Gold Price Surge Dollar Decline 2026 Stock Market Impact: Markets Are Repricing American Power

Gold Price Surge Dollar Decline 2026 Stock Market Impact is the defining macro story of this decade, and FintechZoom.Live is tracking every tick in real time. While President Trump insists the dollar remains strong, the greenback has dropped roughly 9% over the past year and gold has ripped to all-time highs above $5,600 per ounce before pulling back to the mid-$4,000 range. Markets are quietly repricing American economic power as foreign holders question Treasury exposure and central banks treat gold as strategic insurance rather than a simple commodity. In this 2026-forward analysis, we break down the mechanics behind dollar weakness, forecast gold trajectories through 2030, and deliver actionable buy-or-sell signals for Magnificent 7 names, meme stocks, EV disruptors, AI leaders, and dividend plays. Zero-delay data plus expert forecasts start here.

Key Takeaways

- The U.S. Dollar Index has declined approximately 9-10% over 12 months, making dollar-priced assets cheaper for foreign buyers but raising capital flight risks.

- Central banks purchased over 1,000 tonnes of gold annually since 2022, with China cutting U.S. Treasury holdings to $693 billion as of February 2026.

- BRICS nations are constructing gold-backed settlement infrastructure and payment alternatives outside SWIFT, with operational targets set for 2030.

- Tech giants face mixed effects from dollar weakness: currency translation gains overseas but margin pressure from volatile macro conditions and tariff uncertainty.

- A 5-15% allocation to gold through physical bullion, ETFs, or quality mining stocks offers portfolio insurance without overexposure to single-asset risk.

Why the Dollar Is Weakening Despite Strong U.S. Markets (Exorbitant Privilege Under Pressure)

Gold Price Surge Dollar Decline 2026 Stock Market Impact | The dollar is losing ground because foreign investors demand higher risk premiums for U.S. debt and geopolitical shocks are accelerating reserve diversification. This is not a cyclical dip. It is a structural repricing of American creditworthiness that affects every asset class from Treasuries to tech equities.

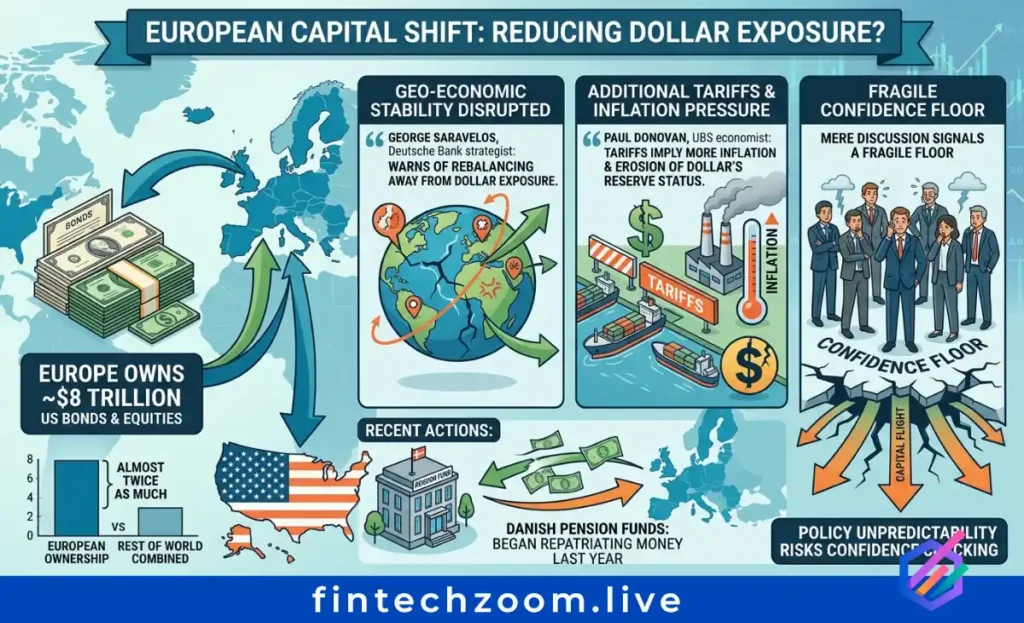

Treasury demand mechanics are shifting in ways that signal long-term fragility. Foreign investors now hold approximately 30% of publicly held U.S. debt, down from more than 50% during the Global Financial Crisis. China has reduced its Treasury stash to $693 billion, falling to third place among foreign holders behind Japan and the United Kingdom. Over the 12 months through February 2026, China and Hong Kong combined shed $96 billion in Treasury exposure. Meanwhile, the Euro Area has been loading up on Treasuries, adding $164 billion over 12 months to reach a record $2.0 trillion. This creates a paradox: total foreign ownership has climbed to a record $9.4 trillion even as traditional anchors like China retreat, suggesting that financial centers rather than sovereign allies are absorbing issuance.

