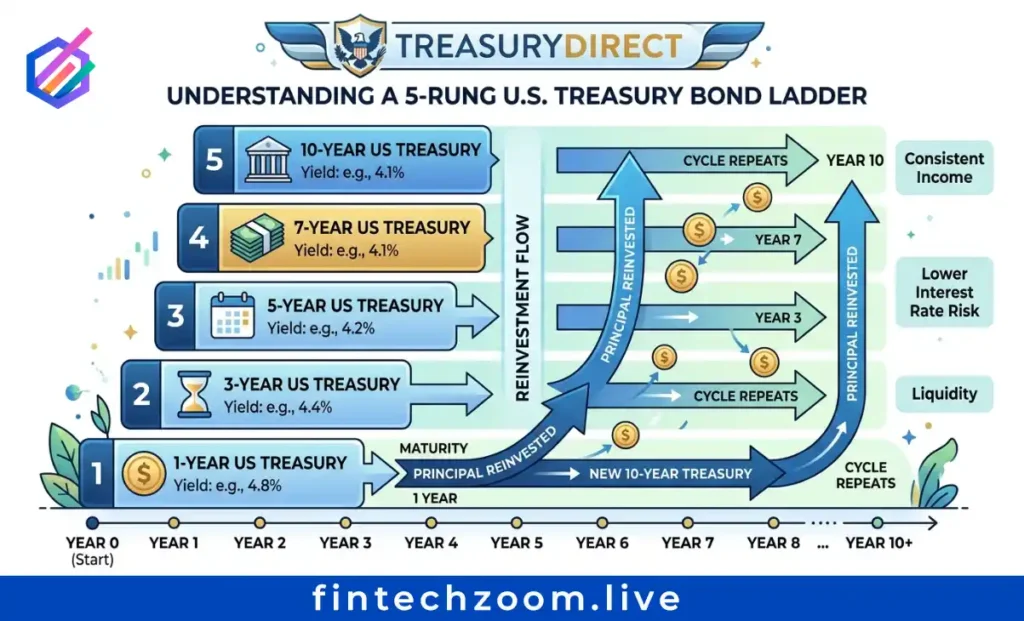

A 2026 ladder might include 1-year, 2-year, 3-year, 5-year, and 10-year Treasuries, with maturing principal reinvested at the long end. This approach mitigates interest rate risk while maintaining liquidity options.

Bond yield versus bond price relationship follows mathematical inverse correlation. When yields rise, prices fall, with longer durations experiencing greater price sensitivity. A 10-year Treasury with 8-year duration declines approximately 8% in price for every 1% yield increase. Understanding this relationship prevents panic selling during rate-driven price declines.

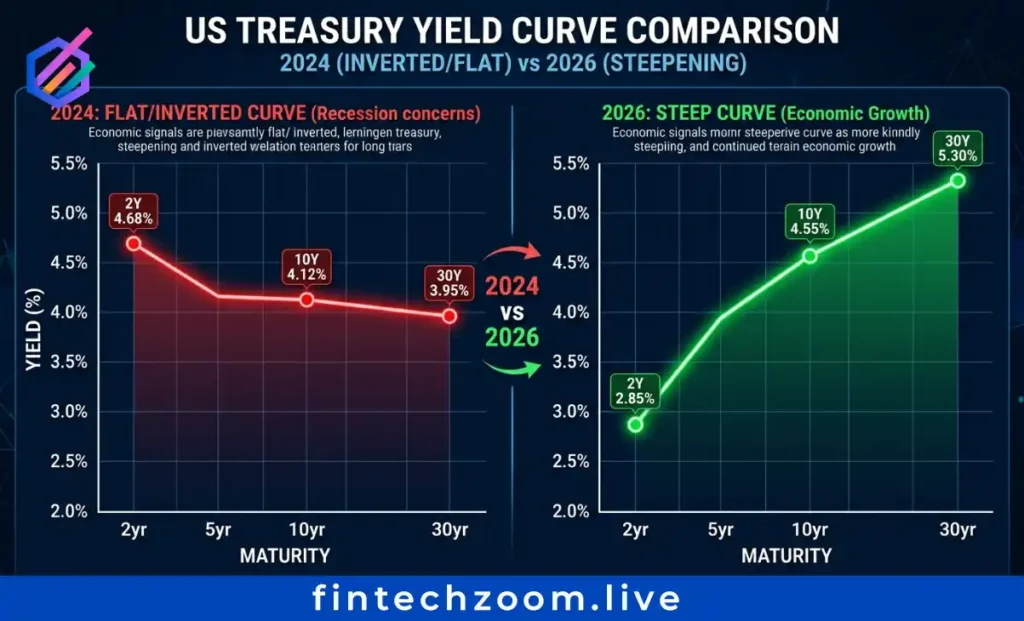

The inverted yield curve phenomenon that characterized 2023-2024 has largely normalized, with 10-year yields now exceeding 2-year yields by 50 basis points. This steepening historically precedes economic expansion but may also reflect term premium increases from debt supply concerns. Current curve shape favors intermediate maturities over extreme short or long positions.

