapon 2026 would soon eclipse those disruptions. The episode demonstrated that energy could be used as a tactical weapon, but the global economy possessed sufficient redundancy to absorb the blow within twelve to eighteen months. Energy as geopolitical weapon 2026 operates differently because the disruptions are simultaneous, global, and embedded in a fragmented geopolitical order.

2026 Reality – Middle East Conflict Reshapes Global Energy Flows

The February 2026 outbreak of war in the Middle East introduced a fundamentally different geometry to energy markets. Attacks on energy infrastructure and shipping disruptions in the Strait of Hormuz, which handles about 35% of global seaborne crude oil trade and 20% of liquefied natural gas, triggered the largest oil supply shock on record according to the International Energy Agency. An initial reduction in global oil supply of roughly 10 million barrels per day sent Brent prices more than 50% higher by mid-April compared to January levels.

The coordinated release of 400 million barrels from IEA emergency reserves highlighted the scale of the disruption, yet oil futures remained volatile in the $80 to $100 per barrel range as markets priced in sustained energy as geopolitical weapon 2026 risk premia. The U.S. Energy Information Administration now forecasts Brent crude to average $96 per barrel in 2026, up sharply from prior estimates of $79, before moderating to $76 in 2027. Unlike 2022, the 2026 shock affects oil and LNG simultaneously, hitting Asian manufacturing economies and European gas-dependent power systems at the same time. Energy as geopolitical weapon 2026 manifests through this dual-channel disruption that leaves no major economy insulated.

Why Energy Weaponization Is Now the New Normal

Energy as geopolitical weapon 2026 has become a permanent feature of great-power competition rather than an exception. The post-Cold War assumption of stable, rules-based commodity flows has given way to a multipolar order where supply chains for fertilizers, chemicals, and metals face systematic disruption. About one-third of global fertilizer shipments pass through the Strait of Hormuz, raising food price risks alongside fuel costs.

Russia’s 2022 gas cutoff proved that energy could influence political behavior; the 2026 Hormuz crisis proves that energy can destabilize entire economic regions without a single shot fired at the attacker, cementing energy as geopolitical weapon 2026 in the global consciousness. Fragmented globalization amplifies these risks because spare capacity is lower, strategic reserves are finite, and alternative routing options are limited. The repetition of energy as geopolitical weapon 2026 across multiple conflicts confirms that commodity markets have become permanent battlefields. Investors must now treat energy geopolitics as a baseline condition, not a tail risk.

2026–2030 Inflation and Economic Projections: Energy as Geopolitical Weapon 2026 Drives Global Forecasts

The IMF projects global growth of 3.1% in 2026 and headline inflation of 4.4%, with energy prices representing the single largest variable that could push those figures into adverse or severe territory. Energy as geopolitical weapon 2026 sits at the center of every major forecast revision.

IMF World Economic Outlook (April 2026) Key Figures

The April 2026 World Economic Outlook presents a reference forecast predicated on limited conflict duration, alongside two scenarios reflecting escalating disruption. Under the reference case, global growth slows to 3.1% in 2026 and 3.2% in 2027, while headline inflation rises to 4.4% this year before easing to 3.7% next year. These figures already embed a 0.2 percentage point downward revision to growth and a 0.7 percentage point upward revision to inflation compared with pre-conflict assumptions.

The adverse scenario assumes larger and more persistent energy price increases, with oil and gas prices jumping 80% and 160% respectively from baseline levels under extended energy as geopolitical weapon 2026 conditions. Global growth would drop to 2.5% in 2026 and inflation would reach 5.4%. In the severe scenario, oil prices double and remain elevated into 2027, averaging approximately $110 per barrel this year and $125 next year. Global growth would fall to roughly 2% and inflation would climb above 6% by 2027, bringing the world close to recession conditions seen only during the global financial crisis and the COVID-19 pandemic. Energy as geopolitical weapon 2026 scenarios are now the primary risk factor in every major macroeconomic model.

IEA and Commodity Outlooks

The World Bank Commodity Markets Outlook forecasts overall commodity prices to rise 16% in 2026, driven by a 24% surge in energy costs and record-high prices for several base metals. Fertilizer prices are projected to increase 31%, driven by a 60% jump in urea prices, eroding farm incomes and threatening crop yields. If the conflict persists, up to 45 million additional people could face acute food insecurity this year.