Europe owns roughly $8 trillion of U.S. bonds and equities, almost twice as much as the rest of the world combined. Deutsche Bank strategist George Saravelos warned clients that in an environment where geo-economic stability is disrupted, Europeans may rebalance away from dollar exposure. Danish pension funds began repatriating money last year, and UBS economist Paul Donovan noted that additional tariffs imply more inflation pressure and further erosion of the dollar’s reserve status. The mere discussion of capital flight inside major investment banks signals a fragile confidence floor that could crack if policy unpredictability continues.

Trump trade shocks and Fed independence fears compound the pressure. When Trump announced sweeping tariffs in April 2025, Treasury yields rose and the dollar fell simultaneously, indicating genuine capital flight rather than simple portfolio rotation. Markets feared Trump would install a Fed loyalist to force rate cuts. When Trump nominated Kevin Warsh in January 2026, gold plunged 12% and silver dropped over 30% in a single day because Warsh was perceived as more hawkish and independent than feared. The violent reaction proved how much the debasement trade had relied on political interference fears, and it showed that dollar confidence remains tethered to Fed credibility.

Real interest rates and currency confidence are collapsing in tandem. The U.S. 10-year Treasury yield has eased toward 4.1% while inflation expectations remain sticky, compressing real returns. The DXY has traded near 98, down from peaks above 106 in 2022-2023. Wall Street forecasts imply DXY settling around 99.2 by year-end, with EUR/USD ranging between 1.10 and 1.25. If foreign buyers go on strike at Treasury auctions, the dollar could face disorderly repricing rather than managed decline.

Gold as the Ultimate Stress Signal – Central Banks Are Voting With Their Wallets | Gold Price Surge Dollar Decline 2026 Stock Market Impact

Gold has become the preferred hedge against systemic risk because it carries no counterparty liability and sits outside sanctions reach. Central banks are not trading gold for short-term profit. They are accumulating it as permanent portfolio insurance against a fragmenting monetary order.

BRICS de-dollarization is advancing through practical infrastructure rather than headlines. The bloc controls 72% of rare earth reserves, 40% of global oil, and over 12,000 tonnes of gold. Russia and China now settle over 90% of bilateral trade in rubles and yuan. Project mBridge, a blockchain-based payment platform connecting central bank digital currencies backed by gold and local currencies, processed over $55 billion in transactions by late 2025. The proposed BRICS settlement unit would be backed 40% by gold and 60% by member currencies, with kilo bars stored across member vaults. These systems target operational status by 2030, creating a parallel financial rail that reduces dependency on dollar clearing.

Central bank gold buying has hit structural levels that suggest a permanent demand floor. From 2022 through 2024, net central bank purchases surpassed 1,000 tonnes annually, more than double the prior decade average. In 2025, buying remained elevated at 863 tonnes despite record prices. China extended its buying streak to 17 consecutive months through March 2026, reaching approximately 2,313 tonnes. Poland added 67 tonnes in the first half of 2025 alone. The World Gold Council reports that 95% of surveyed central banks expect global gold reserves to increase over the following 12 months. This is not speculative flow. It is sovereign asset reallocation.

Gold price performance in 2025 was historic by any measure. The metal achieved over 50 all-time highs and returned more than 60% through November. It peaked above $5,600 in January 2026 before correcting sharply. Amundi Investment Institute models suggest gold could reach $4,200 in 2026 and $5,000 by 2028 due to structural demand shifts. Silver has surged alongside gold, with industrial crossover demand from solar and electronics adding beta to the precious metals complex. The gold-to-S&P 500 ratio has climbed, indicating that capital is rotating from paper equity claims to hard stores of value.

Gold ETFs and mining stocks offer liquid equity-market hedges for investors who prefer brokerage accounts to vaults. Global gold ETFs witnessed record annual inflows of $89 billion in 2025, with assets under management doubling to $559 billion. The Sprott Gold Miners ETF and Junior Gold Miners ETF provide exposure to large-cap and mid-tier producers with strong balance sheets. As operational costs rise, quality miners with low debt-to-equity ratios offer amplified exposure to spot prices without single-mine risk.

