Are you wondering where Disney stock is headed this year? With a brand new CEO at the helm and streaming finally turning a profit. DIS stock is one of the most talked about entertainment plays on Wall Street right now. If you have been searching for a reliable fintechzoom dis stock prediction. you are in the right place.

Disney stock (NYSE: DIS) is trading around $98 as of late March 2026. That is a steep drop from its all time high near $201 back in 2021. Yet 15 Wall Street analysts still rate it a “Strong Buy” with an average price target near $135. So what is going on? And more importantly. should you buy. hold. or sell?

In this post. we break down the fintechzoom dis stock prediction for 2026 using real data. recent earnings reports. analyst ratings. and our own analysis. Whether you are a beginner or a seasoned investor. this post will give you the clarity you need.

Why Fintechzoom DIS Stock Prediction Has Investors Divided Right Now

Disney is at a crossroads. The stock has dropped about 20% from its 52 week high of $124.69. and the broader market sell off has not helped. But the problems go deeper than macro pressure.

Here is what is weighing on the stock:

Streaming costs are still high. Disney+ and Hulu brought in $5.35 billion in Q1 fiscal 2026 revenue. up 11% year over year. Streaming operating income hit $450 million. That sounds great. but entertainment segment operating income still fell 35% overall because of rising content and marketing costs.

Ad revenue dropped 6%. The loss of Star India revenue from the prior year and a YouTube TV carriage dispute that cost Disney roughly $110 million in operating income both hit the bottom line.

Leadership change adds uncertainty. Bob Iger handed the CEO title to Josh D’Amaro on March 18. 2026. While D’Amaro is a 28 year Disney veteran who built the parks division into a profit engine. markets hate uncertainty. And a CEO change always creates it.

Have you considered how much of the current stock price already reflects these problems?

How FintechZoom Analyzes DIS Stock: Our Approach

When building a fintechzoom dis stock prediction. we look at three pillars: fundamentals. technicals. and sentiment. This is not guesswork. It is a structured process that combines real numbers with market psychology.

Fundamental Analysis

We study quarterly earnings. revenue growth by segment. profit margins. and cash flow. Disney reported $26 billion in Q1 fiscal 2026 revenue. a 5% increase. The experiences segment hit a record $10 billion in quarterly revenue for the first time ever. Domestic parks brought in $6.91 billion while international parks added $1.75 billion. Both grew 7% year over year.

Technical Analysis

Fintechzoom DIS stock prediction shares remain in a downtrend. The $102 to $108 zone acts as key resistance. If the price breaks below the $90 to $95 support range. it could slide toward $70 to $60. Moving averages also paint a cautious picture right now.

Sentiment Analysis

Wall Street is still bullish. 53% of analysts recommend a Strong Buy and 40% recommend a Buy. Only 7% suggest holding. Nobody is saying sell. The average price target of $134.73 implies roughly 35% upside from current levels.

Pro Tip: Always weigh analyst sentiment against the price chart. When analysts are bullish but the chart is bearish. the stock often needs more time to find a bottom before rallying. 🎯