Government versus corporate bonds present distinct risk-return profiles. Treasuries carry no credit risk but face inflation and rate risk. Corporate bonds add credit risk compensated by yield spreads. In 2026, investment-grade corporate spreads near historic lows suggest limited compensation for credit risk, favoring Treasury allocations for risk-averse investors.

Best bond ETF selections include:

Vanguard Total Treasury ETF: 0.05% expense ratio, broad duration exposure

iShares 7-10 Year Treasury ETF: Intermediate focus, 4.2% yield-to-maturity

Vanguard High-Yield Corporate ETF: 4.5% yield, diversified credit exposure

iShares National Muni Bond ETF: 3.8% yield, tax-advantaged income

Schwab US TIPS ETF: Inflation protection, real yield exposure

Treasury Bond Rates Today vs Stocks Comparison 2026 – Where to Allocate in a Higher-for-Longer World

Historical performance data demonstrates bonds’ role as portfolio ballast during equity volatility periods. In 2022, when stocks declined 18%, intermediate Treasuries fell only 12%, while short-term Treasuries declined less than 5%. This downside protection justifies fixed-income allocations even when equity returns appear more attractive.

The 2026 investment outlook suggests bonds for income generation and diversification, growth stocks for capital appreciation. With 10-year Treasuries yielding 4.3% and S&P 500 earnings yields near 5.0%, the risk premium for equities has narrowed, making high-quality bonds relatively attractive for risk-adjusted returns.

Portfolio allocation models require personalization based on age, risk tolerance, and income needs. Traditional 60/40 stock/bond allocations face pressure from correlated declines during rate shock periods. Alternative approaches include all-weather portfolios balancing growth, inflation, and deflation scenarios, or barbell strategies combining short-term bonds with long-term growth equities.

Meme stocks like GameStop and AMC demonstrate extreme volatility that bonds offset through stability. When equity sentiment deteriorates, Treasury prices typically rise as investors seek safety, providing negative correlation benefits. Rotation from speculative equities to high-quality bonds during market stress preserves capital for future opportunities.

EV disruptors including Lucid and Rivian show particular sensitivity to interest rate changes. These capital-intensive companies rely on debt financing for operations and expansion. Rising Treasury yields increase their borrowing costs while reducing the present value of future profit projections. This double impact creates elevated risk for speculative growth companies in higher-rate environments.

Bond Ladder Strategy Guide + Duration Risk Explained

Building a 2026 bond ladder requires selecting maturities that align with cash flow needs and reinvestment expectations. A five-rung ladder might include 1-year, 2-year, 3-year, 5-year, and 10-year Treasuries with equal dollar allocations. As the 1-year bond matures, proceeds purchase a new 10-year bond, maintaining the ladder structure while capturing current yields.

Duration risk measures price sensitivity to interest rate changes. Modified duration of 5 years indicates approximately 5% price decline for every 1% yield increase. Short-term bonds (1-3 year duration) minimize this risk but offer lower yields. Long-term bonds (15+ year duration) maximize yield but expose portfolios to significant volatility.

Current yield curve positioning suggests intermediate durations (5-8 years) optimize the risk-reward tradeoff. These maturities capture most of the available yield while limiting duration exposure if rates rise further. The steep curve provides incremental yield for extending maturity from 2 years to 10 years, justifying modest duration extension.

Real-world ladder implementation through TreasuryDirect requires minimum $100 purchases per security, with no maximum limits for most instruments. Electronic holdings simplify management and eliminate paper certificate risks. Automatic reinvestment options facilitate ladder maintenance without active trading decisions.

How to Buy Treasury Bonds Rates Today Direct – Zero-Commission Playbook

TreasuryDirect account establishment takes approximately 10 minutes online. Required information includes Social Security number, U.S. address, bank account details for funding purchases, and email address for notifications. Account verification typically completes within 24 hours, enabling immediate trading capabilities.

Treasury bill purchases suit investors seeking short-term cash management with maturities from 4 weeks to 52 weeks. These instruments sell at discount to face value, with returns representing the difference between purchase price and maturity value. Current 1-year Treasury bills yield approximately 4.1-4.3%.

Treasury notes (2-year to 10-year) provide intermediate duration exposure with semi-annual interest payments. These instruments trade in $100 increments with active secondary markets ensuring liquidity. Notes suit income investors seeking predictable cash flows without long-term commitment.

