FTSE 100 Today sits at a pivotal moment in its history. After breaking the 10,000-point barrier for the first time ever in early 2026 and recording an all-time closing high of 10,910.55 on February 27, 2026, the UK’s flagship blue-chip index has become one of the most closely watched benchmarks in global finance. For retail investors, institutional traders, and anyone seeking real-time intelligence on the London Stock Exchange, tracking FTSE 100 Today is no longer optional, it’s the foundation of a smarter UK investing strategy.

FintechZoom.Live delivers zero-delay price updates, curated analyst signals, and forward-looking data on every major index and stock that matters. This post breaks down where the FTSE 100 stands right now, what the 2026 forecast means for your portfolio, and which positions make the most sense based on the latest market data.

The FTSE 100 Today is trading in the range of 10,800 to 11,100, with April 2026 projections pointing toward an average level near 10,885 before a potential push toward 11,165 by month-end.

The London Stock Exchange opens at 08:00 GMT and closes at 16:30 GMT, Monday through Friday, excluding UK public holidays. Real-time pricing is available via FintechZoom.Live’s live widget, which pulls direct feeds from the LSE and updates tick-by-tick throughout the trading session.

Key intraday metrics to watch right now:

For the most precise FTSE 100 Today live price, use the interactive chart on FintechZoom.Live, which also overlays RSI, moving averages, and volume signals for active traders.

The FTSE 100, or “Footsie,” is the index of the 100 largest companies by free-float market capitalisation listed on the London Stock Exchange, and it represents approximately 80% of the total LSE market cap.

Launched on January 3, 1984, at a base level of 1,000 points, the Footsie has grown into the primary benchmark for UK blue-chip equities and one of the world’s most widely tracked indices. It is calculated in real time, weighted by free-float market cap, and rebalanced quarterly. When a company’s market cap grows enough, it enters the index; when it falls, it exits.

What makes tracking FTSE 100 Today particularly relevant in 2026 is its international character. As Morningstar chief European market strategist Michael Field has pointed out, as much as 80% of constituent revenue derives from overseas operations. This means the index is less a measure of the UK domestic economy and more a barometer of global corporate health, making it relevant far beyond London.

Current sector breakdown (as of January 1, 2026, per Siblis Research):

This sector composition explains why the index moves correlate so strongly with commodity prices, bank earnings cycles, and global pharmaceutical pipelines.

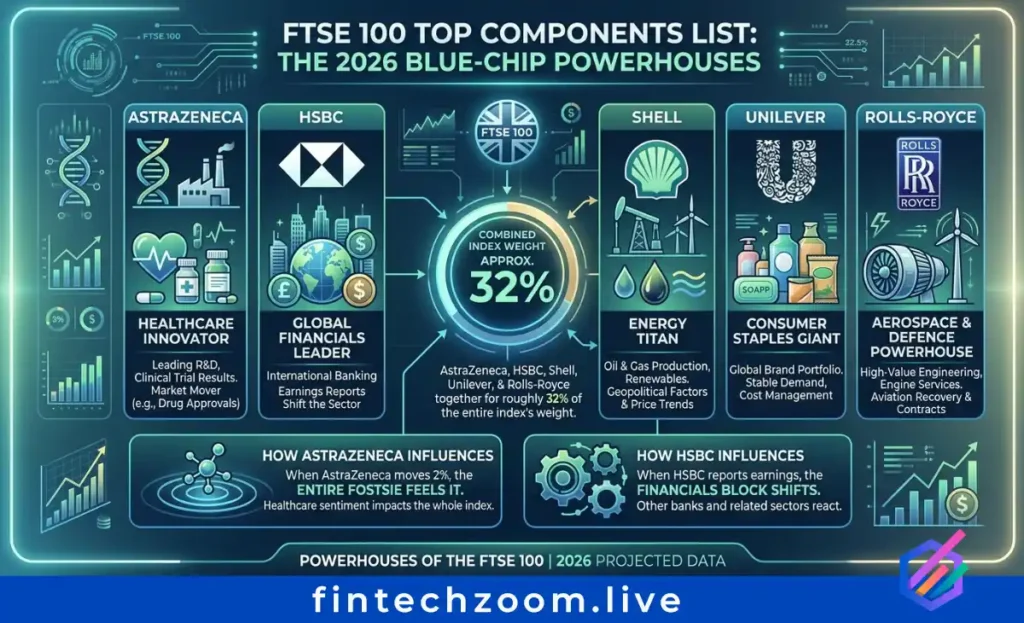

The five largest FTSE 100 constituents by market cap, AstraZeneca, HSBC, Shell, Unilever, and Rolls-Royce, together account for approximately 32% of the entire index’s weight.