Stock Market Repricing – Sector-by-Sector Impact and Buy/Sell Decisions

The gold price surge dollar decline 2026 stock market impact playbook varies by sector, with tech, meme, and dividend names responding differently to currency repricing. Investors must distinguish between temporary currency translation effects and permanent margin erosion caused by input cost inflation and tariff uncertainty.

Magnificent 7 Winners and Losers in a Weaker Dollar World

NVDA and AI chip demand remain structurally bullish, but margin compression from tariff uncertainty and supply chain reconfiguration demands caution. A weaker dollar helps NVIDIA’s foreign revenue translation, yet export restrictions to China and volatile capital expenditure cycles from hyperscalers create headwinds. The stock trades at premium multiples that assume flawless execution; any macro shock could trigger sharp multiple contraction that wipes out currency gains.

TSLA faces a more complex matrix. Dollar weakness should theoretically boost overseas pricing power, but robotaxi regulatory timelines and EV export competition from Chinese manufacturers complicate the bull case. If the dollar decline reflects genuine loss of confidence in U.S. governance rather than simple interest rate differentials, risk assets including Tesla could suffer multiple compression regardless of currency effects.

AAPL, MSFT, AMZN, META, and GOOGL generally benefit from foreign earnings translation when the dollar weakens. These companies generate substantial revenue outside the United States, so a lower dollar inflates reported earnings in greenback terms. However, if dollar weakness coincides with tariff escalation or retaliatory measures against U.S. tech, the net effect turns negative. Apple has shown resilience, rising 0.5% even during the January 2026 gold meltdown that hit miners hard. The key is monitoring whether currency tailwinds outweigh regulatory headwinds.

Meme Stocks, EV Disruptors and High-Beta Plays

AMC and GME retain their short-squeeze sensitivity, but dollar hedging by institutional desks can amplify volatility. When gold surges and the dollar drops, macro funds often reduce risk exposure across speculative names. Meme stocks depend on retail flow stability; a disorderly dollar decline could drain liquidity from the riskiest pockets of the market faster than fundamentals can justify.

Rivian, Lucid, and NIO face amplified foreign exposure through divergent channels. These EV names rely on global supply chains and overseas growth markets. Dollar weakness raises input costs for imported components while potentially helping overseas sales if local currencies strengthen against the greenback. For U.S.-based EV makers, the input cost effect often dominates, squeezing gross margins at exactly the moment when scale matters most.

PLTR, CRWD, and SMCI sit at the intersection of government contracts and AI infrastructure. Palantir’s government revenue provides a defensive backstop, yet dollar weakness that forces fiscal austerity could pressure defense and intelligence budgets. CrowdStrike benefits from non-discretionary cybersecurity spending, making it relatively resilient. SMCI remains tied to data center capex cycles, which correlate with liquidity conditions and could face cuts if rates stay higher for longer.

