Asian stock markets today are flashing a clear message: volatility is the price of opportunity. As of April 18, 2026, Asia-Pacific indices are navigating a complex intersection of geopolitical risk, AI-driven earnings momentum, and shifting central bank postures. The Nikkei 225 closed Friday at 58,886, down 1.06%, retreating after touching a near all-time high just 48 hours earlier. The Hang Seng Index settled at 26,126.86 (down 1%), while the Shanghai Composite edged to 4,051.45. These moves are not noise. They are signals. And reading them correctly, before the next session opens, is exactly what separates informed investors from reactive ones.

International investing involves currency risk, political risk, and differences in accounting standards. Speak with an adviser before making international equity investments.

International investing involves currency risk, political risk, and differences in accounting standards. Speak with an adviser before making international equity investments.

FintechZoom.Live delivers zero-delay data, expert forecasts, and buy-or-sell decision frameworks on every index that matters, from the Nifty 50’s domestic growth story to Taiwan’s semiconductor supercycle.

The short answer: Asian indices closed the week on a cautious note, with broad-based declines driven by profit-taking and Iran ceasefire uncertainty, not deteriorating earnings.

Investors tracking asian stock markets today live will find the following benchmark levels heading into the weekend session:

| Index | Last Close | Change | Key Driver |

|---|---|---|---|

| Nikkei 225 (Japan) | 58,886 | -1.06% | Tech/AI profit-taking |

| Hang Seng (Hong Kong) | 26,126.86 | -1.00% | Ceasefire uncertainty |

| Shanghai Composite | 4,051.45 | -0.10% | Modest consolidation |

| KOSPI (South Korea) | 6,191.19 | -0.60% | Energy import costs |

| ASX 200 (Australia) | ~9,150 | -0.53% | Risk-off sentiment |

| Nifty 50 (India) | ~23,200 | -1.90% | Worst weekly performer |

Pre-market gaps and volume signals point to a cautious open across Asia-Pacific markets today live on Monday, pending weekend developments in US-Iran negotiations. Oil prices remain elevated: West Texas Intermediate briefly spiked to $104.82 following weekend reports that ceasefire talks stalled, putting disproportionate pressure on Japan, South Korea, and India as net energy importers.

Biggest movers this week: Technology and AI-adjacent names led losses. Kioxia Holdings fell 9.6%, Sumco dropped 9.56%, and SK Hynix slid 3.46%. On the upside, Chinese EV names caught a bid. Contemporary Amperex (CATL) gained 5.5% and BYD added 2.4%.

Real-time technical signals show the Nikkei 225 testing support at the 58,500 level. RSI readings across major Asian indices are cooling from overbought territory (above 70) back toward the 55-60 range, a healthy reset rather than a trend reversal. The 50-day moving average continues to slope higher on both the Nikkei and KOSPI, confirming the medium-term uptrend structure remains intact.

The short answer: Each major Asian market is driven by distinct macro catalysts, and understanding those distinctions is the difference between smart allocation and guesswork.

The Nikkei 225 hit a record high in mid-April 2026 before Friday’s pullback to 58,886. The index is up dramatically from its 2024 base, driven by three structural forces: yen weakness boosting export earnings, Bank of Japan (BOJ) normalization that is still gradual enough to remain equity-friendly, and corporate governance reforms compelling Japanese firms to prioritize return on equity over asset hoarding. UBS Securities Japan’s year-end 2026 target of 54,000 implies modest upside from current levels, though analysts note that AI-infrastructure spending by Japanese tech suppliers could lift that ceiling if semiconductor demand accelerates beyond consensus estimates.

China’s Shanghai Composite Index is up 23.63% year-over-year as of April 16, 2026, a figure that would have seemed implausible eighteen months ago. Beijing’s multi-pronged stimulus campaign, spanning property market support, consumer subsidies, and tech sector rehabilitation, has fundamentally changed the investment calculus. The Hang Seng, at 26,126.86, reflects a market still pricing in geopolitical risk premium, but the direction of travel is constructive. PineBridge Investments notes that both indexes had risen around 15% and 30%, respectively, year-to-date through late 2025, and that investor confidence in China has structurally improved heading into 2026.