EU electricity futures are trading near USD 95 per MWh for 2026 delivery, with expectations of moderation to around USD 85 per MWh in 2027 as storage rebuilds and demand management takes effect, though energy as geopolitical weapon 2026 could delay this moderation. Oil demand growth continues modestly despite elevated prices, supported by Asian industrial activity and limited short-term elasticity in transport fuels. Rare-earth and critical mineral frictions add secondary pressure, with copper, aluminum, and tin prices reaching all-time highs on demand from data centers, electric vehicles, and renewable energy infrastructure.

Beyond 2026 – Structural Shifts

Artificial intelligence and data center expansion represent a new wildcard for energy demand. Electricity consumption in accelerated servers, driven primarily by AI adoption, is projected to grow 30% annually through 2030, with AI workloads accounting for almost half of the net increase in global data center electricity use. In the United States, data centers are expected to account for almost half of projected electricity demand growth between 2026 and 2030.

This surge collides with the clean-energy shift timeline, adding complexity to energy as geopolitical weapon 2026 response strategies. Accelerated renewable build-out is necessary to meet both climate targets and baseline demand growth, yet persistent fossil dependency in conflict zones and developing economies complicates the path. The result is a structural tension: clean energy investment must rise faster to offset both geopolitical supply risks and AI-driven demand increments. Energy as geopolitical weapon 2026 dynamics add urgency to every infrastructure decision.

Stock Market Reactions in 2026 – Volatility, Sector Rotation, and Resilience Signals

Equity markets have sold off on inflation fears while energy stocks rallied, but the banking sector has emerged as an unexpected beneficiary of higher-for-longer interest rates. Energy as geopolitical weapon 2026 has created clear sector winners and losers.

Immediate Market Impact

The initial weeks of the Middle East conflict produced sharp equity drawdowns, rising bond yields, and a pronounced shift toward volatility instruments. Technology and cyclical sectors faced margin compression as input costs rose and consumer discretionary spending came under pressure. Energy exporters outperformed importers by a wide margin, with the divergence between commodity-rich and commodity-dependent economies reaching levels not seen since the 1970s oil crises.

Energy stocks benefited from the short-term price spike, yet the sustainability of those gains depends on how long energy as geopolitical weapon 2026 disruptions persist. The World Bank notes that even after transit resumes, higher risk premia and uncertainty may curb investment and growth in producing regions. For importers, the shock functions as a sudden tax on income, reducing corporate profitability and household purchasing power simultaneously. Energy as geopolitical weapon 2026 has redistributed wealth from consumers to producers on a massive scale.

Banking Sector as Unexpected Winner

Higher-for-longer interest rates have widened net interest margins across the UK banking sector, and Lloyds Banking Group exemplifies this dynamic. The bank reported first-quarter 2026 net interest income of £3.57 billion, beating consensus estimates of £3.55 billion, with a banking net interest margin of 3.17%. This margin expansion reflects the Bank of England’s cautious stance on rate cuts amid reaccelerating inflation, a direct consequence of energy price pressures.

Lloyds has upgraded its full-year 2026 return on tangible equity target to greater than 16%, supported by net interest income guidance of approximately £14.9 billion and structural hedge income expected to reach £7 billion. The bank’s domestic focus insulates it from emerging market currency volatility and trade disruption, while its mortgage book benefits from stable UK employment and housing demand. Even as energy as geopolitical weapon 2026 rattles global markets, UK domestics generate predictable sterling-denominated returns.

FTSE 100 and Global Indices Outlook

Caution persists across global indices, yet the FTSE 100 has shown relative resilience due to its heavy weighting in energy majors and domestic banks, a pattern that energy as geopolitical weapon 2026 has reinforced. UK-focused institutions provide ballast against global volatility because their revenue streams are tied to sterling-denominated lending and deposit spreads rather than international trade finance. The divergence between energy exporters and importers is likely to widen further if the conflict extends beyond mid-2026, rewarding portfolios with exposure to North Sea production, UK utilities, and select financials.