Understanding the top holdings is the fastest way to understand where the index is headed on any given day. When AstraZeneca moves 2%, the entire Footsie feels it. When HSBC reports earnings, the Financials block shifts.

| Company | Ticker | Approx. Market Cap (2026) | Sector | 2026 Verdict |

|---|---|---|---|---|

| AstraZeneca | AZN | ~£210bn (~$284bn) | Healthcare | Hold/Buy – pipeline strength, oncology leads |

| HSBC Holdings | HSBA | ~$275bn | Financials | Buy – largest dividend payer (£10.7bn forecast) |

| Shell | SHEL | ~$212bn | Energy | Hold – £6.3bn dividend forecast; oil price sensitivity |

| Unilever | ULVR | Top 5 | Consumer Staples | Hold – stable income, slow price growth |

| Rolls-Royce | RR. | Top 5 | Industrials | Buy – up 1,040% in five years, earnings recovery phase |

| RELX | REL | Top 10 | Information Services | Buy – 12-month target ~44% above current price |

| British American Tobacco | BATS | Top 10 | Consumer Staples | Hold/Income – £5.3bn dividend forecast |

| Barclays | BARC | Top 10 | Financials | Buy – dividend upgrade of £800m expected in 2026 |

| Glencore | GLEN | Top 10 | Mining | Hold – largest dividend increase (£800m) alongside HSBC |

| GSK | GSK | Top 10 | Healthcare | Buy – analysts see significant upside from current valuation gap |

Data sources: CMC Markets (Jan 2026), AJ Bell Dividend Dashboard (Apr 2026), Motley Fool UK (Jan 2026).

HSBC is projected to deliver the single largest dividend payment within FTSE 100 Today at £10.7bn for 2026, followed by Shell at £6.3bn and British American Tobacco at £5.3bn.

The analyst consensus for FTSE 100 Today by end-2026 sits in the 11,000–12,700 range, with a bull-case scenario touching 13,000+ if corporate profit upgrades continue and UK rates fall faster than expected.

Several independent forecasting models converge on a year-end 2026 target between 11,165 and 12,767. AJ Bell investment director Russ Mould has highlighted that analysts have actually upgraded profit forecasts for 2026 and 2027 in the first three months of this year, a marked contrast to the pattern of recent years. Pre-tax income across the index is now expected to hit a record £264bn in 2026, followed by an even higher £288bn in 2027.

Dividend outlook:

Record aggregate FTSE 100 payouts of £88bn are forecast for 2026, up from £86bn estimated in December, according to the AJ Bell Dividend Dashboard (April 2026). This surpasses the previous all-time high of £85.2bn set in 2018. Adding £29.4bn in share buybacks already declared, the total cash return expected from FTSE 100 Today constituents is approximately £117.4bn, equivalent to 4.4% of the index’s total market cap.

Bull scenario (probability: moderate):

Bear scenario (probability: lower but real):

From a pure technical standpoint, FTSE 100 Today has confirmed a breakout above the 10,000-point psychological level, with the next meaningful resistance zone at 11,000, followed by the 12,000 region.

Key technical levels to track (April 2026):

The chart in 2026 shows a well-established uptrend from the 2022–2023 consolidation base. The February 2026 all-time high at 10,910.55 acts as the primary technical ceiling. A clean weekly close above 11,000 would open the path toward 11,700–12,000 by mid-year, aligning with multiple forecast model averages.

Traders using FintechZoom.Live’s real-time chart can layer Bollinger Bands and the MACD histogram alongside the intraday feed to identify momentum shifts as they happen.

Also Read This: 2026 health finance is booming as AI, GLP-1 drugs, and digital health drive a $429B market, while healthcare stocks rebound and HSAs hit new limits amid policy shake-ups.

Discover smart investment angles in mental health fintech, wearables, and ETFs like XLV before the next wave of outpatient and longevity plays hits.