India is the growth engine of Asia, full stop. The IMF projects Indian GDP growth at 6.5%+ for 2026, and the Nifty 50 and Sensex reflect a domestic economy firing on multiple cylinders: consumer spending, digital infrastructure build-out, and financial sector deepening. Friday’s 1.9% decline in the Nifty 50 was the worst single-day performance among major Asian benchmarks, but this is largely attributed to energy-cost sensitivity given India’s oil import dependency, not a structural deterioration. The Sensex and Nifty 50 remain in long-term uptrends, with IT services, private banking, and infrastructure sectors providing the most durable earnings growth.

Australia’s ASX 200 (~9,150) reflects a resource-heavy economy benefiting from Chinese demand recovery and steady domestic employment. South Korea’s KOSPI at 6,191.19, after surging 71.2% in 2025, is consolidating. Its near-term trajectory depends heavily on Samsung Electronics and SK Hynix, both exposed to Nvidia’s AI chip demand cycle. Taiwan’s TAIEX, home to TSMC, remains one of the highest-conviction structural plays in global markets. Analysts hold a 12-month median price target on TSMC representing a 24.18% premium to April 2026 opening levels.

Side-by-side YTD performance snapshot (as of April 18, 2026):

| Index | YTD 2026 | 2025 Full Year |

|---|---|---|

| KOSPI | +8.2% | +71.2% |

| Hang Seng | +6.4% | +28.7% |

| Nikkei 225 | +14.5% | +61.9% |

| Shanghai Composite | +23.6% YoY | ~+15% |

| ASX 200 | +3.1% | +11.2% |

| Nifty 50 | -1.8% | +9.4% |

The short answer: Six structural forces are reshaping the risk-reward calculus across Asia-Pacific, and ignoring any one of them creates blind spots that cost returns.

Across asian stock markets today, six macro and sector catalysts are simultaneously at work, each pulling capital flows in a distinct direction.

China’s stimulus and tech self-sufficiency push is the most underappreciated driver in global markets right now. Beijing has moved decisively to rehabilitate its technology sector, provide consumer fiscal support, and stabilize property markets. The result is a sentiment shift among institutional allocators who had been systematically underweight China through 2023 and 2024.

India’s 6.5%+ GDP growth engine places it in a category of its own among major economies. The digital economy, spanning payments, e-commerce, financial inclusion platforms, and IT exports, is creating a compounding earnings base for Indian equities that structural investors are increasingly pricing as a 10-year secular opportunity.

The Bank of Japan’s normalization trajectory remains one of the most consequential monetary policy stories globally. The BOJ is moving away from decades of ultra-loose policy, but the pace is measured. Every 25-basis-point rate hike strengthens the yen, compresses export earnings, and tests equity valuations. The market is currently pricing in two more hikes through 2026. A faster pace would pressure the Nikkei 225 meaningfully below current levels.

The global AI and semiconductor supercycle is the single largest sector tailwind across Asia. Demand from the Magnificent 7, particularly Meta, Microsoft, and Alphabet, for high-bandwidth memory, advanced logic chips, and AI infrastructure is flowing directly into SK Hynix, TSMC, Samsung, Advantest, and SoftBank Group. The IMF explicitly cites AI-driven investment as offsetting the drag from US tariff uncertainty on Asian economies in 2026.

EV and green energy transition is a multi-year structural sector theme with China at the center. CATL’s 5.5% gain this week reflects accelerating EV penetration in both domestic and export markets. BYD’s order book remains robust. The EV supply chain, spanning battery chemistry, rare earth processing, and power electronics, is predominantly concentrated in Asia, creating structural earnings visibility.

Currency dynamics and US Fed policy ripple effects cannot be overstated. The IMF’s expectation of continued US dollar depreciation in 2026 is historically positive for Asia equities. Invesco’s 2026 Asia outlook explicitly states that a weakening dollar trajectory has historically benefited the region. Combined with the global rate-cut cycle, this creates a liquidity tailwind that institutional investors are actively positioning for.