Why Lloyds Bank Continues to Thrive Amid Energy as Geopolitical Weapon 2026 Turmoil

Lloyds Bank is outperforming because its domestic UK focus, structural hedge income, and rising net interest margins insulate it from the direct effects of energy import dependency and emerging market volatility. Energy as geopolitical weapon 2026 has not derailed its growth trajectory.

2025 Performance Recap and 2026 Analyst Consensus

Lloyds Banking Group delivered a standout 2025. Statutory profit after tax reached £4.8 billion, return on tangible equity hit 12.9% (14.8% excluding the motor finance provision), and tangible net asset value per share rose to 57 pence. The share price gained 79.3% during the year, and total shareholder return reached 87.9% when including dividends.

For 2026, management has guided to net interest income of approximately £14.9 billion, a cost-to-income ratio below 50%, and return on tangible equity greater than 16%. Analysts have responded with average twelve-month price targets around 113 to 114 pence, implying 14% to 16% upside from current levels. The bank intends to pay down its common equity tier 1 ratio to around 13% by year-end while returning excess capital through dividends and a £1.75 billion share buyback program. These targets hold firm even as energy as geopolitical weapon 2026 pressures the broader economy.

Key Resilience Drivers

Lloyds derives its strength from three structural advantages. First, its mortgage book grew £10.8 billion in 2025 to reach £323 billion, supported by a flow share of roughly 19% and resilient UK housing demand. Second, the structural hedge notional stood at £244 billion at year-end 2025, generating approximately £5.5 billion in income that is expected to step up to £7 billion in 2026 and £8 billion in 2027. This hedge income provides a predictable revenue base that is largely insulated from commodity price swings.

Third, Lloyds maintains a digital and AI program that scaled 50 generative AI use cases into production during 2025, generating £50 million in profit-and-loss benefit with expectations of more than £100 million in 2026. These efficiency gains help offset inflationary cost pressures and support the sub-50% cost-to-income target even if wage growth remains firm. Energy as geopolitical weapon 2026 cannot easily disrupt these internal efficiency drivers.

Risks and Mitigants for Lloyds and Peers

The primary risk facing UK domestic banks is a potential rise in bad loans if energy as geopolitical weapon 2026 pressures persist and unemployment ticks upward. Lloyds has guided to an asset quality ratio of approximately 25 basis points in 2026, up from 17 basis points in 2025, reflecting prudent provisioning. Capital generation is expected to exceed 200 basis points this year, providing a thick buffer against unexpected credit deterioration.

Peers face similar dynamics, though Lloyds benefits from its position as the UK’s largest digital bank with 23.6 million digitally active customers and a branch network optimized for cost efficiency. The bank’s commitment to provide £35 billion in new finance to UK companies in 2026 reinforces its domestic orientation and reduces exposure to international trade disruption. Energy as geopolitical weapon 2026 poses less threat to purely domestic lenders than to global trade finance institutions.

Investment Strategies for 2026 and Beyond – Managing Energy Geopolitics

Investors should hedge energy volatility through commodity exposure and gold, while maintaining selective positions in UK domestic banks and renewable infrastructure to capture margin expansion and structural growth. Energy as geopolitical weapon 2026 demands a multi-asset response.

Portfolio Hedging Tactics

Direct exposure to energy equities remains the most effective near-term hedge against geopolitical supply shocks. Integrated oil majors with low production costs and diversified geographic footprints offer defensive characteristics even if prices moderate in 2027. Diversified commodity baskets, including agriculture and base metals, protect against the fertilizer and food price spillovers that follow energy disruptions. Gold has broken price records in 2026, with average prices forecast to rise 42% this year as geopolitical uncertainty fuels safe-haven demand.

Selective bank exposure, particularly in UK domestics, offers a less obvious but equally important hedge. Higher-for-longer rates expand net interest margins without the currency risk attached to emerging market lenders. Lloyds, with its sub-50% cost-to-income target and RoTE above 16%, provides a sterling-denominated buffer against dollar volatility and energy import inflation. Portfolios constructed around energy as geopolitical weapon 2026 should include this banking exposure as a stabilizer.

Long-Term Themes

The renewable acceleration theme is intact but now intersects with critical mineral geopolitics. Copper, lithium, cobalt, and rare-earth elements face supply concentration risks that rival fossil fuel dependencies. The United States has advanced bilateral critical minerals partnerships with Australia, Japan, and Ukraine, while exploring price support mechanisms and a $2 billion stockpile expansion through the National Defense Stockpile Transaction Fund. Investors should favor companies with vertically integrated supply chains or offtake agreements in politically stable jurisdictions.