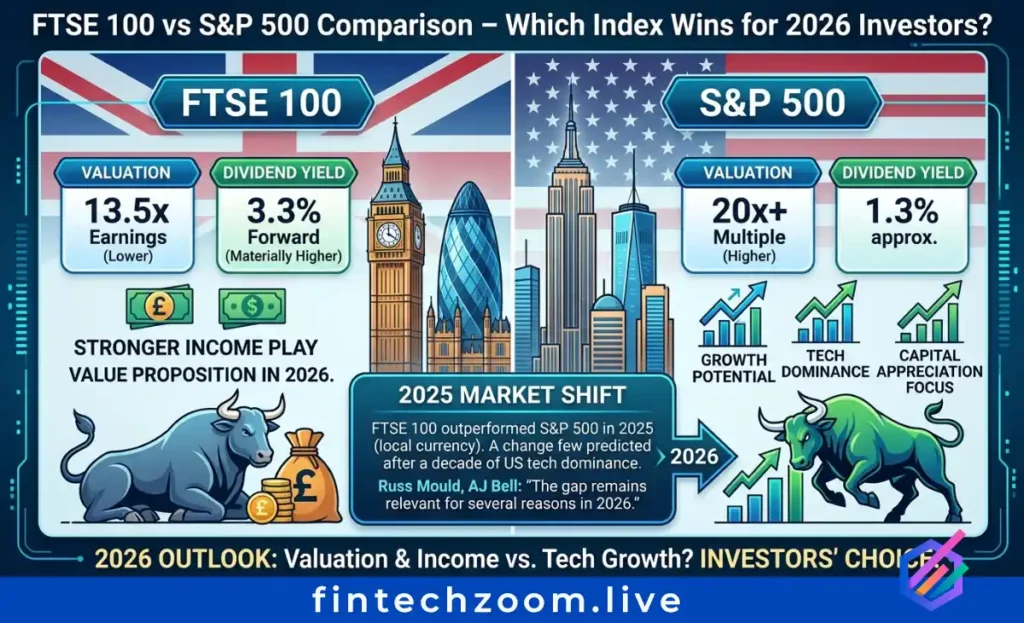

The FTSE 100 Today offers a materially higher dividend yield (3.3% forward) and lower valuation multiple (13.5x earnings) versus the S&P 500’s approximately 1.3% yield and 20x+ multiple, making it the stronger income play and value proposition in 2026.

The performance story has changed notably. As AJ Bell’s Russ Mould noted, the FTSE 100 outperformed the S&P 500 in 2025 in local currency terms, a result few predicted given the decade-long dominance of US tech stocks. In 2026, the gap remains relevant for several reasons:

UK blue-chip index advantages vs S&P 500:

S&P 500 advantages:

For income-focused investors and those seeking relative value in 2026, FTSE 100 Today represents a compelling alternative. For growth-oriented investors betting on AI-driven earnings expansion, the S&P 500 retains the structural edge. A blended approach tracking the Footsie through FintechZoom.Live while maintaining S&P 500 exposure delivers geographic and sector balance.

The most efficient way to gain exposure to FTSE 100 Today without stock-picking risk is through a low-cost index ETF, with the top options offering expense ratios as low as 0.07%.

Top FTSE 100 ETF options for 2026:

| ETF | Ticker | Expense Ratio | Dividend Treatment | Best For |

|---|---|---|---|---|

| iShares Core FTSE 100 ETF | ISF | 0.07% | Distributing | Core long-term hold |

| Vanguard FTSE 100 ETF | VUKE | 0.09% | Distributing | Income investors |

| HSBC FTSE 100 ETF | HUKX | 0.07% | Distributing | Cost-sensitive buyers |

| Invesco FTSE 100 ETF (Acc) | S100 | 0.09% | Accumulating | Growth compounding |

| Lyxor FTSE 100 ETF | L100 | 0.04% | Distributing | Lowest cost option |

All five provide near-identical exposure to the UK’s blue-chip benchmark, tracking the index with minimal tracking error. The main distinction is whether dividends are distributed (ideal for income investors drawing on yield) or accumulated (ideal for those reinvesting for growth). Given the forecast 3.3% forward yield, distributing ETFs are particularly attractive for 2026 income portfolios.

Tax-efficient wrappers such as the Stocks and Shares ISA allow UK investors to capture dividends and capital gains from FTSE 100 Today holdings free of UK tax, an advantage unique to the domestic market.

There are four primary routes to FTSE 100 Today exposure: direct shares, index ETFs, CFDs, and futures/options, each with a different risk, cost, and time horizon profile.

1. Direct share ownership Buy individual Footsie constituents through a share dealing account. Best for active stock-pickers targeting AstraZeneca, HSBC, or RELX specifically.

2. Index ETFs Low-cost, passive exposure to the index as a whole. Best for buy-and-hold investors with a 3–10 year horizon.