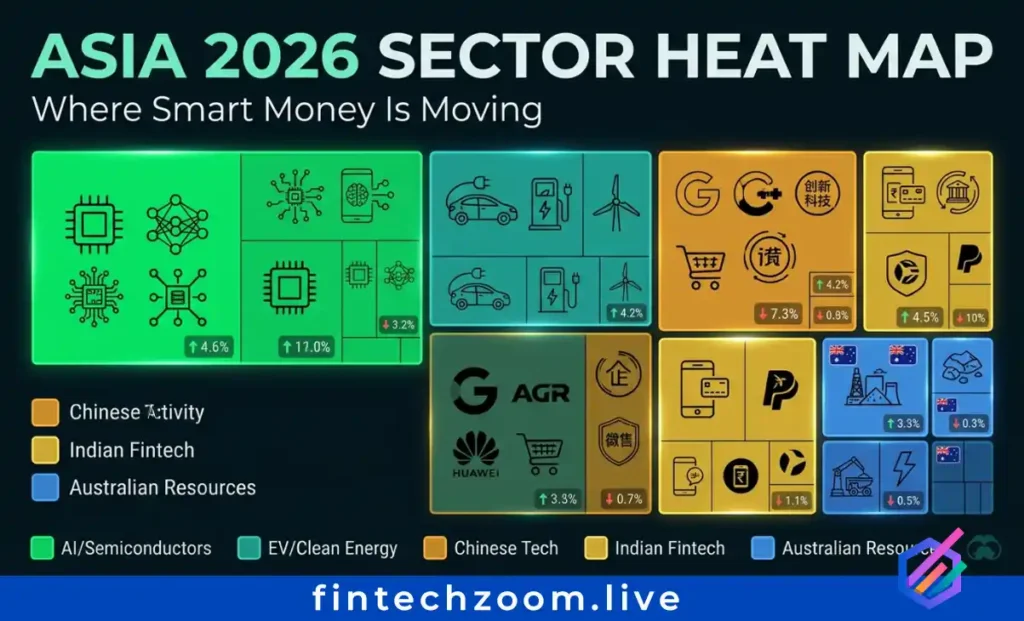

The short answer: Five high-conviction positions stand out across AI/semiconductors, Chinese tech recovery, Indian financial services, and Australian resources.

1. TSMC (Taiwan Semiconductor Manufacturing)

2. Tencent Holdings (Hong Kong/ADR)

3. SK Hynix (South Korea)

4. HDFC Bank or SBI (India)

5. BHP Group (ASX 200, Australia)

ETF Watchlist for Broad Asia Exposure:

The short answer: Bull cases are intact for Nikkei and KOSPI; China recovery plays remain the highest-risk, highest-reward setup; India needs oil stabilization.

Nikkei 225 Forecast 2026: The rounding bottom pattern that formed on the 4-hour chart through late February 2026 played out as the index surged to near-record highs before Friday’s pullback. Key resistance sits at 59,518 (recent high) and 60,000 (psychological ceiling). Support zones are at 58,500 and 56,500. UBS targets 54,000 as a year-end base case. A break above 60,000, requiring sustained AI earnings beats and a stable yen, would open a path toward 65,000 in a bull scenario.

Hang Seng 2026 Target: The Hang Seng’s recovery from its 2024 multi-year lows has been dramatic. Technical support holds at 25,500. Bull case: 30,000 if China’s domestic demand recovery accelerates. Bear case: 22,000 if US-China technology restrictions escalate.

Nifty 50 Outlook 2026: India’s medium-term technical structure remains positive, but the index is highly sensitive to global oil prices given India’s import dependence. Support at 22,500. Base case year-end target: 26,500-28,000, contingent on oil stabilization below $90 per barrel.

KOSPI: The 6,000 level is now critical support after the index’s extraordinary 2025 run. A confirmed hold above 6,000 keeps the medium-term uptrend intact. The governance reform catalyst from Korea’s amended Commercial Code, expanding fiduciary duties and improving board independence, is a structural positive still being priced by institutional investors.

Weekly and Monthly Outlook: The dominant theme for the week of April 21 is Iran ceasefire progress. A confirmed deal extension would immediately lift all Asian indices, with energy-sensitive markets (Japan, Korea, India) seeing the sharpest snap-back. A breakdown in talks would push oil back toward $110 and test Asian support levels.

The short answer: Market timing, currency hedging, and platform selection are the three variables that determine whether a retail investor captures Asia’s structural returns or gets ground down by volatility.