AI-energy infrastructure represents a parallel opportunity. Data center power demand is growing at 15% annually globally, with AI-specific server electricity consumption projected to rise 30% per year. Grid modernization, natural gas peaker plants, and utility-scale battery storage are necessary enablers for this expansion and will attract capital regardless of oil price direction.

Scenario Planning

Base case assumptions assume limited conflict duration with energy disruptions fading by mid-2026. Under this path, inflation bumps moderately but central banks avoid aggressive tightening. The adverse scenario involves persistent Hormuz closures and oil averaging $115 per barrel, pushing developing economy inflation to 5.8% and forcing rate hikes that deepen the growth slowdown.

The severe scenario, modeled by the IMF, assumes oil prices near $125 per barrel in 2027, inflation expectations de-anchoring, and corporate credit spreads widening 100 basis points in advanced economies. Portfolios should be stress-tested against all three paths, with liquidity buffers raised and equity allocations tilted toward domestic revenue exposure. Preparing for energy as geopolitical weapon 2026 requires more than tactical commodity trades; it demands structural portfolio adjustments that account for persistent inflation, higher rates, and fragmented supply chains.

Policy Responses and the Path to Energy Security Post-2026

Central banks face a balancing act between containing inflation and supporting growth, while governments accelerate diversification strategies and strategic reserve policies that acknowledge the limits of multilateral cooperation. Energy as geopolitical weapon 2026 has exposed the fragility of coordinated global responses.

Central banks entered 2026 with plans to cut rates; the energy shock has forced a reassessment. The Bank of England, Federal Reserve, and European Central Bank must now weigh sticky services inflation and rising energy costs against slowing output and tightening financial conditions. The IMF notes that in adverse scenarios, policy rates in advanced economies could rise 50 basis points by 2027, while emerging markets face larger increases.

Governments are responding with accelerated diversification. The United States is expanding LNG export capacity and exploring coordinated critical minerals trading frameworks with allied countries. The European Union is rebuilding gas storage and fast-tracking renewable permits, though its dependence on imported energy remains acute. Strategic petroleum reserves have been tapped, but inventories are finite and replacement purchases will eventually support prices.

Global cooperation faces structural headwinds. The multipolar era limits the effectiveness of joint sanctions, price caps, and supply agreements that worked during previous crises. Countries are prioritizing bilateral deals over multilateral frameworks, fragmenting energy markets into competing blocs. Investors should expect higher risk premia, more volatile term structures, and persistent inflation differentials between energy exporters and importers through 2030. Energy as geopolitical weapon 2026 has accelerated this fragmentation.

Conclusion – Energy Weaponization Is Here to Stay: Position for Resilience in 2026+

Energy shocks create clear winners and losers, and investors who position for resilience through domestic banks, commodity hedges, and scenario-based planning will outperform those who treat geopolitical risk as a temporary anomaly.

Energy as geopolitical weapon 2026 is not a fleeting headline but a permanent feature of the investment landscape. The IMF reference forecast assumes limited conflict duration, yet the probability that global growth falls below 2% remains elevated at 25%, while the probability that inflation exceeds 5% has jumped to 38%. These are not tail risks; they are base-case adjacencies that demand continuous portfolio attention.

The actionable takeaway is clear: energy shocks create winners alongside broad volatility. Resilient banks like Lloyds, with RoTE targets above 16% and structural hedge income approaching £7 billion, offer sterling-denominated stability. Energy equities, gold, and critical mineral supply chains provide inflation protection. The call to action is equally direct: monitor IMF and IEA updates monthly, stress-test portfolios against adverse and severe scenarios, and maintain liquidity to exploit dislocations when volatility spikes. Energy as geopolitical weapon 2026 rewards those who prepare today.

Frequently Asked Questions

What does energy as geopolitical weapon 2026 mean in practice?

It refers to the systematic use of energy supply disruptions, shipping blockades, and infrastructure attacks to achieve strategic political and economic objectives. The 2026 Middle East conflict demonstrates energy as geopolitical weapon 2026 through Strait of Hormuz closures that reduced global oil supply by 10 million barrels per day and sent energy prices surging 24%. Unlike accidental outages, these disruptions are deliberate tools of statecraft that weaponize commodity interdependence.