Legacy Dividend Plays and Blue Chips

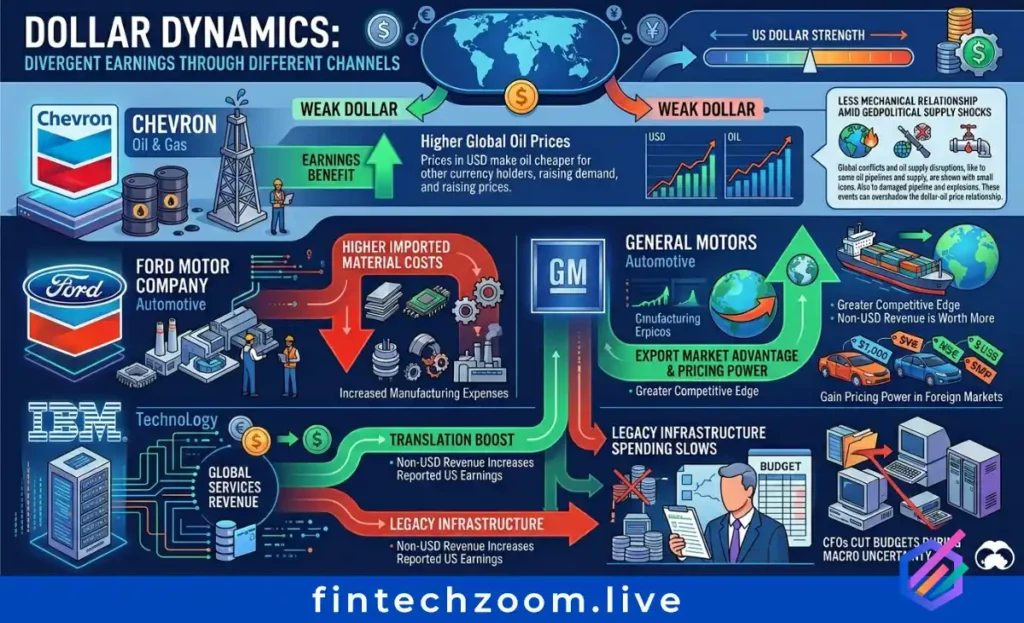

Ford, GM, IBM, and Chevron face dollar-sensitive earnings through divergent channels. Chevron benefits when dollar weakness lifts oil prices, though the relationship has become less mechanical amid geopolitical supply shocks. Ford and GM face higher imported material costs but gain pricing power in export markets. IBM’s global services revenue receives a translation boost, yet legacy infrastructure spending slows when CFOs cut budgets during macro uncertainty.

Best dividend stocks to buy now in a gold-repricing era include consumer staples with domestic revenue bases, utilities with regulated returns, and energy names with low production costs. These sectors offer cash flow stability when currency volatility rises and interest rate uncertainty persists.

Portfolio Playbook – 2026 Allocation Strategies

Investors should treat gold as portfolio insurance rather than a speculative trade, allocating 5-15% depending on risk tolerance and dollar exposure. This range aligns with both institutional advisory standards and central bank reserve diversification logic. The goal is not to predict the exact peak in gold but to own an asset that historically preserves purchasing power when fiat confidence erodes.

Gold ETF vs. physical vs. mining stocks requires careful ranking based on liquidity needs and risk appetite. Physical bullion offers zero counterparty risk but carries storage costs and liquidity delays. Gold ETFs like GLD and IAU provide instant liquidity and tight tracking of spot prices. Mining stocks offer amplified exposure but add equity beta and operational risk. The Sprott Gold Miners ETF emphasizes quality large-cap producers with strong revenue growth and low debt. Junior miners through SGDJ add exploration upside but require higher risk tolerance and longer time horizons.

Treasury bond rates today demand a fixed-income rotation. With the 10-year yield near 4.1% and real rates compressed, long-duration Treasuries offer limited inflation protection. TIPS provide some shelter, yet if the dollar decline accelerates, foreign buyers may demand even higher yields, pushing prices lower. Short-duration government paper and gold-backed bonds offer a middle ground that preserves capital without full exposure to duration risk.

Crypto and Bitcoin ETF correlation with dollar decline remains positive but volatile. Bitcoin has traded as a risk-on asset during dollar weakness, yet it lacks gold’s central bank bid and multi-millennia track record. A blended approach using both gold and crypto hedges against different failure modes: gold protects against sovereign credit risk, while crypto protects against monetary debasement and capital controls.

Live tools on FintechZoom.Live including the stock screener and gold price tracker help investors monitor real-time correlations between DXY, Treasury yields, and sector rotations. Use these screens to flag when tech exposure exceeds risk thresholds or when gold miner valuations detach from spot prices.

Risks and Black Swans to Watch Through 2030

A disorderly dollar decline poses the greatest systemic threat to global portfolios. If foreign holders coordinate Treasury selling rather than simply refusing to roll over maturities, the United States could face a funding crisis that forces abrupt Fed accommodation and fiscal retrenchment. The April 2025 tariff shock showed how quickly capital flight can materialize when policy credibility cracks, with yields spiking and the dollar falling simultaneously.

Fed policy interference and inflation reacceleration remain live risks that could trigger violent repricing. If the next Fed chair faces political pressure to cut rates into sticky inflation, real yields could collapse and send gold parabolic. Conversely, if the Fed maintains hawkish independence to defend the currency, risk assets including stocks and crypto could face liquidity drains. The market’s violent reaction to Kevin Warsh’s nomination demonstrated how sensitive gold is to perceived Fed independence, with a 12% single-day drop erasing weeks of gains.