Asian Markets Open and Close Time Cheat Sheet (UTC):

| Market | Open (UTC) | Close (UTC) |

|---|---|---|

| Tokyo (Nikkei 225) | 00:00 | 06:00 |

| Shanghai/Shenzhen | 01:30 | 07:00 |

| Hong Kong (HSI) | 01:30 | 08:00 |

| Mumbai (NSE/BSE) | 03:45 | 10:00 |

| Sydney (ASX 200) | 23:00 | 05:00 |

| Seoul (KOSPI) | 00:00 | 06:30 |

Currency hedging: Investors outside Asia face meaningful FX drag. A strengthening yen or rupee relative to the USD can amplify or erode returns independently of equity performance. Hedged ETF share classes (e.g., USD-hedged Nikkei ETFs) reduce this variable for US-based investors. However, with the USD expected to weaken in 2026, unhedged positions may actually benefit from currency tailwinds in markets like India and South Korea.

Portfolio allocation tips for 2026: Invesco’s institutional outlook recommends a constructive overweight on Asia ex-Japan equities, citing improving earnings prospects, supportive liquidity, and structural reform momentum. A rule-of-thumb allocation for retail investors: 8-12% of total equity exposure to Asia, split roughly 40% to India/Southeast Asia, 30% to China/HK recovery plays, and 30% to semiconductor/AI-led markets (Korea, Taiwan, Japan).

Risk management playbook: Geopolitical events, specifically the Iran-US war and associated oil supply disruptions, are the primary tail risk for Asian markets in 2026. Position sizing below 5% per individual stock, stop-losses 10-12% below entry for volatile names like semiconductor stocks, and diversification across at least three sub-regions within Asia are the minimum risk controls for retail participants.

The short answer: Speed and depth are not mutually exclusive, and in fast-moving Asian markets, you need both simultaneously.

FintechZoom.Live tracks asian stock markets today with zero-latency data feeds across 12 major Asia-Pacific indices. The platform delivers intraday technical signals, institutional sentiment data, earnings calendars calibrated to Asian time zones, and buy/sell/hold ratings updated as market conditions shift, not once a day after close. For investors who need to act on China stimulus announcements at 2 AM UTC or BOJ rate decisions at 3 AM UTC, delayed platforms are not a real option.

The semantic-rich analysis on FintechZoom.Live is also built for AI answer engines and featured snippet visibility, which means the information you need to make decisions reaches you faster, through more search surfaces, with more contextual depth than legacy financial news platforms provide.

Asian stock markets today present a rare convergence: short-term volatility created by Iran conflict uncertainty sitting on top of one of the most structurally compelling equity investment backdrops in decades. The IMF projects the Asia-Pacific region to contribute the largest share of global GDP growth in 2026 at 4.1%. China’s recovery is real and quantifiable, with Shanghai up 23.63% year-over-year. India’s earnings growth runway is a multi-year story that patient capital is quietly accumulating. And the semiconductor/AI supercycle connecting Nvidia’s demand to SK Hynix’s and TSMC’s supply is not a 2026 story; it is a 2026-2030 structural shift.

The three strongest opportunities heading into Q3 2026 are: TSMC as the AI infrastructure backbone, Tencent as the China tech recovery proxy with the highest analyst upside target (+42%), and India’s private banking sector as the digital economy compounder. Bookmark FintechZoom.Live for daily pre-market analysis, subscribe for real-time buy/sell alerts, and position before the next macro catalyst moves the market, not after.

Asian sessions span UTC midnight to mid-morning. Tokyo opens at 00:00 UTC and closes at 06:00 UTC. Shanghai and Hong Kong open at 01:30 UTC. Mumbai opens at 03:45 UTC. Sydney opens Sunday evening at 23:00 UTC. Seoul mirrors Tokyo, opening at midnight UTC.

The Shanghai Composite held up best on a relative basis, declining only 0.1% on Friday versus India’s Nifty 50 dropping 1.9%. China’s limited exposure to oil import costs and its ongoing domestic stimulus program provided relative insulation from the Iran conflict-driven risk-off move.

Yes, with calibrated position sizing. UBS Securities Japan targets 54,000 for year-end 2026, implying roughly 8% upside from current levels in the base case. Semiconductor sector strength and corporate governance reform are structural positives. The primary risk is a faster-than-expected BOJ rate hike cycle strengthening the yen and pressuring exporters.