Treasury bonds (20-year to 30-year) offer maximum yield for liability-matching strategies. These long-duration instruments require careful evaluation of inflation and rate risks but provide guaranteed income for retirement planning or endowment management. Current 30-year yields near 4.9% represent multi-decade highs.

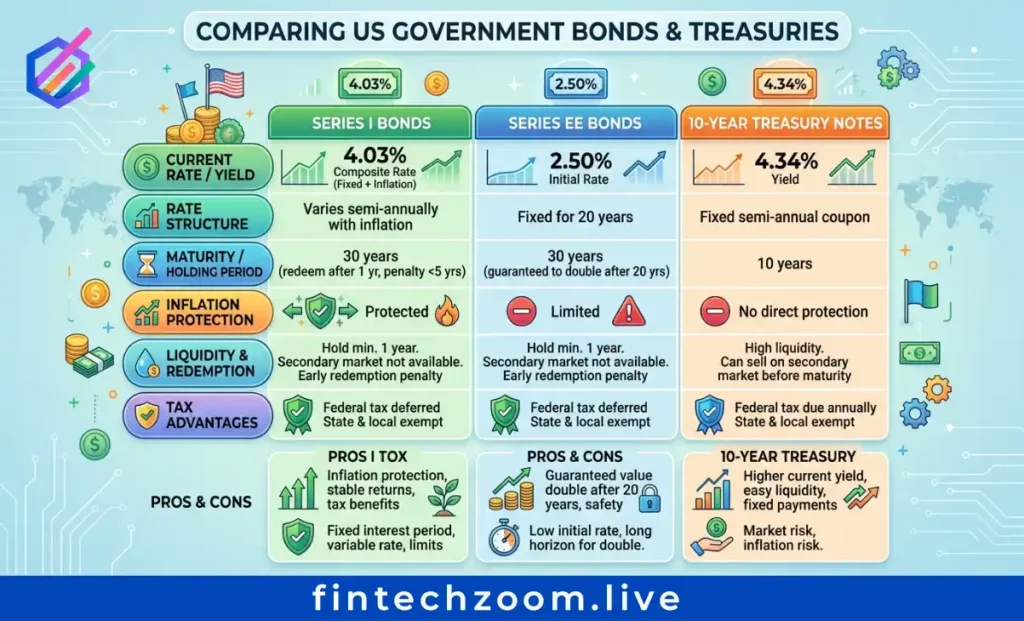

Treasury Inflation-Protected Securities (TIPS) provide real yield exposure with principal values adjusting for CPI changes. Current 10-year TIPS yields near 1.5-2.0% offer positive real returns absent in much of the 2010-2021 period. TIPS suit investors concerned about inflation erosion of nominal returns.

Tax implications favor Treasury securities over corporate bonds for high-bracket investors. Treasury interest remains exempt from state and local income taxes, providing 0.5-1.0% yield enhancement on a tax-equivalent basis for residents of high-tax states. This advantage compounds over multi-year holding periods.

Liquidity considerations favor Treasury ETFs for investors requiring rapid position adjustments. While TreasuryDirect purchases can be sold through the Secondary Market program, execution takes several business days. ETF shares trade intraday with immediate settlement, providing flexibility for dynamic asset allocation.

Actionable Takeaways

Treasury bond rates today present opportunities unseen in over a decade, with risk-free yields exceeding 4% across much of the curve. The 2026 outlook suggests continued elevation with potential for modest declines if the Federal Reserve achieves soft landing objectives. Investors should emphasize intermediate durations, maintain credit quality discipline, and utilize tax-advantaged savings bonds for appropriate allocations.

FintechZoom.Live delivers the real-time monitoring and analysis necessary for successful fixed-income investing in volatile markets. Track live Treasury yields alongside Magnificent 7 stock correlations, receive alerts for significant rate movements, and access expert commentary on Federal Reserve policy developments.

Subscribe now for daily bond market alerts, yield curve analysis, and integrated stock market intelligence. Your edge starts here – live.

Key Takeaways:

Elevated rates persist through 2026 – CBO projects 10-year Treasury rates at 4.1% for 2026, rising to 4.3% by 2027, with interest costs consuming over $1 trillion annually.

Yield curve steepening creates opportunity – Long-term rates are rising faster than short-term rates, favoring intermediate-duration bond strategies over ultra-long positions.

Savings bonds offer inflation protection – Series I bonds currently yield 4.03% with inflation adjustment, while Series EE bonds guarantee doubling in 20 years at 2.50% fixed.

Federal Reserve policy remains data-dependent – Eight FOMC meetings in 2026 will determine the path from current 3.50-3.75% federal funds rate toward projected 3.00-3.25% by year-end.

Record debt issuance requires vigilance – OECD sovereign borrowing hits $18 trillion in 2026, increasing supply pressure and demanding selective credit quality focus.