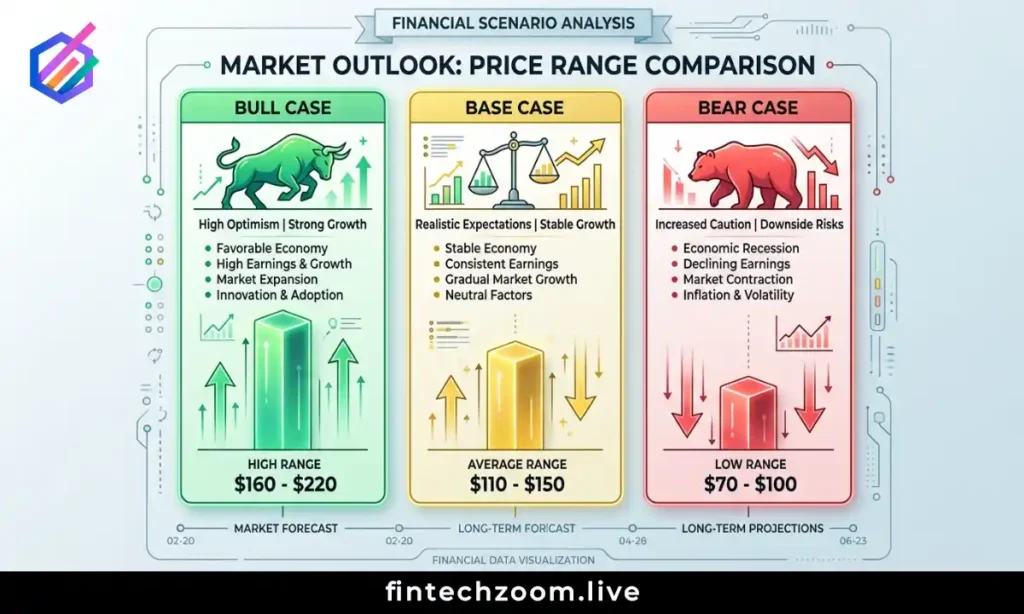

FintechZoom DIS Stock Prediction: Three Scenarios for 2026

Here is our detailed fintechzoom dis prediction broken into three possible outcomes. Each scenario is based on specific assumptions about streaming. parks. and the broader economy.

Bull Case: $130 to $150

In this scenario. Disney+ streaming margins reach the company’s 10% operating margin target for fiscal 2026. The new CEO D’Amaro successfully merges Disney+ and Hulu into a unified experience (planned for later this year). Theme parks continue setting revenue records. and the $60 billion global parks expansion plan starts generating visible returns. Box office hits from franchises keep the content pipeline strong.

If all of this plays out. the stock could reach or exceed the average analyst price target of $135.

Base Case: $100 to $125

This is the most likely path. Disney meets most of its guidance. streaming margins improve but stay slightly below 10%. and parks growth slows to mid single digits. The CEO transition goes smoothly without major strategic shifts. The stock trades sideways for several months before gradually recovering toward the end of the year.

Bear Case: $75 to $95

If the economy tips into recession. consumers cut back on discretionary spending. That hits both parks attendance and streaming subscriptions. Content costs balloon due to competition with Netflix. Amazon. and other platforms. The CEO transition leads to strategic confusion or delays. In this scenario. DIS could test its 52 week low of $80.10 or even break below it.

| Scenario | Price Range | Key Assumption | Probability |

| Bull Case | $130 to $150 | Streaming hits 10% margin. parks boom | 25% |

| Base Case | $100 to $125 | Steady growth. smooth CEO transition | 50% |

| Bear Case | $75 to $95 | Recession. rising costs. execution issues | 25% |

What scenario do you think is most likely based on current economic conditions?

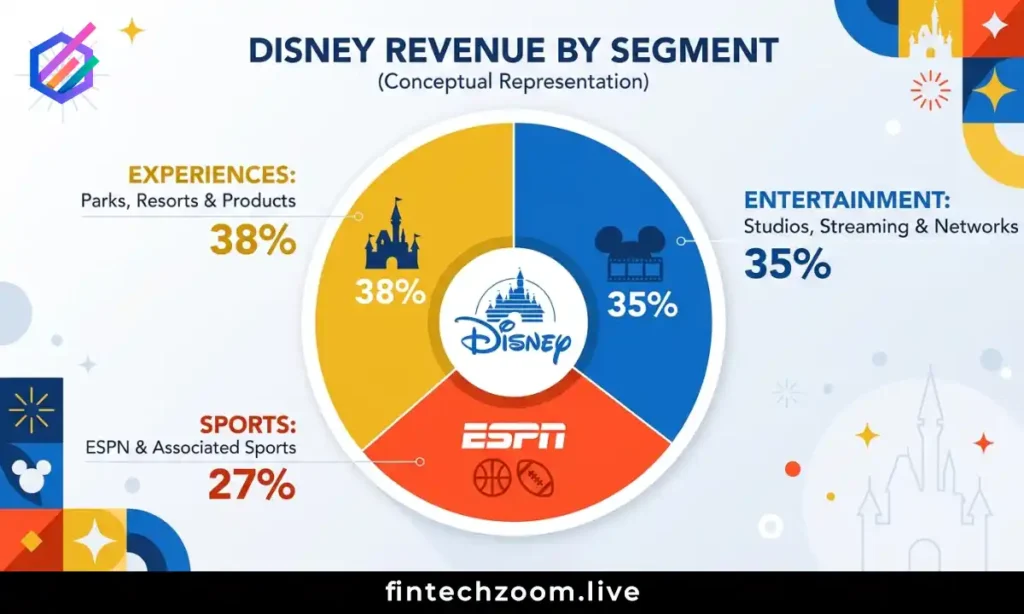

Disney’s Revenue Breakdown: Where the Money Comes From

To form an accurate fintechzoom dis analysis prediction. you have to understand how Disney actually makes money. The company operates in three segments.