China’s policy stimulus has already driven the Shanghai Composite up 23.63% year-over-year as of April 2026. Continued consumer spending support, tech sector rehabilitation, and infrastructure spending provide the base for additional upside. PineBridge Investments holds a constructive view on both indexes through 2026, with a bull case Hang Seng target of 30,000 if domestic demand recovery accelerates.

TSMC (+24% median analyst target), Tencent (+42% median analyst target), SK Hynix (AI memory demand), HDFC Bank (India’s digital finance runway), and CATL (EV battery dominance) represent the highest-conviction opportunities across the region, based on current analyst consensus data.

Fed rate policy affects asian stock markets today through two channels: dollar direction and global liquidity. A rate-cutting Fed weakens the USD, which historically benefits Asia equities by improving dollar-denominated returns for US investors and reducing pressure on Asian currency debt. The IMF explicitly references globally accommodative financial conditions as a tailwind for Asia equities in 2026.

Both track India’s market closely: the Nifty 50 is the broader institutional benchmark (50 stocks), while the Sensex tracks 30 blue-chips. For pure India exposure, the Nifty 50 offers greater sector diversification. IT services, private banking, infrastructure, and consumer discretionary are the highest-conviction sectors within both indices for 2026.

The IMF projects emerging Asia to grow faster than the global average, with India leading at 6.5%+ and China at 4.4%. Korea’s governance reform momentum and improving shareholder returns are attracting global institutional capital. The primary risk for emerging markets Asia is US tariff escalation and energy price spikes from Middle East conflict.

The most accessible routes are US-listed ETFs (AAXJ, EWT, EPI), ADRs for major names like Tencent, Samsung, and TSMC, and global broker platforms with direct Asian market access. Currency-hedged share classes are available on most major Asian equity ETFs for investors concerned about FX drag.

AI semiconductors hold the highest near-term earnings momentum. Demand from US hyperscalers is not discretionary. EVs and battery supply chain names offer the strongest 3-5 year structural growth case, with China’s CATL and BYD dominating global supply. Indian fintech provides the most differentiated growth profile given the sub-penetration of financial services in a 1.4-billion-person economy.

Curated Editorial Insights Across FintechZoom’s Core Verticals: Thought-provoking analysis in Markets, Business Strategy, Crypto Innovation, Personal Finance, Economic Policy, and Lifestyle Wealth, designed to challenge conventional thinking, deepen financial literacy, and empower readers to make smarter, forward-looking decisions.

FintechZoom.Live is your real-time gateway to smarter investing, delivering instant stock market updates, expert analysis, and actionable insights on the stocks that matter most. From Magnificent 7 giants like NVIDIA, Microsoft, and Tesla to high-momentum meme stocks like GameStop and AMC, we cover the full spectrum of opportunities with zero-delay reporting. Our platform specializes in low-competition, high-value SEO content clusters, prioritizing “buy or sell” decision guides, price predictions, and forecast analysis for retail and institutional investors alike. Whether you’re tracking EV disruptors Lucid and Rivian, AI leaders Palantir and C3.ai, or legacy dividend plays like Ford and IBM, FintechZoom.Live provides semantic-rich, data-driven coverage optimized for search visibility and investor clarity. With 50+ stock clusters, 500+ semantic keywords, and real-time market intelligence, we empower you to make informed decisions before the market moves. Your edge starts here live.

Disclaimer

The information provided on FintechZoom.Live is for informational purposes only and should not be considered financial or investment advice. Investing in cryptocurrencies, digital assets, or any financial product involves significant risk, including the potential loss of your entire investment. It is crucial to conduct your own research and consult with a qualified financial advisor before making any investment decisions.

FintechZoom.Live does not endorse any specific investment or financial product. We are not responsible for any losses or damages incurred as a result of using the information on our website.

Please be aware that the regulatory landscape for cryptocurrencies and digital assets is complex and varies across jurisdictions. It is important to understand the applicable regulations in your location before investing.

For further information on U.S. regulations, you may refer to the following resources:

Securities and Exchange Commission (SEC): https://www.sec.gov/

Commodity Futures Trading Commission (CFTC): https://www.cftc.gov/

Financial Crimes Enforcement Network (FinCEN): https://www.fincen.gov/

By using FintechZoom.Live, you acknowledge and agree to this disclaimer.

Your trusted source for stocks, crypto, commodities, and fintech news. Track live prices, explore market trends, and make informed financial decisions with data that moves as fast as the markets.