Plaza Accord 2.0 or coordinated intervention odds are rising as dollar weakness becomes a global problem. If the decline turns chaotic, G7 finance ministers could agree on joint currency support. Such intervention would temporarily boost the dollar and crush gold momentum. However, structural drivers including BRICS settlement systems and central bank diversification would likely reassert within months, making any intervention a selling opportunity for dollar strength rather than a long-term trend reversal.

Actionable Investor Checklist – What to Do This Week

Immediate steps for retail and institutional investors center on reducing single-currency risk and adding asymmetric hedges. Start by measuring your portfolio’s dollar exposure through international revenue shares and currency-hedged positions. Buy candidates include quality gold miners with free cash flow, large-cap tech with dominant foreign revenue streams, and consumer staples with pricing power. Hold positions in core S&P 500 index funds but reduce concentration in names trading above 30x forward earnings. Sell or trim speculative EV names without near-term profitability, meme stocks dependent on retail flow stability, and long-duration Treasuries vulnerable to foreign buyer strikes.

Portfolio rebalancing steps include raising cash to 10% for opportunistic deployment, adding 5-10% gold exposure through ETFs or physical storage, and reviewing international equity allocations for currency hedge ratios. Institutional investors should stress-test portfolios for a 10% DXY drop and a concurrent 20% Treasury yield spike to identify hidden convexity risks.

Conclusion

FintechZoom.Live delivers zero-delay reporting and semantic-rich analysis so you move before the market does. The shift from dollar dominance to gold is already underway. Central banks have voted with their wallets. Treasury mechanics are fraying. Tech, meme, and dividend stocks face divergent futures depending on how quickly the repricing unfolds. Your edge starts with real-time data and ends with disciplined execution.

Frequently Asked Questions

Will the dollar collapse in 2026? A full collapse remains unlikely. The dollar still dominates global trade and reserves at roughly 56-58% of allocated reserves. However, gradual erosion is well underway, and a disorderly decline is possible if foreign buyers strike at Treasury auctions. Most economists expect managed weakness rather than sudden collapse.

Is gold still a buy at current prices? Gold remains structurally supported by central bank buying and de-dollarization trends, but near-term volatility is elevated. After hitting $5,600 in January 2026, gold corrected sharply following the Warsh Fed nomination. Dollar-cost averaging into positions reduces timing risk for long-term holders.

How does dollar weakness affect NVDA and TSLA stock prices? Dollar weakness helps foreign revenue translation for both companies, yet tariff uncertainty and export restrictions to China create offsetting headwinds. NVDA faces AI capex cycle volatility, while TSLA contends with global EV competition and robotaxi regulatory delays.

Which gold ETFs or mining stocks should I buy in 2026? Consider physical ETFs like GLD and IAU for spot exposure, or quality miner ETFs like SGDM for large-cap producers with strong balance sheets. Junior miners add leverage but require higher risk tolerance.

What is BRICS de-dollarization and why does it matter for U.S. stocks? BRICS nations are building payment systems and settlement units backed by gold and local currencies to reduce dollar dependence. This matters because reduced Treasury demand raises U.S. borrowing costs and pressures multinational earnings through currency volatility.

Should I sell Treasuries or rotate into commodities? Selling all Treasuries is extreme. Consider shortening duration, adding TIPS, and allocating 5-15% to gold or commodities. A complete exit from fixed income removes portfolio ballast.

How will Fed independence under Trump impact stock futures? Perceived threats to Fed independence have driven gold surges and dollar weakness. If independence is preserved, the dollar may stabilize and rate-cut expectations moderate. If political pressure mounts, expect higher volatility across stock futures and precious metals.

Best stocks to buy now in a gold-repricing environment? Focus on large-cap tech with foreign revenue, quality gold miners, consumer staples, and energy names with low production costs. Avoid speculative names with weak cash flows and high dollar-sensitive input costs.

Gold vs. Bitcoin: which hedge wins in 2026-2030? Gold offers central bank support, zero counterparty risk, and millennia of track record. Bitcoin provides digital scarcity and portability but trades with higher volatility and regulatory risk. A blended allocation captures both sovereign credit hedges and monetary debasement protection.

Live gold price forecast – when does the next leg up begin? Gold needs a catalyst such as renewed Fed dovishness, escalation in Middle East tensions, or a Treasury buyer strike. Amundi models suggest $4,200 in 2026 with upside to $5,000 by 2028. Monitor DXY breaks below 95 and 10-year yield compression for technical triggers.