Experiences (Theme Parks. Cruises. Consumer Products)

This is now Disney’s biggest profit engine. In Q1 fiscal 2026. the experiences division posted record revenue of $10 billion. Domestic parks generated $6.91 billion and international parks added $1.75 billion. Consumer products contributed $1.3 billion. Operating income for the segment was $3.3 billion.

Josh D’Amaro built this division from the ground up. His promotion to CEO signals that Disney sees parks and experiences as the future growth driver. The company has committed $60 billion to global park expansions over the coming years.

Entertainment (Streaming. Studios. Linear TV)

Revenue grew 7% to $11.6 billion in Q1 fiscal 2026. Streaming is finally profitable. Disney+ and Hulu generated $450 million in operating income. up 72% from the prior year. However. overall entertainment segment operating income fell 35% to $1.1 billion due to higher content costs and the FuboTV acquisition.

Disney no longer reports subscriber numbers for Disney+ or Hulu. following Netflix’s lead. The company now focuses on revenue per user and operating margins instead.

Sports (ESPN)

ESPN posted $191 million in operating income for the quarter. down $56 million from last year. Ad revenue grew 10% but was offset by higher programming costs. The YouTube TV carriage dispute was a painful short term hit.

Pro Tip: The experiences segment now drives more profit than entertainment. Watch parks revenue closely because it tells you more about Disney’s near term health than streaming subscriber headlines. 🏰

What Analysts Are Saying About DIS Price Targets

When you look at the fintechzoom dis price target landscape. the consensus is clear. Most of Wall Street believes DIS is undervalued.

Here is a breakdown of recent analyst ratings:

| Firm | Rating | Price Target | Date |

| Guggenheim | Buy | $140 | Feb 3. 2026 |

| Wells Fargo | Buy | $150 | Feb 3. 2026 |

| TD Cowen | Buy | $123 | Feb 3. 2026 |

| Goldman Sachs | Buy | $151 | Recent |

| JP Morgan | Buy | $160 | Recent |

The average target across 15 analysts is $134.73. The lowest target is $112 and the highest is $160 from JP Morgan. That highest target implies over 60% upside from current prices.

Morningstar assigns a fair value of $132 to DIS and notes that no competitor can match the depth of Disney’s character library and franchises. They also point out that the streaming business is no longer a drag on profitability.

Do you find it interesting that every single analyst covering DIS rates it either Buy or Hold? Not a single Sell rating exists right now.

Disney vs Netflix: Which Entertainment Stock Wins?

A proper fintechzoom dis forecast insights analysis would be incomplete without comparing DIS to its biggest streaming rival.

| Metric | Disney (DIS) | Netflix (NFLX) |

| Stock Price (Mar 2026) | ~$98 | ~$950+ |

| Market Cap | ~$174B | ~$400B+ |

| P/E Ratio | ~15x | ~35x+ |

| Streaming Profitable? | Yes (8.4% margin) | Yes (higher margin) |

| Theme Parks Revenue | $10B per quarter | N/A |

| Dividend Yield | 1.3% | 0% |

| Content Library | Marvel. Star Wars. Pixar. ESPN | Original content focus |

Disney trades at a significant discount to Netflix on a P/E basis. That reflects the market’s concerns about Disney’s transformation. But it also creates opportunity. Disney owns something Netflix cannot replicate: theme parks. cruises. and decades of beloved intellectual property that drives merchandise. licensing. and live experiences.

Netflix is a pure play streaming company. Disney is a diversified entertainment empire. If you believe the parks and experiences growth story. DIS offers a better risk reward profile at current prices.

Pro Tip: Do not compare these stocks on streaming alone. Disney’s real edge is the flywheel between content. parks. merchandise. and streaming. That ecosystem is very hard for any competitor to copy. 🔄

The New CEO Factor: Josh D’Amaro’s Impact on DIS Stock

The fintechzoom dis trends conversation is incomplete without discussing the leadership change. Josh D’Amaro officially became Disney’s CEO on March 18. 2026. replacing Bob Iger.