3. CFDs (Contracts for Difference) Used by active traders to go long or short on the Footsie with leverage. Higher risk; appropriate only for experienced traders with clear stop-loss discipline.

4. Futures and options Institutional and sophisticated retail traders use FTSE 100 futures and options for hedging or leveraged directional bets. Require margin accounts and active management.

2026 actionable framework:

The two macro variables driving FTSE 100 Today in April 2026 are the ongoing Middle East conflict’s effect on energy prices and the Bank of England’s rate-cutting timeline.

Recent conflict in the Middle East triggered a correction of more than 10% from the February high, but AJ Bell’s dividend dashboard confirms that profit forecasts are “not showing any sign of strain yet” as of early April 2026. Oil prices spiking above $100/barrel remain a risk, given their impact on consumer discretionary spending and industrial margin compression across FTSE 100 Today constituents.

UK-specific macro risks affecting the index right now:

FintechZoom.Live publishes breaking FTSE 100 Today news throughout the trading day, including earnings releases, macro data drops, and analyst rating changes the moment they hit the wire.

The FTSE 250 is the mid-cap companion to FTSE 100 Today, covering the next 250 largest LSE-listed companies, and it has a much higher sensitivity to the UK domestic economy.

While the Footsie earns 80% of its revenue internationally, the FTSE 250 skews heavily toward domestic UK businesses, retailers, housebuilders, regional banks, and leisure companies. This makes the FTSE 250 a better barometer of UK consumer confidence and domestic GDP growth, and a more volatile but potentially more rewarding play when UK economic conditions improve.

Smart investors track both indices on FintechZoom.Live simultaneously. FTSE 100 Today provides global, large-cap, dividend-rich stability. The FTSE 250 adds domestic beta, growth potential, and small/mid-cap alpha when the UK economic cycle turns. Many portfolio managers use the Footsie as a core holding and the FTSE 250 as a satellite position to balance yield and growth.

The data for 2026 builds a consistent picture. FTSE 100 Today sits at a historically attractive valuation relative to the S&P 500. Record dividends of £88bn are within reach. Profit forecasts have been upgraded, not cut. And the total cash yield of 4.4%, dividends plus buybacks, still outpaces UK inflation and the Bank of England base rate.

The risks are real: gilt yields near 5%, Middle East uncertainty, GBP fluctuations, and the absence of major technology exposure compared to US indices. But for income investors and value-oriented buyers, these are known, manageable risks, not structural flaws.

Your 2026 FTSE 100 Today action plan:

Bookmark FintechZoom.Live as your daily FTSE 100 Today dashboard.

1. What is the current FTSE 100 live price today? As of April 18, 2026, the index is trading approximately between 10,800 and 11,100. The all-time closing high was 10,910.55, reached on February 27, 2026. For the precise real-time level, FintechZoom.Live updates tick-by-tick during London trading hours (08:00–16:30 GMT).

2. What is the FTSE 100 forecast for 2026? Multiple analyst models project the index in the range of 11,000–12,700 by year-end 2026, with bullish scenarios pointing toward 13,000+. AJ Bell’s investment director Russ Mould has cited 14% analyst-consensus profit growth for 2026 as the primary support for continued upside.

3. Which are the best FTSE 100 dividend stocks for 2026? The highest total dividend payers in the index for 2026 are HSBC (£10.7bn forecast), Shell (£6.3bn), and British American Tobacco (£5.3bn). For yield percentage, Legal & General and Standard Life (Phoenix Group) offer the highest forward dividend yields, both in the 7–8% range.

4. How does the British Pound affect FTSE 100 Today? A weaker GBP is broadly positive for the Footsie because the index’s constituents earn approximately 80% of their revenues in foreign currencies. When the pound falls, those overseas earnings translate back into GBP at a higher value, boosting reported profits. Conversely, GBP strength, as seen in early 2026, acts as a “translational headwind” per Aviva Investors’ commentary cited by Morningstar.

5. Should I buy, sell, or hold FTSE 100 stocks right now? Based on current data, the consensus leans toward buy on dips / hold. At ~13.5x forward earnings and a 3.3% dividend yield, the index offers better value than the S&P 500. The Middle East conflict and gilt yield headwinds are the primary risks to watch. Active traders should treat any pullback toward 10,365–10,600 as a considered buying window. This is not personal financial advice.