How does the 2026 Middle East conflict differ from the 2022 Russia-Ukraine energy shock?

The 2026 shock is larger, more persistent, and simultaneously affects oil, LNG, and fertilizer flows through a single chokepoint. In 2022, Russia cut gas to Poland and Bulgaria, causing a European-centric crisis that normalized within eighteen months. The 2026 Hormuz crisis affects 35% of seaborne crude and 20% of LNG globally, with the IMF modeling severe scenarios where oil averages $125 per barrel in 2027 and inflation exceeds 6%.

What are the latest IMF projections for global growth and inflation in 2026?

The IMF reference forecast projects 3.1% global growth and 4.4% headline inflation for 2026. These figures reflect a 0.2 percentage point growth downgrade and a 0.7 percentage point inflation upgrade from pre-conflict assumptions. Adverse scenarios drop growth to 2.5% and raise inflation to 5.4%, while severe scenarios approach 2% growth and 6% inflation.

Will oil prices stay above $80–100/barrel through 2027?

Under the base case, Brent averages $96 in 2026 and moderates to $76 in 2027, but adverse scenarios keep prices above $115. The EIA forecasts Brent at $96 per barrel this year, while the World Bank warns that sustained Hormuz closures could push averages to $115. Much depends on whether energy infrastructure damage extends beyond mid-2026.

Why is Lloyds Bank stock outperforming despite energy as geopolitical weapon 2026 inflation?

Lloyds benefits from higher UK interest rates that expand net interest margins, combined with structural hedge income and a domestic lending focus. The bank reported Q1 2026 net interest income of £3.57 billion and a banking net interest margin of 3.17%, beating consensus. Management guides to RoTE greater than 16% in 2026, supported by £7 billion in structural hedge income and a cost-to-income ratio below 50%.

How will higher energy prices affect UK mortgage demand and banking margins?

Mortgage demand remains resilient due to stable UK employment, while banking margins expand because the Bank of England keeps rates elevated to combat inflation. Lloyds grew its mortgage book by £10.8 billion in 2025 to £323 billion, reflecting continued housing demand. Higher rates widen the spread between what banks earn on loans and pay on deposits, directly benefiting net interest margins even if energy costs squeeze household budgets.

Which sectors offer the best hedging against geopolitical energy risks in 2026?

Energy equities, diversified commodities, gold, and UK domestic banks provide the most effective hedges. Gold prices are forecast to rise 42% in 2026 on safe-haven demand. Energy majors with low production costs benefit from elevated oil prices, while UK banks like Lloyds capture margin expansion from higher rates. Critical mineral supply chains offer a structural long-term hedge against fossil fuel dependency.

What role will AI and data centers play in future energy demand and prices?

AI-driven data centers will account for almost half of U.S. electricity demand growth through 2030 and are projected to grow global consumption by 15% annually. Accelerated server electricity use, driven by AI adoption, is projected to grow 30% per year. This adds a structural demand increment that competes with residential and industrial users for grid capacity, potentially keeping power prices elevated even if fossil fuel disruptions ease.

Should investors buy Lloyds Banking Group shares in 2026?

Analyst consensus supports a positive outlook, with average price targets of 113–114 pence implying 14% to 16% upside and a dividend yield supported by strong capital generation. Lloyds upgraded its 2026 RoTE target to greater than 16% and guides to net interest income of approximately £14.9 billion. The bank returns excess capital through dividends and a £1.75 billion buyback, though investors should monitor credit quality if energy as geopolitical weapon 2026 pressures persist.

How can retail investors prepare portfolios for prolonged energy volatility beyond 2026?

Retail investors should build diversified exposure across commodities, domestic banks, and gold while maintaining liquidity buffers and avoiding overconcentration in energy-importing emerging markets. Scenario planning is critical: base case assumptions suggest moderate inflation, while adverse scenarios require hedges against both equity drawdowns and currency depreciation. Regular rebalancing, exposure to renewable infrastructure, and avoidance of borrowed-capital commodity positions provide a robust framework for managing multi-year volatility driven by energy as geopolitical weapon 2026 dynamics.