Here is what has been revealed about his vision so far:

He wants Disney+ to become a digital hub. At his first shareholder meeting. D’Amaro said Disney+ will evolve beyond streaming to become a portal connecting stories. games. films. and experiences. He also confirmed plans to merge Disney+ and Hulu into a single unified app later this year.

Parks are his specialty. As head of the experiences division. D’Amaro led Disney’s theme parks to record revenue. He oversaw $36 billion in annual segment revenue and 185.000 employees worldwide. He is the architect of the largest global expansion in Disney Experiences history.

He is focused on connection. His stated goal is to deliver a more connected and personalized experience to consumers wherever they are. This suggests a strategy that ties streaming subscribers more closely to parks. merchandise. and live events.

Will D’Amaro’s parks first mentality give the stock the boost it needs?

Key Risks That Could Derail the Forecast

Every honest fintechzoom dis prediction market assessment must address the downside risks. Here are the biggest threats to watch.

Recession risk. Theme parks and streaming are both discretionary spending categories. If the economy weakens. consumers cut entertainment budgets first. Disney’s domestic parks saw attendance rise in Q1. but international visitation was softer. That softness could spread.

Streaming competition. Netflix. Amazon Prime Video. Max. and Apple TV+ are all fighting for the same viewers. Content costs keep rising. and Disney has to spend big just to keep its library competitive. The company reduced its FY26 revenue estimate from $101.9 billion to $100.8 billion partly because of a slim film release schedule.

Fox integration risks. Disney’s acquisition of Fox assets continues to present challenges. Analysts have flagged concerns about whether expected synergies will materialize on time.

Linear TV decline. Traditional cable and broadcast are shrinking fast. While streaming growth offsets some of this loss. the high margins Disney enjoyed from cable are gone forever.

Tariffs and global trade tensions. International parks in Shanghai. Paris. and Hong Kong face geopolitical risks that could affect attendance and revenue.

Frequently Asked Questions

Is Disney stock a good buy for beginners in 2026?

Disney can be a solid choice for beginner investors because the brand is easy to understand and the business is diversified. However. beginners should be aware that the stock is in a downtrend and may take time to recover. Start with a small position and add over time rather than going all in at once.

What is a realistic fintechzoom dis stock prediction for end of year 2026?

Based on analyst consensus and our own analysis. a realistic range is $100 to $135 by December 2026. The base case puts the stock around $110 to $120 assuming steady execution under the new CEO and continued streaming profitability.

Does Disney pay a dividend in 2026?

Yes. Disney currently pays a dividend with a yield of about 1.3%. The company restored its dividend after suspending it during the pandemic. While the yield is modest. it signals confidence in cash flow generation.

Should I sell DIS stock at current prices?

That depends on your timeline. If you are a long term investor (3 to 5 years). the current price near $98 is well below the $132 fair value that Morningstar assigns and well below the $135 analyst consensus target. Short term traders may want to wait for a clearer trend reversal before adding to positions.

What moves Disney stock price the most?

Earnings reports have the biggest impact. followed by streaming profitability updates. parks attendance data. and box office performance. CEO announcements and strategic shifts also move the stock. as we saw when D’Amaro’s appointment was announced.

Where DIS Stock Goes From Here

The full fintechzoom dis stock prediction together.

Disney is trading at a discount to both its historical valuation and Wall Street consensus targets. The P/E ratio of about 15x is well below the S&P 500 average and below Disney’s own five year average. The company expects double digit growth in adjusted earnings per share for fiscal 2026 and plans to repurchase $7 billion in stock.

The new CEO brings operational discipline and a parks first strategy that could re energize investor confidence. Streaming is now profitable. and the planned Disney+ and Hulu merger could improve user experience and reduce churn.

At the same time. risks are real. The economy is uncertain. streaming competition is fierce. and the leadership transition needs time to prove itself.

Our take: DIS stock looks like a strong long term buy at current prices for investors who can hold for 2 to 3 years. The risk reward ratio is favorable when you compare the current price near $98 to the analyst consensus of $135. That is roughly 38% upside.

If you are looking for an entry point. consider dollar cost averaging between $90 and $100. Set a stop loss below $80 if you are risk averse. And keep watching quarterly earnings for confirmation that the turnaround story is on track.

Ready to stay on top of DIS stock updates? Bookmark FintechZoom for the most current fintechzoom dis stock prediction reports. real time analysis. and smart investment insights delivered weekly.