6. What are the top FTSE 100 ETFs to buy in 2026? The strongest options for FTSE 100 Today exposure are iShares Core FTSE 100 ETF (ISF, 0.07% OCF), Vanguard FTSE 100 ETF (VUKE, 0.09% OCF), and Lyxor FTSE 100 ETF (L100, 0.04% OCF). Distributing variants suit income investors; accumulating variants suit growth-oriented portfolios.

7. How do gilt yields impact FTSE 100 performance? The 10-year UK gilt yield is currently near 5% — its highest level since 2008. Elevated gilt yields create two headwinds for the index: they raise the discount rate applied to future equity cash flows (reducing valuations), and they offer income investors a competitive risk-free alternative to FTSE 100 Today dividend stocks, potentially redirecting capital from equities to bonds.

8. FTSE 100 vs S&P 500 – which is better for 2026? For income investors, FTSE 100 Today wins clearly: 3.3% dividend yield vs ~1.3% for the S&P 500, and a materially cheaper valuation. For growth investors betting on AI and tech mega-cap earnings, the S&P 500 retains the edge. A blended portfolio tracking both indices offers the best of both worlds in 2026.

9. What time does the FTSE 100 open in London? The London Stock Exchange begins trading at 08:00 GMT and closes at 16:30 GMT, Monday to Friday, excluding UK public holidays. Pre-market auction runs from approximately 07:50 GMT. Real-time FTSE 100 Today pricing outside these hours reflects futures or after-market activity.

10. How is FTSE 100 different from the FTSE 250? FTSE 100 Today covers the 100 largest LSE companies, with ~80% of revenue earned internationally, making it a global blue-chip index rather than a UK-domestic one. The FTSE 250 covers the next 250 companies and has far higher domestic UK revenue exposure, making it more sensitive to UK consumer spending, GDP growth, and Bank of England policy. Together, the FTSE 100 Today and FTSE 250 form the FTSE 350, the broadest practical measure of the UK equity market.

Also Read This: Corporate finance in 2026 is firing on all cylinders: M&A volumes are up 40% YoY, private credit is eclipsing traditional bank lending in a $41T market, and the IPO window is selectively open for AI-powered profitable companies.

Agentic AI has moved into the CFO’s office, autonomously managing cash flow, fraud, and forecasts, while SMEs tap fintech platforms for instant working capital amid lingering tariff and macro risks.

Curated Editorial Insights Across FintechZoom’s Core Verticals: Thought-provoking analysis in Markets, Business Strategy, Crypto Innovation, Personal Finance, Economic Policy, and Lifestyle Wealth, designed to challenge conventional thinking, deepen financial literacy, and empower readers to make smarter, forward-looking decisions.

FintechZoom.Live is your real-time gateway to smarter investing, delivering instant stock market updates, expert analysis, and actionable insights on the stocks that matter most. From Magnificent 7 giants like NVIDIA, Microsoft, and Tesla to high-momentum meme stocks like GameStop and AMC, we cover the full spectrum of opportunities with zero-delay reporting. Our platform specializes in low-competition, high-value SEO content clusters, prioritizing “buy or sell” decision guides, price predictions, and forecast analysis for retail and institutional investors alike. Whether you’re tracking EV disruptors Lucid and Rivian, AI leaders Palantir and C3.ai, or legacy dividend plays like Ford and IBM, FintechZoom.Live provides semantic-rich, data-driven coverage optimized for search visibility and investor clarity. With 50+ stock clusters, 500+ semantic keywords, and real-time market intelligence, we empower you to make informed decisions before the market moves. Your edge starts here live.

Disclaimer

The information provided on FintechZoom.Live is for informational purposes only and should not be considered financial or investment advice. Investing in cryptocurrencies, digital assets, or any financial product involves significant risk, including the potential loss of your entire investment. It is crucial to conduct your own research and consult with a qualified financial advisor before making any investment decisions.

FintechZoom.Live does not endorse any specific investment or financial product. We are not responsible for any losses or damages incurred as a result of using the information on our website.

Please be aware that the regulatory landscape for cryptocurrencies and digital assets is complex and varies across jurisdictions. It is important to understand the applicable regulations in your location before investing.

For further information on U.S. regulations, you may refer to the following resources:

Securities and Exchange Commission (SEC): https://www.sec.gov/

Commodity Futures Trading Commission (CFTC): https://www.cftc.gov/

Financial Crimes Enforcement Network (FinCEN): https://www.fincen.gov/

By using FintechZoom.Live, you acknowledge and agree to this disclaimer.

Your trusted source for stocks, crypto, commodities, and fintech news. Track live prices, explore market trends, and make informed financial decisions with data that moves as fast as the markets.